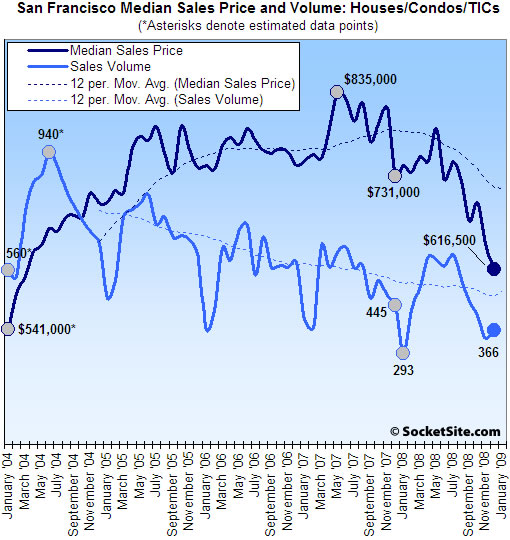

According to DataQuick, home sales volume in San Francisco fell 17.8% on a year-over-year basis last month (366 recorded sales in December ’08 versus 445 sales in December ‘07) but rose 7.6% compared to the month prior. San Francisco once again recorded the sharpest year-over-year decline in sales volume of any Bay Area county last month with Marin a close second (down 14.5% YOY).

San Francisco’s median sales price in December was $616,500, down 15.7% compared to December ’07 ($731,000) and down 4.9% compared to the month prior.

For the greater Bay Area, recorded sales volume in December was up 36% on a year-over-year basis and rose 19.7% from the month prior (6,889 recorded sales in December ’08 versus 5,065 in December ’07 and 5,756 in November ’08), while the recorded median sales price fell 43.8% on a year-over-year basis, down 5.7% compared to the month prior.

Once again, think foreclosures and mix.

Homes that were foreclosed on accounted for 50.0 percent of December’s resale activity, up from 46.8 percent in November, and up from 14.0 percent for December a year ago. Foreclosure resales ranged from 12.4 percent in San Francisco last month to 67.7 percent in Solano County.

At the extremes, Solano recorded a 103.6% year-over-year increase in sales volume (a gain of 373 transactions) on a 42.3% decrease in median sales price, while Contra Costa recorded a 84.1% increase in sales volume (a gain of 817 transactions) on a 50% drop in median sales price.

And as always, keep in mind that DataQuick reports recorded sales which not only includes activity in new developments, but contracts that were signed (“sold”) many months or even years prior and are just now closing escrow (or being recorded).

∙ Bargain hunting dominates Bay Area home sales in December [DQNews]

∙ San Francisco Recorded Sales Activity In November: Down 29% YOY [SocketSite]

I know most people on here are only interested in SF proper, but this caught my eye:

“The median price paid for a Bay Area home was $330,000 in December. That was down 5.7 percent from $350,000 for the month before, and down 43.8 percent from $587,500 for December 2007. That was the lowest it has been since March 2000 when the median was $320,500, and 50.4% below the $665,000 peak of June/July 2007.”

I’ve been waiting to see a -50%+ print for the area as a whole, and I didn’t think we’d see it so quickly (18 months after peak).

Is there a map of the locations of the 366 recorded sales in Dec? With info for asking vs actual selling price?

Nice chart!

If there was any room to debate the trend line in late ’07 that debate is over now.

I found this to be the most interesting part of the DQ report: “Homes that were foreclosed on accounted for 50.0 percent of December’s resale activity, up from 46.8 percent in November, and up from 14.0 percent for December a year ago. Foreclosure resales ranged from 12.4 percent in San Francisco last month to 67.7 percent in Solano County.”

So the % of SF sales that are foreclosures is just about where the Bay Area as a whole was a year ago, and about 4X where SF was a year ago. I don’t know if a year from now 50% of SF sales will be foreclosures but it is a safe bet that it will be way, way higher than 12.4%. Once again, SF is following right along with the parts of the state that have been whalloped the hardest, just about 12 months behind.

Since it looks like we will pierce through the 2004 levels any time now, we really should be looking at a longer term graph to understand where the bubble began and guess about potential undershoots.

It is a very San Franciscan lanscape: think Telegraph Hill between Montgomery and Sansome.

“I know most people on here are only interested in SF proper.”

False. Real SF is all that matters.

It’s interesting to see the seasonal price variations. Seems like the best time to buy is in the fall/winter and the best time to sell in the Spring.

The Spring surges of yore are a thing to behold! Look at the 04 and 05 Spring surge in median prices. Then pretty much each spring thereafter there is less of a surge. Maybe 09 is the first year we don’t see a Spring surge?

And following up . . . .

The Spring Surge of 07 was a big one. Sandwiched between a few ho hum spring surges.

What’s amazing is how foolish the banks still are.

So now they require 20-30% down?

At a drop rate of 4.9% per month, that’s going to get wiped out in 6 months!

Medians aren’t prices, but if I were the typical SF homeowner who bought last year with 10% down (the requirement for a year ago), I’d be thinking I had lost the entire downpayment and was paying a mortgage that was more than my home was worth.

@tipster

true, that 20-30% down payment can (will?) get eaten up in 6 months, but I would think that the majority of people who put down that kind of down payment will not turn around and default in less than a year. The vast majority of them will ride it out. Yes, some will lose jobs, etc. But with that kind of down payment, I don’t think the banks are taking an unreasonable risk. They are, after all in the money lending business (at least in theory. 😉

“So the % of SF sales that are foreclosures is just about where the Bay Area as a whole was a year ago, and about 4X where SF was a year ago. I don’t know if a year from now 50% of SF sales will be foreclosures but it is a safe bet that it will be way, way higher than 12.4%.”

Uh….actually I wouldn’t say that’s a safe bet at all. This is the same logic that 3 years ago, said prices were going up at 10% a year, and it was safe bet to assume this would continue. I’m not making an argument on this one way or the other, as I don’t think there is enough data to definitively support either side. With that said, looking at the current trendline to support ongoing behavior is what got us into the mess.

