Purchased for an “over asking” price of $1.45 million in early 2015, the ClockTower loft unit #C322 at 461 2nd Street returned to the market this past April listed for $1.395 million or roughly $915 per square foot.

Reduced to $1.3 million in June, the “sophisticated top floor live/work loft” with “generous space to entertain” and a “spa-like master bath” was then relisted anew for “$995,000” last month, a sale at which would have represented a 31.4 percent drop in value for the South Beach condo since early 2015 but an “over asking!” sale if it closed for a dollar more.

And the resale of 461 2nd Street #C322 has now closed escrow with a contract price of $1.25 million, which is officially 25.6 percent “over asking!” but a 13.8 percent drop in value for the unit since February 2015 on an apples-to-apples basis.

Not having a real bedroom hurts this unit. IMO, a better configuration of the existing space with one real bedroom, and a second loft bedroom could have fetched a better price.

i don’t think that’s a viable “alternative” with respect to your suggestion for bedrooms. the whole thing about these “lofts” is that they are what they are because they wouldn’t meet the code if it were any other way. in this case there are no windows at the loft nor any of the side walls to create bedrooms with.

i’m so sick of the over asking metric. the only data point that matters is the sales price. we see that this unit sold for $1.25m today, which is a big drop since the last sale in 2015. those points matter. as a buyer, i’m really tired of this stupid industry stat that provides no value for buyers.

No value to anyone else either. I agree 100%.

supposedly it provides value to real estate agents. it gives them a point to market, but i’m not exactly sure who is falling for it. the bay area real estate market is fairly sophisticated, but i guess with the right spin, you can make anything sound good, even a pointless stat.

No, it’s all marketing hype, like “only on the market one day” ploy. If it’s offered 30% below what it last sold for, even if market prices have dropped a bit, of course it’s going to sell “over asking.” Might as well slap a $1 sign on every property.

It’s a mistake to think that real estate agents, or salespeople in general, “know the market”. What they know is what prospective customers want to hear.

If you stop trying to tie what they are currently spinning to the market reality and instead use it to get a pulse on the desires of the buyer pool you’ll find much more utility with what they have to say.

A parallel is to stores that have their merchandise constantly “on sale”: i.e. for those who don’t do due diligence it provides evidence – false, but reassuring perhaps – of something (“value” in the one case, rising prices in the other).

As for whether it really matters or not, apparently it does to the one person who counts…the editor.

yes please, SS: please stop trying to mock the “over asking!” BS. everyone, especially the SS commentariat, knows its BS.

“(“value” in the one case, rising prices in the other).”

That’s the key realization here. I do think that most members of the general public are misled by the over-asking ruse and mainstream media greatly aids this misconception. But looking deeper this begs the question of why does the industry go to such lengths to fake rising prices vs the more common “on sale” ruse of faking falling prices.

And the answer is that they are salesmen spinning a story that their customers want to hear. And during the upswing of a boom what people increasing want is price momentum, the perception of rising prices.

And it’s also very easy to see why a momentum based market is less stable and more cyclical than a value based market.

When rising prices increase buyer interest, the added demand feeds back and further increases prices, further increasing buyer interest,…

But when momentum fades with prices at too high a level to attract value buyers, this cycle reverses.

And when buyers can come from across the globe into a “hot” market and can lever up either due to loose lending or low interest rates, these cycles can become extremely large.

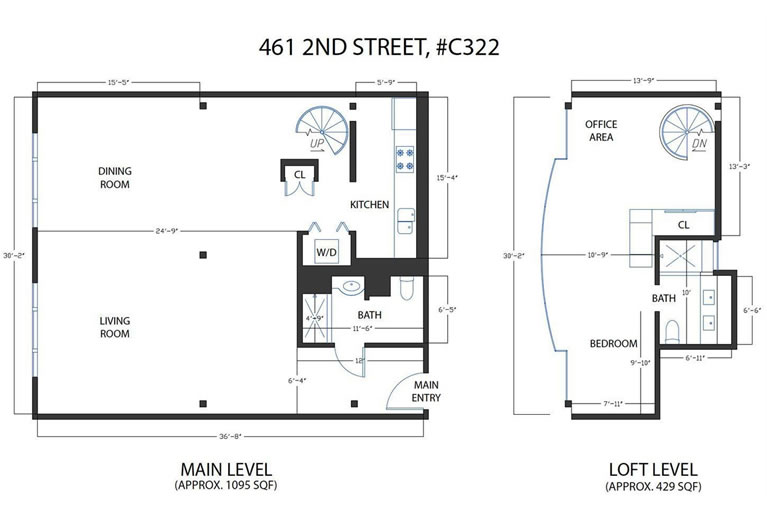

If I’m reading this floor plan correctly, to use the right sink in the upstairs bath room you have to be darn-near to standing in the toilet. Interesting feature for a “spa-like master bath”.

At first I thought “why have 2 full baths” but I guess if you’re going to go through the expense of putting in a half bath, and have the room, why not add a shower. Can always serve the guests on the fold out sofa in the main space.

That’s not a toilet, it’s a “foot spa”.

