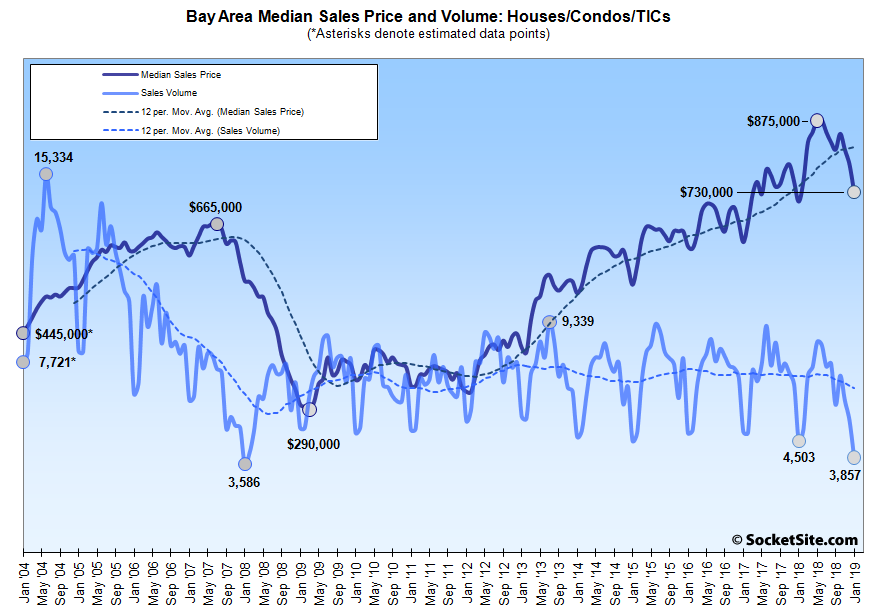

The number of single-family homes and condos that traded hands across the greater Bay Area totaled 3,857 in January, down 14.9 percent on a year-over-year basis. And in addition to representing another 11-year seasonal low, last month’s sales were an 11-year low in the absolute as well, according to recorded sales data from CoreLogic.

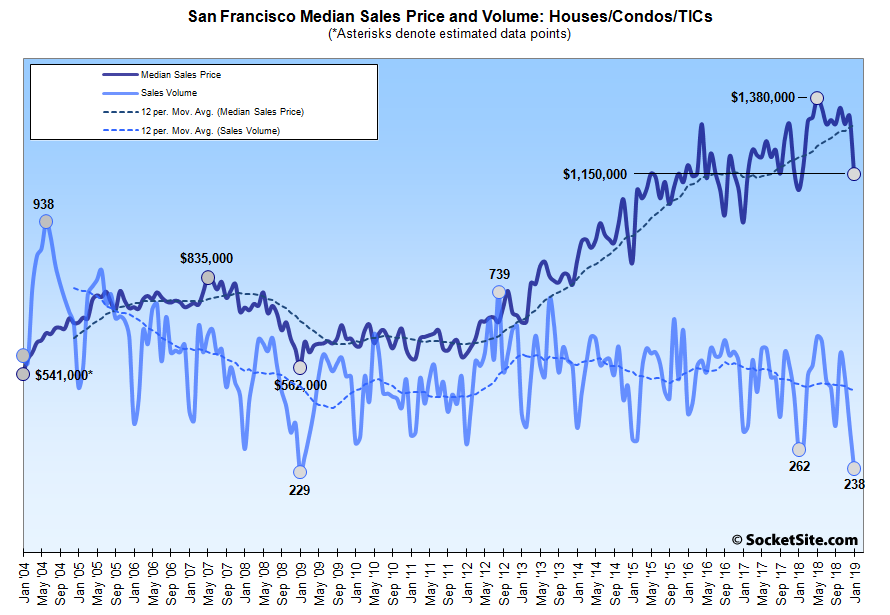

In San Francisco, recorded sales totaled 238 last month, down 18.5 percent on a year-over-year basis and a 10-year low in the absolute, which shouldn’t catch any plugged-in readers by surprise.

On the eastern side of the Bay, homes sales totaled 841 in Alameda County last month, down 10.3 percent on a year-over-year basis, sales in Contra Costa County totaled 742 (down 20.3 percent), and sales in Solano County totaled 363, down 10.4 percent versus the same time last year.

Down south, home sales in Santa Clara County totaled 803 in January, down 13.2 percent on a year-over-year basis, while sales in San Mateo totaled 288, down 8.3 percent versus the same time last year.

And up north, home sales in Napa totaled 77 last month, down 20.6 percent versus the same time last year, sales in Sonoma totaled 354 (down 10.4 percent), and sales in Marin totaled 141, down 5.4 percent on a year-over-year basis.

The median price paid for those aforementioned 238 homes in San Francisco was $1,150,000 in January, down 13.2 percent from the month before and 16.7 percent below last year’s peak but still 5.0 percent above its mark at the same time last year.