“if I were the typical SF homeowner who bought last year…”

Actually, the typical SF homeowner probably still delusionally thinks their place has appreciated or held it’s value since last year. I know that MY condo is up this year despite the identical condo upstairs selling for less than in ’05.

Seriously, though, I’m curious what spring brings. Obviously I don’t think there will be a bounce, but I’m wondering if there’s a flood of new listings when folks realize it ain’t stabilizing anytime soon, and they try to get out before we run out of lifeboats. In other words, will primoland inventory explode, or will it continue to be managed by the real estate cognoscenti, as mentioned on the other thread?

Housing will almost certainly go down another 20-25% in SF, but I don’t think the banks are necessarily being foolish to lend with 20-25% down payments.

They know that buyers on average are unsophisticated and loss averse. Once they plunk down the 20-25% (this is big $$ in SF), they’ll be trapped there, paying their mortgage month by month while their wealth is siphoned into the pockets of the banksters. Sure, a job loss or relocation could cause a realized loss because the house must be sold, but the incidence of these can be estimated, there is some profit to the bank in the lending spread, and loss severity in the event of foreclosure will be reduced by the down payment that the market will have chewed through.

Now, about those buyers being foolish…..

When it comes to pass that they are indeed trapped by the market, they’ll tell themselves it’s not a real loss until it’s sold. And keep paying. And they’ll point to the stock market and point out how a “paper” loss there for someone who has a 30 year horizon is somehow very different from a “paper” loss on real estate that they thought they would sell in 10.

^^^

Plus they got to live in it!

“Once again, SF is following right along with the parts of the state that have been whalloped the hardest, just about 12 months behind.”

I agree that right now SF lags by 12 months, but now we have proof SF isn’t immune, and we know how much further there is to go down–A LOT. My guess is pretty soon the lag will only be 3-6 months.

Prices will drop at a faster rate in SF than the rest of CA. Because who is gonna put down 20-30% to buy a house when there’s proof this money will be completely wiped out in a year or less. No buyers, means lower prices.

Lance,

It’s an ESPECIALLY safe bet that there will be way more foreclosures because there was a statewide foreclosure moratorium in November and December.

As dire as things are getting, though, I wouldn’t be surprised to see the Obamatons propose some kind of national foreclosure moratorium for a year or longer. It may comes close to infringement on contract law and further zombify the banks, but I bet it (or something equivalent) happens. No stopping this snowball now, but more taxpayer money must be wasted to give the appearance the government is “doing something” or “looking for a solution,” etc.

“…there was a statewide foreclosure moratorium in November and December.

There was? I never heard about this.

Do you know how many homes were saved from foreclosure?

I wonder if Obama will do a nationwide moratorium? He seems very keen on “stabilizing” prices (keeping them inflated). And subsidizing mortgage rates.

This could cause a seller to wait to list their house…hoping the Government will come and save the day.

Mix continues to distort these figures,to the extent that the median is rendered totally meaningless.

No district other than d10 with any semi-sensible SFH sales data (above 5) shows a YOY drop of above 10% – and shows a rise in 2 districts.

also from

http://www.rereport.com/sf/ron/

SFHs are actually down 12.5% Yoy (with the mix a big factor) and condos 9.3% YOY.

I am kinda baffled how that equates to the 15.7% shown here from dataquick.

either way, it shows the total unreliability of one overall citywide median price.

The editor says “Once again, think foreclosures and mix.”

So, you could interpret that to mean that if sales weren’t so heavily skewed toward foreclosures – prices would be down by some smaller amount. I’ll be the first one to say that using one month (especially January) to extrapolate prices as a whole is a mistake. With that said – there is clearly a premium for financing in the upper-end of the market, the % of foreclosure sales is much higher than foreclosure inventory (i.e. – a shift into bottom feeding), and down payment requirements for jumbo loans are at least 20%. This would all suggest that mix is impacting these numbers negatively, and prices really aren’t down as much as these stats would indicate. That’s my interpretation at least, but I’d love to hear some reasonable arguments to the contrary.

I came in here to say what Jay said-

It would be nice to see a 15-year graph. It would also be nice to see how housing did in the last recession (the post-dot com notwithstanding, since housing was the recovery mechanism there)

[Editor’s Note: It’s slightly apples (median) to oranges (mean), but a couple of graphs to get you started: San Francisco Home/Condo Sales: Historical Context and A Decade Of Movement In San Francisco’s Mean Sales Price.]

Mix this, mix that. It’s all pretty irrelavant for your average homebuyer or seller.

Forget about rearranging deck chair on the titanic.

“Mix this, mix that. It’s all pretty irrelavant for your average homebuyer or seller.”

Oh yes, you might be on to something. Taking median price changes as fact, when there are so many underlying changes underneath the covers makes much more sense.

Wow….I don’t know how I could have missed that one 😉

I found some very interesting data in a report that was written by T2 Partners in NY. A whole lot of information can be found here on historic price to rent ratios, lending standards, bubble history etc.

http://www.calculatedriskblog.com/2008/12/t2-partners-why-there-is-more-pain-to.html

rational renter wrote:

> I found some very interesting data in a report that was

> written by T2 Partners in NY. A whole lot of information

> can be found here on historic price to rent ratios, lending

> standards, bubble history etc.

http://www.calculatedriskblog.com/2008/12/t2-partners-why-there-is-more-pain-to.html

I’ve met Whitney at T2 partners (he was in the same HBS section as one of my fraternity brothers) and he is a sharp guy. I don’t think I have met anyone else where more people have told me “he is the smartest guy I know”…

“…there was a statewide foreclosure moratorium in November and December”

http://2.bp.blogspot.com/_4ZgohmRDQmI/SW2ycN_Ox_I/AAAAAAAAAT0/q3TgCZKNWyI/s1600-h/ForeclosureRadarREODropDec2.jpg

nott rue

Umm, pretty sure it was “t rue” to some extent:

From LATimes, November 10, 2008:

As part of his plan to spur the California economy, Gov. Arnold Schwarzenegger announced last week a belated but welcome effort to keep more troubled borrowers in their homes. Now we’d like to see the governor follow through by pushing the Legislature to turn his proposals into law and making sure that lenders deliver the relief.

http://www.latimes.com/news/opinion/editorials/la-ed-moratorium10-2008nov10,0,5107428.story

You are right – I was sloppy. The moratorium ended at the beginning of December. (It wasn’t really a moratorium, it just added a 60 day waiting period that pushed everything out).

