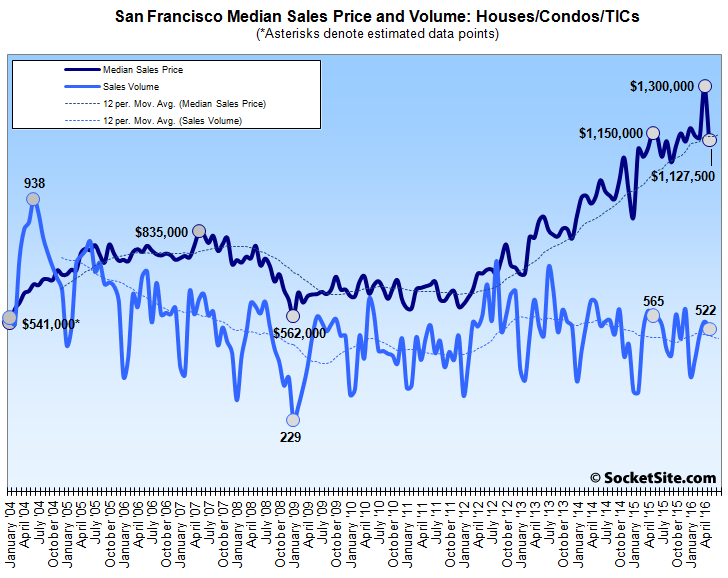

At a time of the year when sales typically increase by 10 percent versus the month before, the recorded sales volume of single-family homes and condos in San Francisco dropped 4.2 percent from April to May and was 7.6 percent lower versus the same time last year. At the same time, listed inventory levels are currently running over 50 percent higher.

And having hit a record $1.30 million in April, “driven largely by a change in mix which is being amplified by the slowdown in sales,” as we reported at the time, the median sale price for the San Francisco homes that changed hands in May, which includes new construction sales, dropped 13.3 percent to $1.13 million and is now running 2.0 percent lower versus the same time last year. The recorded year-over-year drop in the median is only the second since 2011.

Across the greater Bay Area, home sales increased 3.2 percent from April to May but are running 4.2 percent lower versus the same time last year, with the greatest year-over-year drops in Marin (down 12.4 percent) and San Mateo (down 11.3 percent). The median price of the homes that sold was $700,000, up 1.4 percent from April and 6.3 percent higher versus the same time last year.

And based on 1,490 sales, which was 1.5 percent lower versus the month before and 9.7 percent lower versus the same time last year, the median sale price in Alameda County, which includes Oakland, was also $700,000 in April, 2.1 percent higher versus the month before and 8.9 percent higher versus the same time last year.

Keep in mind that while movements in the median sale price are a great measure of what’s selling, they’re not necessarily a great measure of appreciation or changes in value and are susceptible to changes in mix, as opposed to movements in the Case-Shiller Index.

My simple interpretation: prices are stabilizing. Betcha next few months of data will bear that out. No need to sound off any major alarms IMO. Business as usual for SF RE at this point in the cycle. Carry on

Yes, because look at all of those ‘plateaus’ and ‘stabilizations’ in the chart! IMO…

Err….X axis of chart is highly compressed. Spread that puppy out a bit and it’ll look a lot flatter. Relativity.

So, your explanation is, essentially “no no no, it’ll plateau for, like, 4 whole months before it drops!”.

Call me crazy, but I don’t consider that a plateau, relatively speaking.

Prices had doubled from Jan 2012 to Jan 2016.

SF RE is everything but flat.

Yeah, and they fell 33% from Jan 07 – Jan 09. Who’s to say we’re not at a Jan ’07 moment, just with a higher climb and higher volatility.

Which means there’s potentially farther to fall. Not saying I’m right, but I don’t think I’m completely wrong, either.

Yes, and we’re likely to see a correction I think. Now it will be a different event than the last correction, since the latest price jump comes from actual cash and not debt-fueled speculation.

But I do see some craziness in the market. Like a guy in the 94114 who buys a very decent (and pricey) house at $1000/sf and plans to double the square footage, baking in the current $/sf and probably expecting an increase. He’s probably doing that with his own cash but the behavior is bubbly.

Worth getting a reality check regarding the amount of actual cash going round.

“If you’re in the market for a home, it might seem like cash is king. But the percentage of homes being purchased without a mortgage in the Bay Area has fallen in the past few years and is much smaller here than in most parts of the country.

[…]

Six of the 10 metros with the smallest share of cash buyers were in California, including the San Francisco and San Jose areas.

[…]

In October, about 29 percent of homes purchased nationwide didn’t have a mortgage.

[…]

In San Francisco-Oakland-Hayward, only 20.6 percent of October purchases were all-cash, and in San Jose-Sunnyvale this number was 22 percent.”