The median sale price in Alameda County dropped 12.3 percent in January to $732,500 in January and was down 2.4 percent versus the same time last year; the median sale price in Contra Costa County dropped 3.5 percent to $550,500 but was still 4.9 percent higher, year-over-year; and the median sale price in Solano County slipped 1.4 percent to $409,000, which was 1.7 percent higher versus the same time last year.

The median sale price in Santa Clara County dropped 2.0 percent in January to $980,000, which is 1.8 percent above its mark at the same time last year, while the median sale price in San Mateo County dropped 7.3 percent to $1,159,000, down 5.0 percent on a year-over-year basis.

The median sale price up in Marin dropped 9.4 percent to $920,000 in January, which was 0.5 percent above its mark at the same time last year. The median in Napa dropped 11.0 percent to $565,000, down 6.6 percent on a year-over-year basis. And the median sale price in Sonoma was relatively unchanged last month, inching down 0.1 percent to $594,500, which is 2.5 percent higher versus the same time last year.

And as such, the median home sale price across the greater Bay Area, which, in fact, has been trending down, dropped 7.0 percent in January to $730,000, which was still 2.2 percent above its mark at the same time last year but 16.6 percent below a peak of $875,000 which was set this past May.

Keep in mind that while movements in the median sale price are a great measure of what’s selling, they’re not necessarily a great measure of appreciation or changes in value and are susceptible to changes in mix, especially as sales volumes drop, as opposed to movements in the Case-Shiller Index.

All that being said, pending sales in San Francisco remain down while inventory levels are up. And the only excuse for perceiving the current market as being “random,” or prices having “surged,” is a fundamental misunderstanding of the underlying data and trends at hand.

bought in oakland at the peak, guess i better hodl!

Well, an 11 year low in sales is definitely an eye opening statistic. There is a delayed response between inventory building up and prices dropping. Price reductions will most likely accelerate through 2019.

Very interested to see how this all plays out. Stock market back up + mortgage rates back down -vs- some bad stats which may add the words ‘slowdown’, ‘peak’, or ‘decline’ in the minds of buyers. Which will win?

Are those the same “bad stats” that would have led people to believe the market was contracting; reductions were rippling through the market and picking up steam, with inventories on the rise; and that sales volumes were actually trending down despite the aforementioned increase in inventory levels?

I don’t understand your reply — or you are clearly constantly on the defensive with the bias in the writing. Bad stats in the comment don’t mean un-trustable stats, they mean stats for either a temporary time or a longer time (to be determined) that state the market is not just going up, causing would-be buyers to potentially double-take on the decision to buy. But that’s all to be seen with time

Got it. Our apologies for constantly being biased by actual analytics, versus feelings, and highlighting the emerging trends at hand. Speaking of which, did we mention that inventory levels are still ticking up while pending sales remain down?

Stock market still way down; fewer IPOs in SV, and the effect of Prop Tax not being tax deductible are all converging at the same time. Not the worst thing that could be happening and some price stabilization or even a decline could be just the thing that many side liners need to jump into the market. I think we see another 12-18 months of contraction as things shake out.

This. Also, lots of talk about a looming recession in 2020-21. Buyers a little weary of an unstable stock market after last year. A contraction might actually be healthy.

Good to hear eddy and denis agree on this. I know that both of you always have your eye on the higher end property market and have some insider knowledge about what’s going on.

Huh? “stock market still way down”? The S&P500 is down slightly over 5% from its all time high. How jaded have people become that stocks being 5% less then their all time high is “way down”.

“fewer IPOs in SV”

there are quite a few big ones happening in SF proper this year.

If you’re referring to Uber and Lyft they’ll be lucky if they even survive the year between IPO and lockup expiration.

Add Slack and Pinterest, and possibly Palantir, AirBnb, Instacart. That’s a f*ck-ton of value getting liquid this year, that will probably survive your snark.

All that said, the historical data doesn’t appear to support an “IPO effect” but it’s hard to tell whether SF would have fared measurably worse without the IPOs.

The problem here is one of easy credit. Having big IPO’s print new millionaires yet not one employee proving positive return on investment is a problem, a huge problem…

Why is that a problem? Amazon wasn’t profitable for many years and it seems to be surviving ok.

Companies often take a while to turn profitable. It doesn’t mean there’s a problem.

its not just credit. its real money.

you must be joking. this are multi-billion dollar companies with large operations and generating ton of revenue. investors do not want them to be profitable. the name of the game is growth and market share. once thats saturated, then they can pull back fpr profits. this is how how growth companies work.

Lyft wants to raise $100m and they lose that much every month. The IPO gives them literally one month to live. They’d have to triple fares to break even.