However, the effect was to hit SALES of foreclosures in November and December.

You’ll see them tick up again this month.

Foreclosure “moratorium” is not the right word. A new law passed in September ’08, SB 1137, added a 30-day “waiting period” and put in some other procedural hurdles before some foreclosures could be instituted. This stretched out the foreclosure pipeline and reduced the number of new foreclosures for a few months in late 2008. The (now longer) pipeline is now filled again and the numbers are picking back up and rising. I.e. this just delayed things a bit. So the numbers for December were artificially lowered.

The moratorium was/is real. Here’s an SF Business Times article from November of ’08 when Fannie and Freddie announced it. It originally ran through January 9th.

http://www.bizjournals.com/sanfrancisco/stories/2008/11/17/daily83.html

The day before it was to run out, they extended it through the end of the month:

http://www.fanniemae.com/newsreleases/2009/4575.jhtml?p=Media&s=News+Releases

As I wrote above, I’m betting they’re waiting for the new administration to announce it will go on for the rest of the year or longer. Keep in mind this is only on loans held by Fannie or Freddie, so other lenders can still foreclose.

You are all too negative. The market will stabilize in San Francisco by the 3rd quarter and values will go up next year.

What do you base that prediction on, Money Man?

His bong told him.

Solano sales are up 100% with prices down 40%… which means a lot of people are snapping up the cheap stuff… and so obviously median and average prices go way down – which does not necessarily mean the million homes there are now selling for $600k.

In SF… more or less the same statistical issue… there were a lot more D10 sales than D7 sales… and D10 is where the majority of foreclosures are with a smattering in SOMA and a couple of other areas. D10 homes selling for $400k when they had been $700k is killing SF stats, especially when moneyed buyers in D7 (and the like) are taking a wait and see approach on the stock market and their jobs.

And I have news for you folks… the D7 types put 40% to 100% cash down when they buy (not all obviously, I am over simplifying here – but many, many more than I’d expect you’d imagine given the comments on SS). This is why D7 or “real SF” won’t drop any where near what the biggest bears predict – it’s already taken a 10% haircut or so simply because some needed or wanted to sell when there was little buyer activity… but many, many D7 and Noe Valley sellers will rent (or let it sit vacant if they have to move and are really well off) or stay put until the market returns… and with 40% to 100% equity… they will wait as long as it takes.

No supply combined with stubborn Sellers who can afford to wait will continue to keep “real SF” prices from dropping much beyond where they’ve already dropped.

Of course with conforming loans at 5%, look for 1BR’s to get snapped up (plus more distressed Sellers at the low end even in D7) thus pushing the median and average prices down… giving fodder to socketsite bears… yet anyone who REALLY wants a D7 Single Family is going to have to pay the least stubborn Seller THEIR stated price… which won’t ever… and I mean EVER… reach 40% off levels.

It part of my Obamamania.

Whitney may be a smart guy but one can’t tell from his housing presentation. It was very late to the party, lots of other folks made the same points more than a year before T2. Most of the deck relies on other’s analysis and it displays almost no original thinking.

REporn – Overall median can decline faster than either SFH or Condo median if mix shifts towards condos (which are cheaper than SFHs).

District by district medians, however, are not necessarily any more or less accurate than overall medians.

The 50% drop in the D10 median is clearly a function of the large share of foreclosures there (i.e., big change in mix). Foreclosures tend to be cheaper homes, so the D10 median change almost surely overstates the average drop in price for a D10 home.

The smaller declines (or increases) in the D1 and D5-D9 (“real SF”) are going to be, if anything, positively affected by mix (almost no foreclosures to boost low-end sales, and as the market falls it gets harder and harder to sell flawed – i.e., cheaper – properties). They’ll also be positively affected by the fact that the only way you can make money now as a recent buyer is if you have improved the property. So for these districts, the median almost surely understates the average drop in a price.

One statistics that has unambiguous implications for prices going forward is a drop in sales, however. The figures you link to are quite shocking – sales in “real SF” (which I’m defining as D1 + D5 through D9) have dropped an incredible 45% over the past year.

For reference, sales in CoCo dropped 18% from 2006 to 2007 and sales in San Diego Co dropped 35% from 2005 to 2006. It took one to two years, however, before (median) prices started dropping rapidly in those areas.

I partially agree with you, sfrob. Prices may indeed fall 40% from peak – that is to say, bids offered for homes may go to that level. But if people don’t have to sell and refuse to take that bid, we won’t see the 40% hit reflected in actual sales numbers. Could happen.

But keep in mind that D7 and Noe Valley comprise…what, like 2 square miles of our 49? And what % of the local population can afford a $2MM home anyway? 5, maybe 10%? I guess my point is that, even if you’re right, the rest of SF is much “realer” to most of us anyway.

sfrob – What evidence do you have that D7 types put 40%-100% cash down? Just curious….

We’ve already seen some D7 comps or listings that are demonstrating major haircuts. -40% from peak prices is certainly not out of the question. Green St view property that I’ve brought up before. $2.75 recorded sale for view home fixer. The currently gutted and framed out SFH on Pacific that was bought for over $4M and is now asking $3.5 and remains unsold are 2 examples.