And even purchases that seem to be all cash may only be using cash pulled together to bridge into getting a mortgage.

“To make their offers more competitive, some buyers — especially in the Bay Area — make an all-cash offer, often with help from family members. Then, shortly after the purchase, they take out a mortgage.

[…]

The counties with the highest percentage of post-purchase mortgages were San Francisco (24 percent),”

So only 20% of SF purchases start out all cash and then about a quarter of those subsequently get a mortgage. So 85% of purchases here end up with a mortgage.

Good point, anon.

But with the median over $1M, the buyers pulling this kind of financing are not your average Joe. They have to be 100% certain they’ll qualify and be able to pay off what they borrowed.

Often using a mortgage is just a way to keep your assets balanced. For instance when I purchased in 2010 I could have paid all cash but decided to have a mortgage on less than 50% to use the leverage. Of course I paid off that mortgage last year as planned 😉

Roy, Roy, Roy, first, SF didn’t crash 07-09. More like end of 08 through 09 was the major decline. Second, it wasn’t 33% city wide. More like 15-20% citywide, with d10 hitting mid-high 30’s%.

Third, and wrt the chart, I consider movement +/- 10% as noise, given seasonality, housing mix vs actual prices, and that the up cycles have normally been tremendous. So when I say stable it includes a moderate decline. And stable means until the next run up, where we go bonkers again. Kapish?

That sure is a big drop. But unlikely it will get back to $562,000. When it was at $562,000, I remember it well, Socketsite commenters screamed that it was sure to go lower.

If you have any interest in trying to be accurate rather than inflammatory, here’s the link to said point in time and all the comments: San Francisco Recorded Sales Activity In January: Down 21.8% YOY

Keep in mind the moving average continued to decline for another eight months and didn’t start to recover until two years after that.

Wow, I can’t believe this was already 8 years ago.

Context is everything though. We had permabulls telling us there was no hit. This was a victory lap more than 2 years in the making and it felt really good.

12 months after these comments, I realized there was no deeper bottom and pulled the trigger.

brilliant observation that moving averages lag

And yet relevant when dealing with a highly seasonal data set.

Yes, and we’ll see by the end of the year if this is an actual inflexion point.

Are u being sarcastic … I hope so…. Obviously a moving average lags…. Inherent in the definition…

Nope, the comments before and for at least for a year after that 562k low were almost unanimously shrill that prices were headed lower. A corollary theme was that not only were prices headed lower, but that the market was really bad. Yet I kept going to open houses and seeing lots of buyers and listings quickly sold. There were only one or two commenters who thought the market wasn’t so bad and that prices would rise. I was impressed by how many people were so insistent that prices would head lower and I hoped this was a contra-indicator, which it proved to be. They all wanted lower prices so they could buy. There was one honest guy who said the fact that the market didn’t completely collapse was a major disappointment to him because he really wanted to buy at a low price. When you have too many people praying for the market to drop, it doesn’t.

I have no idea what prices will do now. Prices sure seem high. I’m not selling here though because selling and trying to buy lower is tough given transactions costs.

And once again, if you’re interested in the actual discussion at the time, here’s a link to the report and comments a year out from the median having dropped to $562,000: San Francisco Recorded Sales Activity In January: Up 35.8% YOY, from which one can easily click back to the report and comments the month before that, and so on and so forth.

Peter Lynch, has always said.

This biggest fools in any market, are the ones waiting for the very top and the very bottom.

It’s still just a reversion to the moving average – i.e. essentially a doubling in four years – and we all know everyone in the world wants to live in – or more precisely buy in – San Francisco (especially after Brexit, or Frexit, or D2exit or whatever), so why should the fun stop?

I fully expect $36,080,000 in ’36 …it even has a nice ring to it:

THIRTY SIX IN THIRTY SIX !!

THIRTY SIX IN THIRTY SIX !!

Why does no one care to acknowledge the substantial decline from ’07 – ’09? If you fail to learn from history, well…

and completely flat from ’09- ’11

2007 to 2009, in San Francisco?

Nobody is acknowledging it because that’s not how it happened in SF. 2007 in particular was a top year.

Sales volume had been steadily dropping since 2004, prices in the southeast neighborhoods had been on the decline since 2006, and the majority of the market in San Francisco had peaked by the end of 2007.

Indeed. I’d responded to someone who stated 07 through 09. You responded to me with a “peak by the end of 2007.” I don’t see why you felt that necessary.

And once again, prices in the southeast neighborhoods had been on the decline since 2006 and prices in many mid-tier areas were already declining in 2007.

Also, sales volume dropping since 2004 is inaccurate.

sorry, “steadily,” that was … it was peaks and troughs. I think late ’03 marked the beginning of some let’s say creative type lending? so that’s why 04 was such a buying frenzy …

Those peaks and troughs are primarily artifacts of seasonality. Try taking a look at the moving average above.

yes, of course southeast neighborhoods. that was something many argued against on here.