Is this really bullish, because lately it seems that IPOs are more of an exit strategy? The poster children of the Bay Area’s “new economy” like Munchery are falling by the wayside, what’s going to happen with that $8M commercial kitchen they built? Oh and 190 just laid off from Apple’s self-driving car division, I thought driverless cars were the next big thing? Elon Musk just took out massive HELOCs on most of his properties, hmm.

A lesson you can take away from the recent stock market correction is that when price goes up on low volume and atypical demand like stock buybacks, it creates air pockets where there is little demand on the way down. San Francisco saw a near “perfect storm” of foreign and tech funny money crazy bidding up prices for years, who exactly are the “sidelined” buyers waiting to catch a falling knife and pay those same prices?

Munchery is not a poster child for anyone. Look at Stripe.

The lesson to be learned from the recent stock market correction is that tariffs and trade wars have very damaging consequences to the economy. Trump pushed for both and now we have the result.

The market tanked because corporations, households, and government are groaning under the load of staggering debt and couldn’t handle the measly extra half point in interest rates at the time. Nor could the housing market, which was pushing the limits of affordability.

What market tanked?

The major indices fell 20% over three months (commonly referred to as a bear market). Until Steve Mnuchin called the President’s Working Group on Financial Markets on 12/23, Trump told reporters on 12/25 “We have companies, the greatest in the world, and they’re doing really well. They have record kinds of numbers. So I think it’s a tremendous opportunity to buy. Really a great opportunity to buy,” and last but not least, Jerome Powell’s pathetic dovish pivot which possibly destroyed what was left of Fed credibility. Regardless, I believe this was a “bear market rally” to be sold.

No. It’s the tariffs. And the government shutdown. And the deficit spending in the middle of a strong economy (the exact opposite of what you’re supposed to do).

We are all paying the price.

It’s likely we are in for a prolonged period of relatively subdued appreciation in the Bay Area – relative to some other major markets. Slower population and job growth in the coming decade will factor into this Places like Phoenix, Seattle and some eastern cities are growing 3 or more times faster than the Bay Area. This realignment of home prices is a healthy thing for the Bay Area going forward. Hopefully affordability will see a significant improvement over time.

Seeing as Seattle prices have apparently dropped 11% in 6 months, does that mean that the Bay Area has already dropped more?

I expect prices will drop slightly everywhere over the next couple of years due to the ongoing weakness in the US economy (assuming the president sticks with tariffs as a good idea). SF will do better than most places, since our economy is healthier than almost anywhere.

Well, on an apples-to-apples basis with the article and methodology you’re quoting, prices in San Francisco proper have dropped 15.4 percent over the past six months, with the Bay Area down 14.1 percent! Apparently everyone has stopped using smart phones and apps…

Did everyone stop using smartphones? I was not aware of that.

No. But someone once proffered: “My facts are that Apple and Google have an absolute duopoly right now on what is arguably the most important product in the world. They are generating inconceivable amounts of cash. Unless you think we’re all about to stop using smartphones, that gusher of cash will continue to flow largely to the Bay Area, where it will continue to support real estate prices.”

By the way, while the Case-Shiller index for Bay Area home values has dropped 2.5 percent since June, and the index for Bay Area condo values has dropped 4.2 percent, it’s actually up nationally (albeit by a nominal 0.5 percent), which is a bit troublesome if one’s rationalization for the Bay Area dip is “the ongoing weakness in the US economy” (and “SF will do better than most places, since our economy is healthier than almost anywhere”).

Which brings us back to the actual data, drivers and trends at hand…

Are Apple and Google not still supporting real estate prices?

That old thread is entertaining reading! People predicting an imminent bubble: “the Everything Bubble”, San Francisco’s population falling. Lots of great predictions. I think I’ll stick with Google and Apple still making lots of money.

But like you said, back to the topic at hand.

We can’t blame you for the deflection. But it’s like playing Jeopardy with Cliff Clavin. And while the data doesn’t support your core premise, that as long as people are still using smartphones, “SF will do better than most places, since our economy is healthier than almost anywhere,” we really can’t argue with the fact that those three people have never been in your kitchen< (or that Google and Apple still make lots of money, as the case may be).

The divergence between the national and SF trends is very interesting.

Unfortunately the moderation policy here makes it hard to have a discussion.

[Editor’s Note: Try staying on topic and adding some value, rather than whinging and whining, it really helps.]

“SF will do better than most places, since our economy is healthier than almost anywhere”

Presumably SS arguing that SF is doing worse than most places then, since you are opposing this premise.

Ok, then, lets review some numbers. By SS’s own statistics, SF’s unemployment rate in December was 2.2%. The United States was at 3.9% in December. I would suggest that 2.2% is better than 3.9%.

Apparently a family income of $117K is considered “low income” in SF, which is the highest figure in the whole country.

I’d be interested to see SS’s argument that SF is doing worse than most places.