More prime listing in D7 on the way. Malin will be testing the waters with 3355 Pacific for $8.9M and they have 2830 coming on for $15ish in April. These will be good judgements for the market.

@sfrob and dude: Anyone who believes that a market clearing price is set by the “stubborn seller” even in the pricier sections of SF doesn’t understand how markets work. The market price is determined by what a bidder is willing to pay. Your thesis is based on the idea that that the average rich guy is flush with cash, doesn’t need to sell, and is looking to buy another property. I, however tend to believe that the opposite is true: A year ago, the average rich guy was printing cash working at a hedge fund, a private equity fund, a real estate development firm, google etc. They probably owned several properties, were heavily invested in the stock market and/or hedge funds, and kept very little cash because their financial planner told them it was inefficient. It was incredibly easy to get financing to buy yet another house if he/she wanted one. Fast forward ahead a year. This same rich guy is not getting a bonus because returns in his fund were negative, his stock options are below water etc. His investments have been pounded and he can’t get his money out of a hedge fund because the fund has put up “gates.” He has very little cash and high expenses because he was overextended and really needs to downsize. Even if he wanted to buy another house, he wouldn’t be able to get the financing without a huge down payment.

Who are the potential buyers in the market now? Anyone who patiently saved their money and didn’t live beyond their means. They hoarded cash, and were very short the market in the past year. These people are few and far between but they are out there, are ready to buy a house and have the means to do it. These people will set the price. And let me tell you something, they will not be paying the asking.

Well said, k10.

Buyers set the price in every market. Always.

I could care less about sellers’ preferences or feelings. I love it, though, when their need for my money exceeds their desire for their assets.

Recessions and depressions (or market wipeouts) are the mechanisms by which capital is returned to its rightful owner.

K10,

Couldn’t agree more. We’ve seen far more problems with our high end clients in the past two months than any other client demographic. Most seem to be over-leveraged in their businesses and in their RE purchases. Currently 3 of our existing clients are selling multiple RE properties to cover business expenses. About a third of those properties involved would be considered the “real SF”.

By that logic and technicality — it’s Bono Vox aka Paul David Hewson. OK?

“D7 puts 40-100% down…”

Um…they might not need a bank loan per se, but, um…they need their investments, which are also down the tube…let’s see…I have heard people put their money, prior to this mess, in: Gold, Euros and, stocks they thought were going to hold steady…um…hello!!!!

well, I’m just one little guy with anecdotes of my clients and of my closest colleagues… but I haven’t had any of the “average rich guy” described by k10. I know they exist, but it seems like they are more prevalent in SOMA and outside of the city… and I’ve only stuck my toe in SOMA in the past 6 months as prices finally started looking realistic.

My apparently “not average” rich guy clients were all shopping for primary homes, paying 40% to 100% cash, and usually told me something along the lines of “well, I’m willing to go up to $4 million, but I only need xyz” and xyz usually had me looking in the $1.5 to 2.5 million range.

I also don’t disagree that Buyers are the ones who set prices… 99% of the time. But don’t we have a diamond industry where the sellers control supply and therefore price. How much will they drop in this market? (i’m a econ drop out so pardon my anecdotes).

The only way LMRiM will be right about ALL of SF (including luxury Russian Hill, Pac Hgts, Cow Hollow, etc) is for half the city to be on bread lines. And since I’m pretty sure that is what LMRiM’s prediction is based on… then I’ll agree…. that is to say that if we see the great depression 2, then yes, D7 will take a major hit.

I would characterize myself as what K10 would call a potential buyer. I’m a young new money person who has kept much of my wealth in near cash mostly out of laziness. I’ve been casually looking at buying though definitely taking my time.

And there is now way in hell I’m offering anywhere near asking. And from what the realtors showing the places are indicating to me, there are definitely deals to be had.

sfrob,

I believe that D7 will suffer a big hit and that it doesn’t require 1/2 the people in the breadlines.

My theory? Those are sophisticated investors that now know where the market is likely to go: A cliff drop followed by a long flat line.

A middle class guy can boast he can wait it out to keep his chin up. A rich guy can say he took a few millions in losses and still keep his chin up, as long as he keeps the bling apparent. Au contraire, how much loss you take without blinking an eye shows how strong and solid your situation is to your social circles.

In short, they know when to hold it, and they know when to fold it. Smart investors know how to take a loss and move on. Only the sheep keep their dead money thinking “buy and hold” is still the name of the game.

DOM,

I absolutely, wholeheartedly agree. We don’t need a Great Depression #2 for prices to go down.

But, I don’t believe all people are about playing a game in public. There are plenty of people in this city who are monied and have no desire to let others know whether they are keeping their chins up or not…mind you, letting others know that they even have a golden lining in their wallets. That might be your circle.

Whatever…this spring will be interesting…bloodbath or not…

Odd that neither Fluj nor Paco posted on such a grand day for RE announcements on SS.

It looks like statewide we are seeing volume pickup as investors are buying foreclosed properties at attractive prices. if we see a couple more months of increased volume it would signal a bottom at the low end of the market. The recovery will start at the low end of the Market.

I am not predicting this will happen but if the trend continues it will have a stabilizing effect on banks.

As soon as the banks started requiring substantial downpayments, the number of sales dropped like a rock. So I don’t think there are as many people as you may think who have that kind of money down. And lots of people who did refinanced and took cash out.

I don’t know anyone who put down one cent in a D7 property and I know 8-10 D7 buyers from 2004-2006.

k10

I join Jorge and LMRiM in agreement with you. It was very well put. One piece in the NYTimes recently stated that “high end” real estate clientele has shifted from hedge fund and money market folks to a previous generation’s economic titans – doctors and lawyers.

Though I would never want to live in D7, I certainly want to hear more anecdotal data re: where the market in that area is going. If they’re hurting, then prices in SF are coming down…way down. So sfrob and others, keep those anecdotes coming!

