Purchased for $2.125 million in April of 2016, the “rarely available,” two-bedroom, two-bath condo #17E in the LUMINA tower at 338 Main Street was offered for rent at $7,000 a month in 2018.

After a year as a rental, the unit returned to the market priced at $2.4 million in May of 2019, was reduced to $2.349 million in August of 2019 and then withdrawn from the market that December.

And having been listed anew for $1.899 million last week, the 1,401 square foot unit with “stunning landscape views of the bridge and city” is already in contract with an official 7 days on the market (DOM).

If you think you know the market for newer view condos in San Francisco, now’s the time to tell. For those running the numbers at home, the unit’s HOA dues are currently running $1,210 per month. And keep in mind that the index for Bay Area condo values is up 14.7 percent over the same period of time (and the “median sale price” is up as well).

So much wasted / dead square footage in the foyer / entrance hall. I’m going to say $1.93M

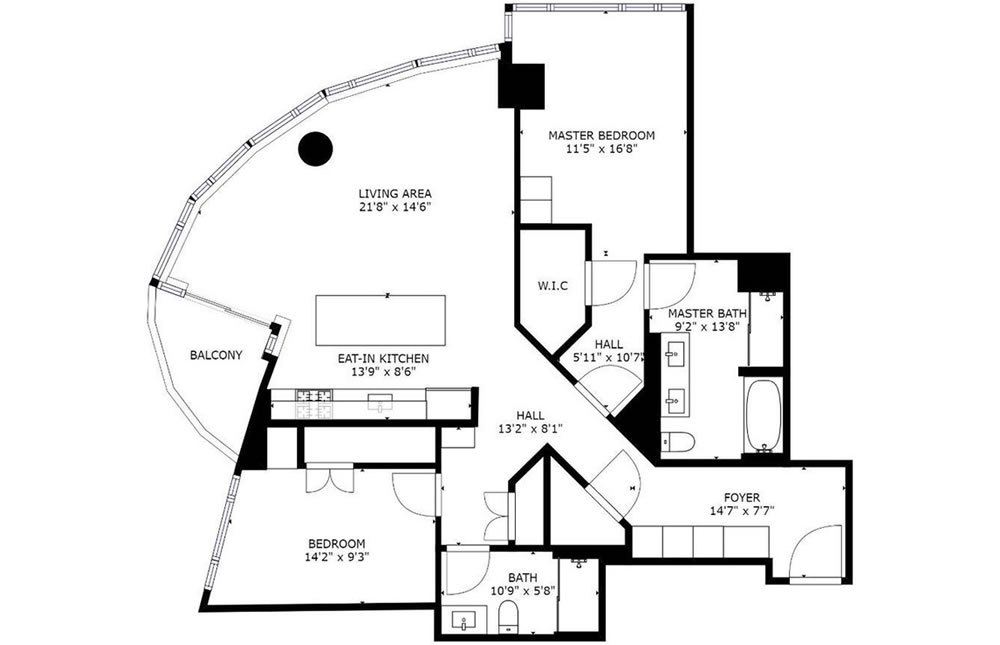

The Lumina layouts I’ve seen are very poor. Lots of unusable space that make large sq condos seem much smaller.

It seems like the design intent was to optimize the locations of the bedrooms and living/ dining room for getting the best views. I agree, it comes at the expense of a having a layout that is overall awkward and not the most efficient in how it utilizes available space. However, this is less of a concern for the kind of buyer who has no intention of using this condo as a primary residence.

I can see people purchasing vacation property in Miami Beach, or even a winter getaway in Paradise Valley and a Summer getaway in Jackson Hole, but who is going to be vacationing in SOMA? I’d think the Marina is where you’d put your SF vacation home. Or is this for investors, that want to sit on the property and wait for appreciation?

Generally, everything being equal, there is a 5% to 10% premium for brand new construction (And you lose that premium as soon as you purchase. Just like a new car, you lose x% of the value as soon as you drive it off the lot). Consider the market peaked in 2016/2017. I say losing 10% of value, i.e, $200k is about right inline.

Can you reference any properties that gave up a 10% premium during the boom?

It is statistics. If you want specific examples:

– New development usually have a clause of no selling for at least 12 months after purchase.

– On this website, there is a plenty of apple to apple comparison (posted with glee of course) of new condos that was purchased in 2016 or 2017 or 2018, and sold at same price or 10% slight lower in 2018 or 2019 when market softened (but not dropped as dramatically by covid).

(And you lose that premium as soon as you purchase. Just like a new car, you lose x% of the value as soon as you drive it off the lot).

That’s incorrect. In fact, new construction units are frequently flipped at a premium to their sales office prices, and often by agents, at least when the market is moving up.

And in fact, the new construction market, which tends to be a leading indicator, started turning back in 2015, a trend which shouldn’t have caught any plugged-in readers by surprise.

It was prefaced, everything being equal….

Of course, if market is shooting up dramatically, the momentum of moving up will cover the new condo premium paid. Even it is shooting up, at the very same moment, a resell will be 5% to 10% lower price than comparable brand new in the same building.

“Even it is shooting up, at the very same moment, a resell will be 5% to 10% lower price than comparable brand new in the same building.”

But do you have any examples of this? You can’t have “statistics” without any data points.

I’ve heard the opposite on this. That since professional sellers (i.e. new condo sales offices) are more properly taking into account the time value of money (financing costs for the development, cost of advertising and running the sales office, opportunity costs,…) they lean towards letting units go at lower prices to yield faster sales vs flippers undervaluing the time factor and focusing more on sales price.

The new construction premium is a not a new concept, google search.