Frexit? I probably missed that memo.

FRenchEXIT

DEutscheEXIT > DEEXIT > D2EXIT

Someone over there is always unhappy.

I thought about HongKongExit – or HEXIT – but that seemed too unlucky to ever pass.

Yeah, I am aware of the words. I just don’t think they’re a thing yet. Now tell me about Grexit.

If there’s any talk about Hexit, expect a few more booksellers to go AWOL.

It’s a twenty year window…I like to think ahead.

If the window is big enough everything will go through it.

Well eventually the EU will just be a Germaining…

Thirty Six – perhaps, the current prices are already unreal and if stagflation returns, but it will just be a number.

13.3% drop month-over month and now Brexit … at this rate we’ll be at zero by Christmas!

The top of mid-2006 coincided with the 17th rate raise by the fed which put the last nail in the coffin for reckless RE financing.

Brexit could be the defining moment of the current cycle. Cheap money has fueled speculation in equities. I think the central banks are going to go into panic mode and give a massive influx of cheap money into the current bubble which could cause its demise.

Or inspire a flight from Britain to the U.S. and prolong it for a year or two.

“…massive influx of cheap money into the current bubble which could cause its demise.”

Well, the Fed intentionally created an asset bubble with a massive influx of cheap money, so why would it change course now?

Single Best Day For Mortgage Rates in More Than a Year

ZIRP forever!

Interesting to see the various comments in both the 2009 and 2010 threads about how interest rates would soon be rising.

Well, all that stimulus money was obviously going to lead to the hyperinflation we have now.

If you’re serious, I don’t think hyperinflation means what you think it means

If you’re being snide, then well said!

Yes, I don’t think most of us realized to what lengths the Fed would be willing to go to screw the productive economy to bail out housing and stocks. Now we know: there is nothing the Fed won’t do to bail out the extractve FIRE sector, regardless of how badly it screws the wider economy. The Fed clearly prefers widespread misery to letting the assets of a couple thousand extremely wealthy people suffer.

Dow closes 610 points down as a result of brexit.

You know what, I’m gonna go contra on this Brexit thing. Yes final vote was definitely a shock,but on a global level, it’s only Britain. So getting back to my little corner of the world, SF RE, I don’t think it will have a pronounced effect. I don’t think it will funk up world markets long term. Interest rates are sure to stay low for that much longer. Global industry, especially our high tech, will make adjustments. England/UK will survive this. I don’t think this will be a turning point of a new recession. At least that’s how I read the tea leaves.

Perhaps the local Mediterranean sun is warping my perspective, so I ‘m open to other’s interpretations…

Watch the strong dollar –> Yuan devaluation, emerging market stress, and Euro banks toppling. Brexit is just one domino in a line.

hahaha. Brexit was the result of a series of particularly British events, choices, leadership, and sociological ramifications. “One domino in a line” — maybe, for the Irish, Scots, and Eurozone effected. Not the context you gave though.

I think that if you look at the unexpected success of Brexit, Sanders & Trump you’ll see that status quo angst is spread across the pond and across the political spectrum.

Brexit=populist uprising. The bottom 90% can no longer ignore their declining standard of living, and it’s becoming obvious that the establishment crony capitalist policies are to blame. The promised trickle down effect has not materialized, and the more power they hand over to elitist bureaucrats, the worse it gets. People are dumb but not that dumb. The only real power they have left is a vote, and if you give them the chance, they will stick it to the man right now even if it hurts them in the short term. The biggest lesson we in the US can learn from Brexit is that the pollsters totally blew it, and I think we may be in for a November surprise.

It was populist, sure. That’s pretty much all you got and OK that’s part of it.

I agree completely with you regarding the polling. Partly not their fault, they use many assumptions based on the past to extrapolate from small sample sizes. But I think many assumptions have changed and I expect this years poll predictions to be very inaccurate.

SocketSite editors and commentators are hilariously and desperately bearish. They pick and choose data to try to present a dark picture whenever possible. Small downturn in prices? Must be an imminent collapse! Small upturn in prices? Anomaly in how we compute things!

See any articles on stats like DOM and SFH pricing for April? Or what’s happening district 5? No bulls allowed!

And the editorial responses are hilariously Trump-ian. SS makes a large unfounded statement (“change in mix” issue). Reader correctly calls them out for being hypothetical (as no detail are provided). SS editor responds a la Trump: i’m not hypothetical– you’re hypothetical! Editor then proceeds to provide some high-level details but without backing it with hard data (making themselves irrefutable). However, they are missing the larger point which is that “the mix” _always_ influences the results in both directions, which is why you don’t write lengthy articles about monthly changes like this. It’s like writing large pieces about daily changes in the S&P… too funny. A data point like this IS interesting… but only enough to just present the data. Writing pieces about changes over a longer period of time might be slightly more meaningful (see: statistical significance).