Jorge,

One is too busy with his sales, and the other one is too busy refreshing SS to check on posts from his mentor so that he can comment a follow-up post.

tipster,

20% downpayemnts mean a big capital risk. Not many candidates nowadays for this gamble. I have a friend in Sunnyvale who bought in 2007 and has now seen his 30% downpayment eaten up by the loss in value (one foreclosure a block away for a similar house sold for 40% of what he paid). He still has the big MoFo mortgage though but no equity. He’s rationalizing the virtual loss of his 10-years savings’ worth going down the drain and his 401(k) sucks too. He can’t save any more because of the house payment, btw. I told him to wait, but nobody listened to bears 2 years ago.

138 DOM- i don’t see owners falling all over themselves to sell their homes to avoid the catastropic price drop you are predicting. And frankly, if we were all that rational no one would ever buy in SF since a catastropic earthquake is at least as likely as your price scenario… humans do strange things aye?

r_gee – sounds like some agents are trying to impress you so as to get your business… and while there will be “deals” they’ll be relative to pre-Sept crisis time… not 40% off deals

recent anecdotes… 2037-2039 Jefferson St got 21 offers a week before xmas… 246 2nd St #1003 got 4 offers the day after xmas…. well priced homes now are getting a TON of attention… so clearl not everyone is as pessimistic as SS commenters.

I started posting 10 months ago. Since then the rationalizations have been:

1 – It’s subprime only

2 – It’s East Bay only

3 – It’s East Bay and Peninsula and Bayview only

4 – It’s the non-primo SF

5 – It’s non-D7

6 – D7 is taking a hit but not really a panic

Will it stop there?

I don’t think so. All these rationalizations have been wrong so far and I’d bet this market will surprise even the bears (I am surprised by the speed of this correction, not by the depth).

As I said earlier, this reminds me of Union Street starting at Washington Square. You go up and up and up . When you reach Montgomery you plateau and think the slope will go down slowly towards the bay, and then you hit the cliff…

Offers are indicative of nothing. Most of the offers are under asking. Some by a lot.

246 2nd street was asking $600 psf for a high floor condo in great condition.

I don’t know what Jefferson Street was asking, but a 2-unit on Scott Street just sold for $430 psft. 2006 sale prices on similar properties was 650 psft. At $430, there are going to be buyers.

http://www.zillow.com/homedetails/3551-3553-Scott-St-San-Francisco-CA-94123/15079826_zpid/

In any declining market, there are plenty of buyers. Doesn’t stop prices from declining. People bought all the way down in Stockton.

I haven’t been posting a long time on here… but I guess I’m Custard making the last stand. Since I’ve got no history on this site I can’t prove this… but I’ve always been in the camp that SOMA/SB/MB pricing was absurd… I called it the “new car” concept… as soon as you drive it off the lot it depreciates 10% since next year everyone will want that year’s model. So why not buy last year’s model? Everyone told me they liked the new stuff… so I said “great, then wait 1 year and then buy what you like today”.

Same holds true today… those who offered on 246 2nd were smart in my estimation… that was last year’s model… while anyone anxiously waiting on phase 2 of the Infinity ought to wait 1 year longer… or buy at ORH or anything else that has now lost it’s new car smell.

Meanwhile, in D7, they aren’t building new cars so the run up was more justified. More akin to buying a classic car. Personally I thought ’05 was the top… and it suprised me to see it continue to get more expensive in late ’06, then again in ’07 and early ’08… so if we go back to 2005 levels… well, I’ll have been right afterall. But I don’t see us getting to 2003 or earlier unless you economy uber bears are right and the entire world is in shambles.

I think I’ve got my SS commenting bug out… I’ll leave the defense of the SS bulls to fluj and paco… spectating the debates is more fun than being apart of it. sfrob out

Sellers in sf are not selling because they believe price will decline for a while but that after around a year’s time they will be heading back up again, therefore they are natural holding. If they believed prices are headed down for the unforeseen future then they would get out now and cut their loses. Owners in outlining areas realized that they will not see the prices of 06/07 for a long, long time and left the game, and that’s just not happening in the real SF, yet.

“but I guess I’m Custard”

Truer words were never spoken. 😉

sfrob,

Thanks for chiming in. I wish we were getting more civilized bull arguments like yours.

About D7, there are many second/third/Nth homes that belong to wealthy folks. And these houses sit sometimes empty for weeks on. One day I made the remark to a friend that the ones really enjoying PH empty mansions were not the homeowners but their gardeners and janitors who get to spend hours with the views during the daylight all week. These homes are not a necessity but a luxury/investment. Therefore they can be unloaded more or less at will provided there’s a buyer. Knowing the humonguous bonfire of fiat money currently happening, I wouldn’t be so sure at the concept of the “Real SF” being a favorite place for second homes for too long.

“In any declining market, there are plenty of buyers. Doesn’t stop prices from declining. People bought all the way down in Stockton.”

God bless ’em. Somebody has to set the new comps on the way down.

wow,

you guys are sooo right. d7 is going to be 40-50% off

(or it is already apparently).

” A rich guy can say he took a few millions in losses and still keep his chin up, as long as he keeps the bling apparent.”

wow again,

such pithy analysis. so insightful. i sure do learn alot on this site…

Paco, thanks for the characteristically brilliant insight: “you guys are sooo right.” Can’t argue with such unassailable logic and powers of persuasion.

I see you’re sticking with that “not in the Real SF” line of argument.

oh no anon,

i’m with the program. i realize that to be popular i have to just say real sf is going down 60-80% . and most sf buyers are ‘utterly clueless’.

i’m going to be picking up pac hgts mansions for 70% off and the previous owners will now work for me. so glad i rented my entire life b/c now everything will be cheap and only us smart renters have any money left…

LOL, more “straw man” arguments from the realtors. You’ll never admit it, paco, but guys like you and fluj never even had an inkling of what was coming.