The RE peak seems to have been in late 2015/early 2016. That was the period of irrational exuberance which led people to pay exorbitant prices for mediocre places such as this. The “luxury” Lumina Towers got caught up in this too – and now they are seeing price reductions on re-sales. Many entitled projects have been put up for sale ( about 920 units worth) and again, these projects were planned often just prior to this period with the assumption that double digit gains would continue indefinitely – or at least for as long as it would take to build the projects out. That kind of appreciation has come to an end and many of these projects simply don’t pencil. 524 Howard will be one to watch in this regard. As for entitlements in play, their investors will likely have to take a loss to “dump” the projects just as the owner of this unit had to take a loss.

Other segments of the marketplace look stronger than 2015.

Except the evidence doesn’t support your point. Case shiller numbers just came out today showing SF condos up in price 10% since late 2015. So that’s the broad measure. 1438 Green 5A, closed yesterday at $1,420,000 after selling for $1,278,000 in December 2015 (up 11.1%). 1040 Masonic #3 sold yesterday for $920,000 after selling for $800,000 May 29, 2015 (up 15% since mid-2015). Yeah, there are outliers, like the place in this post. Don’t be fooled by cherry-picking – a rookie mistake. If you think you can buy a place in SF at a discount to late 2015/early 2016 prices, good luck with that.

Prices may indeed fall. But they certainly are not presently below late 2015/early 2016 prices. There was a little bit of a “false positive” in late 2016 that quickly passed with prices turning upward again. Supply remains very low, and demand remains very high.

And once again, you continue to conflate the broader measure of condo values across the San Francisco Bay Area, the segments of which aren’t moving in lockstep, with what’s happening locally.

Speaking of which, based on recent comparable condo sales around the ClockTower, rather than in Russian Hill or Haight Ashbury, Redfin is currently estimating the market for this unit peaked around the end of 2015 (sound familiar?) and has since dropped around 7 percent.

But we have to admit, they did do a nice job of remodeling your apples-to-oranges anecdote on Green Street between the sale in 2015 and yesterday.

Folks forget that. These CS numbers are for the Bay Area as a whole but even “locally” all real estate is local. As I recall Oakland has had near double digit appreciation and several counties outperformed SF. If the region is 6.1% for the year and other areas are doing better than that then SF is actually up less than 6.1%.

My belief is the whole BA will track national numbers because of all the issues here surrounding quality of life issues. Within that, parts of the BA will lag national numbers and it’s a fair bet SF might.

Please. The conflating is taking a handful of cherry-picked results and calling that “the market” while ignoring the vast majority of resales.

And my apologies as I didn’t realize you were, apparently, saying no more than that condos near the clock tower peaked two years ago while everything else in SF has continued to rise. I misread your post, it seems.

I believe and continue to that SF real estate will now track national numbers in terms of appreciation – for an extended period. Today’s CS report confirms that is what seems to be happening. New construction condos are down a small amount and that ties into all the entitlements in play as those with invested money realize the lower appreciation does not warrant building at this time.

I am not cherry picking – appreciation has leveled off. I would not invest in SF RE – got out in 2014 – so I’m not looking for a deal at below 2015/2016 prices and even if I found one I would not purchase it. There is more money to be made in other markets over the next 5 – 10 years..

You’re not cherry picking. The editor of this site is.

Consider though that this property, as with many others featured on this site, was spotlighted *before* the outcome was known.

Contrast that to the sales that you cherry pick, many of which get debunked as being “rotten apples”, that are picked *after* the outcome is known.

We are often reminded that you got out in 2014, but have you considered whether that was the right call? You missed a ton of appreciation after that and, if you traded over into properties in Washington or Oregon you are also paying property taxes on those properties that you would not pay in California thanks to prop 13. Given our property tax rules, it rarely makes sense to sell an appreciated property unless you need the funds or can accurately predict a CRASH, not a slowdown. I know that you believed that 2014 was the peak at the time, but we now know it was not.

It was the right call. I didn’t think it was the top – no one can time the markets whether stock or RE. The signs were there in terms of future population and job growth and migration patterns that the NW would be a RE goldmine for the coming decade plus. Ironically, I inadvertently exchanged at the right time as a year later Seattle and Portland took off gangbuster in terms of appreciation – much more appreciation than if I had held onto the California properties. Plus better ROI.

Selling an appreciated asset is indeed often warranted – to hold and hope is not usually a wise strategy. Investors are getting out now and have been for a year or more. The sudden increase in “in play” entitlements is no random event. The slowdown and scale back of the Giant’s MR project is very significant though many are not looking at it that way. It’s part of a confluence of events that portends an extended sluggish period for SF RE. Not a crash – not something I believe will happen short a major external event such as a large earthquake.

Just $1,250,000 to be 12″ from I-80. What a time to be alive.

… and no real bedroom or kitchen to boot. But you get to live in SAN FRANCISCO!

It is nonstop noise down there and car horns. And greasy dirt from tires and exhaust that settles back a day after cleaned –floors, sills, surfaces. Hope the unit has AC. Keeping windows open is out of the question.