More reputable and even-handed blogs like thefrontsteps calculate similar data, and simply present it… without the amateurish analysis. I’m definitely switching over my readership. Clearly the SS editors are terrible at predicting the direction of the articles, so please refrain from analysis! SS is at it’s best when doing interest-pieces… please stick to that!

We have to agree. If you’re looking for more low-level data versus actual knowledge, need more industry spin, or are uncomfortable with anything other than “bullish” reports, SocketSite isn’t the best resource for you.

But one suggestion should you decide to “return,” when trying to disparage our amateurish analysis, you might want to pick an example in which our analysis was actually wrong versus being spot-on.

I think I pointed out the high level issue already, but here’s another explanation of the issue… Over the past 4 years, venture funding has been on a epochal and unprecedented expansion. During this period, SocketSite headlined two articles about this growth and both were to highlight “drops” in 3Q14 and 4Q15. That’s like covering the Warriors season and only writing articles about the 9 losses. Its what you call lying with statistics. And you do this same thing with many other stats…

I am not a bull. In fact, I started reading SocketSite when many others did– reveling in deadpool/fckdcompany schadenfreude during the crash. But SocketSite has grown to be more than that, so I think it’s time to evolve into more balanced and realistic coverage. I’d love to read it and walk away smarter… and not walk away tricked into believing an agenda that is made clear by the example above.

Or there’s no shame in steering clear of the big picture analysis if you aren’t going to cover it realistically. I love the other reporting, and thank you very much for that. If you can provide well-researched stories about individual properties, that’s something that sets you apart (a lot of other people are doing market analysis). Those stories are fascinating… (although one comment- please wait until the sale is closed to write some of these stories… yes it becomes less current, but the sale price is key to the story, and the list price means nothing)….

VC funding in SF and the SF bay area is well below the peak years of the dotcom. For SF specifically, VC funding has been running in the range of $1 Billion per month for the past 2-3 years. By comparison, in the last two years before the dotcom bust, VC funding in SF totaled around $90 Billion, which is more than $1 Billion per week in 2015 dollars.

FWIW, the VC money goes farther in SF now because many costs-of-doing-Internet-business are lower than back in the dotcom. For example, even with the recent increases in office rents in SF, rents are still ~25% lower than in the dotcom, inflation adjusted.

One of the hidden-underfoot reasons that it is cheaper to grow Internet intensive companies in SF in this boom than it was in the late 1990s is that the VCs and other investors paid $ Billions to install a dense fiber network throughout SF’s FiDi and SoMa neighborhoods and datacenters like 365 Main. A yuge sunk cost that helped bankrupt several $billion valued carriers. Fortunately, fiber rots slowly.

Also hundreds of SoMa buildings had to be seismically upgraded when converted from PDR to office use in the 1990s. Then they got used for a short time before the bust. More investor money sunk into SF durable value that sat with low utilization for years, but was largely written off, leaving many modernized buildings unencumbered.

I’m not aware of any evidence to support a 2016 the claim that “Over the past 4 years, venture funding has been on a epochal and unprecedented expansion.” I’m aware of plenty of evidence to support the same statement circa 2000.

Total dollars is not the only measure, but by that measure, there has still been outstanding growth over the last 4 years. I think you’re missing the point here which is that SS presents an unrealistically negative picture. For example, here’s a graph that is actually enlightening.

Again, look at the graph, and note that SS posted ZERO articles about VC growth and 8 negative articles about “dips”.

I’m not sure what you think is enlightening about that chart. Appears to me to chart uncorrelated phenomena.

FWIW, 5 months ago on SS that same chart was linked in a comment and I explained why I think it shows no direct correlation.

Here is an enlightening chart. A pullback in employment.

That one is enlightening — record high employment and near-record low unemployment. An amazing improvement from 2010, with near 10% unemployment in SF.

Uh, no, that chart does not show “a pullback in employment,” as I explained in my comment on the link you provided. Folks, this is elementary stats. Or do you think Brandon Belt is in a slump because he went 0 for 4 yesterday?

If you draw a trendline on a more granular chart, we have clearly broken the uptrend. Civilian employment in May in SF, at 533,900, was below where it had been in December. The labor force in May, at 549,800, was below where it had been in July 2015.

I’m not sure why VC deal size is that relevant, but even if you believe in the correlation implied by that chart, wasn’t there a run up in deal size leading to the 2000 bubble? And look at the collapse in rents post 2000.

Clearly there have been booms and busts in the recent past. Maybe this time is different and this is the boom that will have no bust, but it should be obvious why people are looking closely at the data to see if and when rising boom times turn to flat and later to see if flat times turn down.