“never even had an inkling of what was coming.”

thats right. and guys like you are sooo bitter to have missed out on all the gains that ‘less smart’ guys made in the bubble that now you need to see all those gains go away. it helps you to feel superior.

fluj this. fluj that. paco this. paco that.

jorge @ 10:35 p.m.

fronz @ 11:45 p.m.

Satchel not even 8 a.am.

all of you. get a life.

I’m out of here for a while because you three are ruining this website with this stuff, precisely. My presence here is become lightning rod. Jorge, you’re only dissing me every time. nothing more. fronzi, you never had anything to say, and you pouted when I pointed it out. (The other day, in the Sanchez thread, you said six nothings in a row and then called somebody else a “clueless newb!!!!) And satchel, your value is not in your r.e. prognostication-flames, “600K for 210 Steiner,” etc. You are also incapable of humorous writing without derision. You’re a misanthrope, and it shows. That “merde sandwich” quip was the least funny thing anybody ever wrote on here.

As for never saw this coming, any number of archive searches can show otherwise. HOw many examples do you need? My beef was with the inappropriate timing, and the severity. You can’t argue that mix is not a factor right now. D-10 is up in volume and down by nearly 150K. Nowhere else can say that. Couple that datapoint with what’s going on with condos. That’s much of the story at this stage. And I called both of those developments.

Archive searches, that you so love Satchel, will also show some flippant remarks such as the one you bolded in which i was being contrary to somebody seizing upon a 1.4M South Beach condo as third horsemen of the apocalypse. Whatever. This is a BBS, and people will try to elicit responses when cornered. I’m no different.

But I can’t stick around right now. I can take it. I’m a big boy. In fact, I can dish it out better than anybody else on here that I’ve seen. No offense. The “internet slam” isn’t such a great talent to boast about. But really, it’s gotten old, and it’s gotten incessantly personal.

I invited all of you to email me to work out any difference cordially. You were not so inclined. I’ll be back sometime probably. Until then, so long.

And I see paco is also sticking with two other rhetorical arguments: (1) if you rent rather than buy a place, at any inflated price, you’re a loser; (2) anyone who thinks prices will go down is just jealous because, well, just because. But I do see a chink in the armor with his admission of a “bubble.”

Ah, this thread has finally become yet another SS standard.

There is a long-term and lasting relationship between family income and real estate values. This holds true for all income levels. Even multi-millonaires are restricted, though obviously less than most of us. As in any asset class, human behavior being what it is, people sometimes become either overly optimistic and “overbuy” or utterly pessimsitic and unwilling to buy. Nevertheless, the simple relationship between income and what it will support in real estate purchases will never change.

It should be obvious to most of us that, at least for the immediate future, the market sees no catalyst for buying. Incomes, savings and job security are likely to decline, leading to a cycle of deflation. This shouldn’t be viewed as a negative just as the “natural” process of prices clearing to a new affordability, from which the economy can build again.

At what level this clearing will complete is unknown. I try to use the long-term barometer as a guideline and like Warren Buffett look for a margin of safety. For that reason, I left San Francisco in July 2007 for Miami (where real estate values more accurately reflect incomes. In my judgement, Sa Francisco is still expensive and incomes need to rise and/or real estate values decline another 30%.

BTW, I am retired at 55 and one of the “wealthy” who some seem to think are oblivious to economic realities.

Bye, fluj. Best of luck with your flip, and in convincing your unrealistic seller clients to lower their offers, and your gullible clients to raise their bids. At this stage of the bubble unwind, it is important for the losses to be absorbed by someone other than the taxpayer, and I wish you success in your role in that process.

Bye fluj. See you here next week!

Editor:

1)I can concur with other on this board with their wish for this graph to be extended to prior to Jan 04. There is a clear trend that prices will go below that level.

How about Jan 02 – present? pretty please

One more question

2) Did the CII get completely nixed or is there one in the works? I vaguely remember a comment a couple of months ago that it would come “next week”.

If it is gone, i will drop it. But i did think it was a really great feature and service.

But the threads mostly have good info, and often start out well. So fluj, please, don’t leave.

Nope. One last comment before I run out the door to convince an unrealistic buyer of something. I’m taking my own advice: Scorn is best served by avoidance. Some of you SF r.e. bashers might consider that thought. Because all the time you spend here has a great many wondering precisely why? Why are you here?

“1 – It’s subprime only

2 – It’s East Bay only

3 – It’s East Bay and Peninsula and Bayview only

4 – It’s the non-primo SF

5 – It’s non-D7

6 – D7 is taking a hit but not really a panic”

next: obvious progression

7. The real D7 is not taking a hit

Fluj, i was molested by a real estate agent when i was 3.

There is no humor in that whatsoever. Don’t even laugh to yourself about that spencer, and never type it or say it again.

Sonwball — nice comment. I liked this part the best:

As in any asset class, human behavior being what it is, people sometimes become either overly optimistic and “overbuy” or utterly pessimistic and unwilling to buy. Nevertheless, the simple relationship between income and what it will support in real estate purchases will never change.

The last part got a little out of whack with the easy credit that allowed people to essentially borrow from their future earnings, and those future earning in most cases will be used to replenish wiped out down payments.

For the life of me I honestly don’t understand the battles on this board. It’s obvious that in general real estate agents couldn’t give a care about prices going up or down. They just need willing buyers and sellers. They also need to look and react to the world as it is; while many of the people here generally defend their (mostly bear) predictions that are in fact coming true. Why these realities are lost on everyone is beyond me.

Apparently, we all can’t just get along. But that is what makes the BBS interesting.

Another D7 Price Chop -300k at 1612 Vallejo St

https://socketsite.com/archives/2008/09/its_friday_and_we_cant_pass_up_a_pretty_face_facade.html#comments

Originally listed at $2.4 — now at $2.1 (and 0 DOM)

Fluj has to be the most easily baited poster on any internet forum I’ve frequented. No wonder the bears take such pleasure in taking their shots.