And yet, while “the Case-Shiller index for Bay Area home values has dropped 2.5 percent since June, and the index for Bay Area condo values has dropped 4.2 percent, it’s actually up nationally (albeit by a nominal 0.5 percent).”

In fact, of the 20 indexed areas, San Francisco ranked last in terms of market appreciation in December. Or more accurately, it ranked first in terms of depreciation (down 1.4 percent). And on an year-over-year basis, San Francisco currently falls in the bottom quartile of performance and lags the national index by 23 percent.

And once again, all of which is “a bit troublesome if one’s rationalization for the Bay Area dip is “the ongoing weakness in the US economy” (and “SF will do better than most places, since our economy is healthier than almost anywhere”).”

Out of curiosity, why was my response deleted?

It wasn’t. It was flagged by an automated spam filter and since manually cleared.

I’m arguing that the SF economy is doing well. Are you trying to argue that SF’s economy is not doing well?

You appear to be arguing that SF real estate prices have fallen over the last year. Is that a response to Dave’s claim that SF would have “subdued appreciation”? It doesn’t appear to contradict what I’m saying.

What is Socketsite’s argument here?

Hasn’t your argument been that “SF [real estate] will do better than most places, since our economy is healthier than almost anywhere?”

And yet, despite the SF economy doing well, and Apple and Google continuing to make lots of money, the San Francisco market has not only declined, while the national index has risen, but the San Francisco market sits in the bottom quartile of indexed markets, in terms of performance, over the past year.

@SF Realist – the “subdued appreciation” over the next decade is driven or will be driven by macro factors. Not just the BA being one of the slower growing metros over the coming years but the change in the tech industry. With mini-tech hubs springing up (Boise for instance) which will absorb a growing share of tech jobs. SV’s share of the industry will fall going forward. Not to mention major centers such as Seattle, Austin and others which are more attractive to many employees than is the BA.

Yes, my argument is that SF’s economy is stronger than most places, so SF real estate will do better than most places. Now recently, yes prices in SF may have lost value in comparison with some other places, but that’s on the tail end of almost ten years of spectacular growth that was much, much faster than almost everywhere.

So I ask again: what is Socketsite’s position? Is Socketsite saying that San Francisco’s economy is weaker than most places?

Dave, the tech economy as a whole is growing. The Bay Area is the center of it and obviously as it grows the Bay Area becomes a proportionally smaller part of it. But the most valuable and profitable part of it is still the Bay Area.

Overflow areas like Austin and Boise have existed for decades as cheaper outposts. There’s nothing new there.

“prices in San Francisco proper have dropped 15.4 percent over the past six months”?

huh?

The Bay Area is pacing with the national appreciation trend. Give or take. No longer leading the pack as the region did for years. It is good to see price sterilization. What is better is to see price slowing in a market such as Seattle which is undergoing huge population growth. If the Bay Area had had less appreciation in the boom times things would not have gone to hell in a hand basket in terms of Bay Area quality of life.

How do you deduce that price appreciation results in diminished quality of life? Does appreciation not bolster city and county coffers?

Michael Kinsley actually answered your rhetorical question back in 2011. From Why do we continue to think that rising home prices are a good thing?:

Emphasis added. The context of that piece was the recovery from the so-called housing bubble popping, but almost all of it still applies today. Go read the entire thing.

The simple answer is that if you have a region which depends on a steady stream of new arrivals, and the Bay Area is that more than anything, then it’s better to have them spend less on housing so they have the room in their household budgets to afford to raise a family or enjoy the other things in life. Rapid price appreciation prevents them from doing that, and will ultimately result in diminished quality of life.

We can all agree that rapid price appreciation results in increased quality of life for real estate agents making a 6% cut of the rapidly increasing prices.

@Brahma – Exactly. The large price appreciation in the BA has gotten to the point where it hurts the region in attracting talented labor. Even with a tech job one can often barely afford to break into the housing market. If one is lucky enough to do so it often means homes on the periphery with the associated very long commute. Seattle does not want to repeat the mistake of the BA re: housing and rents becoming generally unaffordable. The strategy to avoid that has been to build huge numbers of new units each year – something they have been doing for almost a decade and continue to do. For the moment the effort to keep a lid on prices there seems to be working with significantly slower home appreciation despite huge population and job growth. The BA never made that effort and really still isn’t so doing despite lip service otherwise. The price stagnation the BA is experiencing is to a large degree the hitting of a celling in prices. A point above which very few, even among the well paid, can afford to go.

Right. Price appreciation causes sectors to be unable to afford to purchase housing. That was not the question.

What about the point though, quality of life? I will answer my own question. We’ve seen a doubling down on roommate culture. But is that a truly bad quality of life? It’s actually utilizing housing in an efficient manner. Is it a poor quality of life, really?

Are areas where housing affordability is more widespread also places with high quality of life?