Like I said, new condo purchase will always have at lease 12 month lock in period in the contract, that really prevents any real world controlled experiment.

But one way to do this is to have a thought experiment. Suppose as a buyer, you are faced with 2 choices in the same building. They are exactly the same.

One has never been lived in before, and one someone lived in before.

If they are priced the same, would you buy the used one or brand new one?

I would say 100% of people will pick the brand new one. Thus brand new one is worth more.

Exact how much more, of course, it will rely on statistics again. But you don’t like statistics apparently.

I don’t mind statistics, but you can hardly argue that on average new condos lose 5-10% of value immediately if you can’t even find a single example. Even if you cant find a new condo flip with a sub 1-year hold, you could look at 1 year holds vs existing condo resales. i.e. if new condos flip 10% higher after 1 year in a hot market by your theory existing condos should be flipping 15-20% higher in the same market.

I’ll agree with your thought experiment, but I don’t know if the scale of that is in the hundreds of thousands of dollars. Reversing your thought experiment, would you pay $200k more for an identical condo just because it had no previous owner? Why?

And a sale involves a buyer and a seller. Look at what I said about the sell side above. In a flat market would you rather sell a condo for $1M now or $1M a year from now? Professional sellers employ finance people who make spreadsheets telling them exactly the costs of waiting a year.

@inthemarket — since two units cannot be in the same geographical space and could not have been finished at the same time, they can’t be exactly the same.

In a debt financed market, at 5x leverage, 10% difference in price translates to 2% difference in down payment.

Buyers will consider time-value and market sentiment. If the lived in one has better sunlight or less blight in the view or better view and so on the price can vary. If the exit potential for either unit is the similar in absolute value, then old vs new doesn’t make a difference.

I genuinely don’t understand the very slightly snippy “But you don’t like statistics apparently.” When someone is earnestly asking repeatedly for any kind of general data or data points and you provide none. It’s ironic.

This is not true. Comparing price behavior of homes to cars is comparing apples and oranges. I’m an investor and have bought a number of brand new homes. They appreciated from the start and if I had expected a 10% drop within 3 years I would never have purchased the homes. One thing that happens in a new project built in phases over a year or two is that the first phase asking price is less than the second phase and that phase is less than the third. The first phase units do not depreciate in value, they simply do not appreciate enough to match the prices of the newer phases.

It appears this unit was bought by an investor and rented for a year then left vacant (?) as it was put up for sale. The mortgage payments and other carrying costs for the 2 years or so of vacancy need to be added in meaning there was more than a 10% loss to the investor.

This was bought during the period of irrational exuberance in terms of expected price appreciation. The signs that the market was peaking were out there at the time so it’s a case of the investor not doing their due diligence.

Listen to yourself for a second.

The rise in value of the first phase didn’t match listed brand new prices of second phase (assume everything else is equal). And you still think the concept of new construction premium doesn’t exist?

That is not the point – I was addressing your claim that there is a built in depreciation for new construction as there is for automobiles which isn’t true.

Do you want to pay premium for a new unit or are you expecting premium for a new unit that you intend to sell?

$2.0M

Wow, now it is pending just 5 days after it went back on market.

People who are waiting on the sidelines during covid are jumping back into the market. Especially the millennials who are hitting early to mid thirties (who are renting previously) are all buying.

At the same time, inventory levels have inched up with new listing activity (“supply”) having outpaced the number of contracts written (“demand”) by those who were previously sidelined (on both sides of the isle).

Sure. The numbers of buyers entering the market will be increasing. The sales you see right now are people who started looking in December/early January.

Millennials (who are the biggest demographic) who entered labor force in mass during of 2008 – 2012 financial crisis or just at the end, didn’t have money to buy when they started their careers. By the time, we hit mid 20’s, 2016 2017, the prices are rose so much, it feels like we missed the boat. Now, they (those who are professionals) are making good money, and ironically able to save more a lot money during Covid. Assume two professionals with 200K income each, buying a $1m or $2 million place isn’t a problem for them at all. Since apple to apple is always anecdotal anyways, anecdotally, many of my friends in the same boat are starting to look now. 3 of my friends all bought in last month. It is kind of funny, in my circles, we used to talk about drinking, partying and dating, now real estate dominate our conversations. Believe me, more buyers than ever will enter the market in this coming year or so.

Inthemarket, your anecdotes speak to the very hot 1M to 2M single family home market I’m seeing right now. I didn’t put it down to millennials before but that makes sense. It seems like everything listed for low 1s is going for high 1s so far this year, all over the Bay. There’s simply a lot of people who can afford 1.6 – 1.8M right now. And coincidentally that’s what a decent house costs in Berkeley, Albany, nicer Oakland, Bernal, Mission, the Avenues …

The problem with using the Bay Area condo index and applying it to a particular sub-market (TTC condos) is that the BA condo market is not uniform. It is made up of many sub-markets each performing differently. It’s not surprising there are significant loses in condo prices in the TTC area given the host of factors which have been discussed at SS.

If possible could SS provide more granular numbers for the Bay Area condo and home price markets? Having county by county numbers would allow for a better analysis of a particular sale. In this case the 19% loss is larger than the typical SOMA loss which seems to be around 10% – 12%, but it is not as dramatic a drop as one might infer if one is comparing it to the overall Bay Area condo index.

1.99M

Beautiful. One thing, in this day and age, a small office or den to make a work space in, seems like a must. It would be a deal breaker for me.

So rich people buy expensive properties high in the sky, and walk around a deserted downtown with lots of homeless, dirty streets, closed up restaurants …. what a bargain.

UPDATE: Rarely Available View Condo Fails to Fetch Its 2016 Price