Catching up with comments. I’m on an on/off schedule due to too much work.

paco,

Not all bears are frustrated to have missed on the run-up. Some made out pretty OK. But others have jumped the gun too fast or have held up too long.

fluj,

Your main argument: the “clueless Newb” is moot. This was the name of the poster I responded to.

I usually do not call anyone names. Do a bit of fact checking next time 😉

Eddy,

Most realtors would prefer a balanced upward market. It is the easiest to work in. When it’s a seller’s market, sellers can become unrealistic about what their home is worth and buyers get very frustrated. The realtor’s consolation is a nice pay check.

When it’s a buyer’s market, buyers usually expect a great deal, sellers are often in disbelief and volume drops significantly. Realtor paychecks suffer and many leave the profession.

When the market is balanced, more often, both the buyer and seller think they got a good deal and the agent was terrific. Paychecks are alright and quality of life is better.

anon,

fluj does byte a lot at the bait. But he sure snaps the line more often than once!

ATTENTION:

I WILL BE A CONTRARIAN. (really)

I would like to re-highlight the fact that these numbers are all based in NOMINAL (not real) terms.

I have been doing some research again. I am NOT ready to say with certainty, but there is a very real possibility that we will start to see improved financial and even housing numbers within the next 6 quarters, in NOMINAL terms.

In real terms, both will still do poorly.

again: my suspician is that our govt will try to stealthily inflate our way out of our problem. as they do that, the numbers for housing/economy may improve because the dollar will be worth less.

I woudn’t be surprised if we see a “W” shaped recession as opposed to a “U” or a “L”

I’m not predicting this yet. I’m putting it out there as a possibility.

there is little question that housing will depreciate in most areas in the developed world in REAL terms. but nominal is a whole ‘nother question!

just DONT FORGET INFLATION!!!!!!

but there is a very real possibility that we will start to see improved financial and even housing numbers within the next 6 quarters, in NOMINAL terms.

Could happen. I’d be inclined to take the other side of that bet, at least with regard to the still absurdly overvalued (both in real and nominal) enclaves like SF, Manhattan, West Side LA, etc. We probably will get rough nominal price stabilization in the smashed areas within 6 quarters, though. That seems a reasonable bet to me.

I’ll just point out that a LOT of damage can be done in 6 quarters. In fact, to bring it back to the subject of this thread, the Bay Area median exactly 6 quarters ago hit its high, $665K, and it has fallen 50 percent since! Ironically, Bay Area medians are exactly back where they were in March 2000, the exact top of the last financial bubble (NASDAQ) that snookered so many here.

Fluj,

You’ve thrown out more insults, burned more straw men, and skewed the SF real estate picture more than any other poster on this site. Blaming posters for your departure is a complete sham and perfectly exemplifies the lack of accountability your profession is so well noted for.

I hope this wouldn’t be too OT, but will someone comment on USD? Where it’s at and where is it headed? How long can we expect it to stay strong? Any thoughts will be appreciated.

chuckie,

I like the USD still. You know I was one of the very few voices on SS (maybe the only one?)calling for a strengthening of the USD early in 2008. I still think there is room to go up a little against the majors, although I wouldn’t expect too much strength against the Yen. Europe is a budding catastrophe, and places like Ireland, UK, Spain and Italy (probably most of the “Club Med” countries) could go kablooey. China is a mess as well, and I expect yuan depreciation. All these factors should smash all the other currencies around the world that are managed against the reserve USD in one way or another.

The USD is the best of a very bad bunch (fiat currencies), at least for the next year or so.

I really appreciate these (very OT) comments on the USD — I sure hope this plays out like LMRiM predicts as a trial is taking me to Europe pretty much all summer and the whole family is coming along. It’d be nice if this trip didn’t break the bank.

On fluj, I’ve often said that I sincerely respect his opinions. However, his 8:55 post above illustrates that he’s gotten a bit stale. He’s stuck on “it’s all just D10 and condos and nowhere else” (yes, fluj studiously avoids such unambiguous phrasing, but his post can mean nothing else). I would welcome fluj’s comments back any day, especially if he revises his outlook to include a dose of the current reality.

Jorge,

f!uj will come back. He’s very resilient. He has probably 9 lives and this is the second one I’ve seen him use up. Any long timers know how many exits so far?

USD did a nice comeback since the 1.60 low vs EUR.

The mood in Europe (posting from there for a few weeks) is gloomy at best. Commies are calling for the end of capitalism, you know the nonsense.

The big shocker for me is Fiat that plans to gobble up 30+ of Chrysler, with option to get 20%. For Pete’s sake, FIAT? Some Chrysler models are revamped MBs. What will the next Chrysler model be? Panda Sport? LOL!

LMRiM:

I’m not betting anything. I’m just putting out the possibility of a “W” shaped recession. I’m starting to hear more squawking on this.

of course much of it depends on what Obama and the various Central Banks do in tandem with the market.

as I said above, I’m not predicting this yet. I’m putting it out there as a possibility

it fits in with the Ka-POOM theory, although I still have no idea how long Ka takes before POOM hits.

Ex SF-er: Current inflation expectations (difference between 10 year TIPS and 10 year Treasury) appear to be around 0.5%, so the real interest rate on mortgages is ~4.5%.

Suppose that this inflationary explosion that you fear occurs – let’s say it gets into double digits (10%). Even if real interest rates stay at their current lows, the 30 yr mortgage rate will hit 14.5%.

How on earth will buyers make payments at current prices with mortgage rates near 15%? Sure, after a decade of steady 10% inflation then incomes will rise enough to support current prices at such interest rates. But you’re talking about just 1.5 years out. No way a 15% increase in incomes could offset the downward pressure of a tripling of interest rates.

anonm:

first: I am NOT saying that this is likely. I’m putting it out there as a possibility. some people are 100% sure of their outlook. I’m more pliable.

I believe we’ll see a ka-POOM, but I have no idea when the POOM will occur. I used 6 quarters because I’ve read some reports of others who suggest it could happen in 6 quarters. I personally believe POOM will happen much later, but am open to the possibility.

That said: here is how it could in theory happen: government intervention.

the govt would continue pumping money into the system. stimulus checks, bailouts, etc. perhaps a “bad bank” will take the bad assets off the rotten banks?

they would use some sort of influence to “force” the banks to lend more even to poor candidates. This would increase the velocity of money. which would increase monetary inflation.

the govt could then under-report the inflation (just as they typically do).

the govt could watch what the market does with that information. IF the free market starts putting pressure on the 10 year treasury, then the Fed could buy 10 year Treasuries pushing the yield down. it could also monetize other debt. It could also work in concert with the various central banks to have them purchase at the long end of the curve.

the govt could mandate that banks lend with decreased risk premium using coersion or a new federally chartered Fannie/Freddie/Ginnie like entity. (like the suggested 3.5% 30 year fixed mortgage)

all of the above would mean that one would have negative REAL interest rates which would of course cause misallocation of recources. it could cause a bubble SOMEWHERE (the govt cannot control where the bubble goes).

there are many reasons why this might not happen. If the Central banks refuse to cooperate. If the increased money supply runs to commodities. if the bond market bucks back. and so on.

as I’ve said before, I’m watching for signs of this (I don’t see many right now, but a few)

I don’t trust the govt to do what is right. but I also don’t underestimate their power (especially if wielded foolishly).

sorry, this post poorly worded and likely contains errors, hopefully the gist is understood.

“again: my suspician is that our govt will try to stealthily inflate our way out of our problem.”

Possibly. But unless they’re going to unveil a crazy loan program they’ll have to create wage inflation to boost home prices.

It’s possible for them to create a wage-price spiral but it’s not an overnight process. I think you’ll have plenty of time to see that coming and react to it. At the moment I see layoffs, wage cuts and general deflation. When I see employers start to get into bidding wars to hire talent I’ll start to worry about generalized inflation.

(enjoy the books.)

As the guy who was accused by fluj of running him off the first time, it’s nice to have some company.

Welcome to the club, boys.

But unless they’re going to unveil a crazy loan program

bingo. see my post above.

again: it would be CRAZY to do it, STUPID to try it. REDICULOUS to suggest it.

thus I consider it a possibility. nothing more.

deflation is so “terrible” to our leaders because of all the reasons that you (and even I) have brought up.

however, it can be overcome if people are desperate enough.

I’m only posting a contrarian opinion to keep peopole on their toes.

I also do not see an end to the deflationary forces any time soon. but an INCREDIBLE amount of money has been used by our govt of late with more on the table. it’s kept in check by the lack of monetary velocity. That can in theory change.

also: don’t forget that we can see massive inflation here quickly if foreign central banks repatriate dollars to the US. I find that scenario unlikely for many reasons.

this stuff is intertwined and complex, and I foresee different outcomes based on just a few decisions by a small number of people.

Ex Sf-er,

Mish has an interesting piece about inflation/deflation that isn’t on his blog yet. He says it better and more succinctly than I ever do:

http://www.financialsense.com/Market/shedlock/2009/0122.html

I really think any attempt to ignite “inflation” by the USG will fizzle pretty fast. The government has a lot less power than you give it credit for – in the end it is powerless IME to lean against markets when markets want to go the other way. Extra money that gets showered on the sheeple by some happenstance will quickly get hoovered up by the elites, leaving the population poorer and less able to afford high housing prices.

As I have been saying forever on SS, I think that once the bulk of the debt is either gone (through default or bankruptcy) and/or sitting with the USG (through public absorption of the bankster’s bad gambling debts), that’s when mass inflation will benefit TPTB and that’s when it will happen. It could take 2 years, could be 10, but it’s not going to be in 2009 I bet, and I’m pretty sure it won’t come fast enough to save nominal SF housing prices.

“but it’s not going to be in 2009 I bet,”

yup, I was thinking of setting aside economics in 2009 and pursuing other hobbies. I expect 2009 to just be a long slow grind.

The only thing that might provide excitement in 2009 would be a currency crisis but I’m already positioned in precious metals as insurance against that. A currency crisis would increase the dollar cost of globally traded commodities and things we import and export but wouldn’t have a direct impact on house prices. (At least not a positive one.)

Diemos,

I’ve always been adverse to gold because it only seems to store value only during stress points. (I’m a very unsuccessful market timer) What percentage of your wealth would make it worthwhile to take this timing risk?

Thanks

Gold has no intrinsic value (i.e. you can’t eat it, live in it, burn it for warmth) it only has transactional value. It’s only worth what real wealth someone will give you for it.

My thesis is that gold does well when other “stores of value” do poorly. The bursting of the credit bubble was going to pull the rug out from under stocks and real estate, the economic slowdown was going to collapse industrial commodities and the government response of printing money would eventually hit cash and bonds. This seemed to me to be a once-in-a-lifetime opportunity to ride gold up. We’ll see if that happens and if I can get out in time before it goes back down.

Not investment advice. Gold can go down as well as up. Past performance is not a guarantee of future results. Sorry, tennessee.

“What percentage of your wealth would make it worthwhile to take this timing risk?”

Sorry, didn’t answer your question. I live by a principle from Vegas that has served me well in all areas of my life.

and one other gem from Vegas which I cherish as a guiding principle for my investments:

diemos,

A currency crisis could drive the cost of borrowing in US$ up, as foreign lenders get worried. A rise in interest rates would most certainly affect house prices. I’m not sure what you mean by “positive” (I think it’s positive when house prices come in line with rents and incomes), but at today’s historical lows, it won’t take much of a percentage point increase to drop prices a lot.

Correct.

I use “positive” in it’s conventional sense. A rise in nominal prices that makes housing an attractive investment.

Diemos,

Thank you.

So if you “bet” only what you can afford to lose, does that amount make a material difference in a world in which many currencies have little or no value?