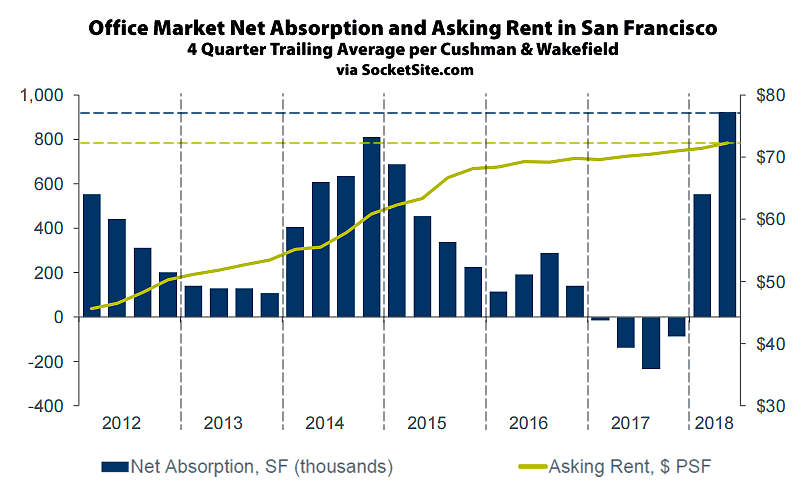

With 1.3 million square feet of new office space having been delivered over the past quarter, all of which was pre-leased and instantly absorbed, included The Exchange at 16th (Dropbox) and the tower at 181 Fremont Street (Facebook), the average asking rent for office space in San Francisco ticked up 1.3 percent in the second quarter of 2018 to an all-time high of $72.30 per square foot per year, which is 3.0 percent above the mark at the same time last year.

At the same time, the average asking rent for older Class B space was relatively unchanged, inching up 0.1 percent in the second quarter to $64.65, which is 2.4 percent above its mark at the same time last year.

And the overall vacancy rate dropped 20 basis points to 7.4 percent (5.1 million square feet), which is 1.6 percentage points below a historical average of 9.0 percent and 1.0 percentage points lower than at the same time last year, but that’s not accounting for 970,600 square feet of space which is technically leased but available for sublet, up from 871,000 square feet of subleasable space the quarter before.

And while there remains another 3.4 million square feet of office space currently under construction in the city, a third of which will be delivered, pre-leased, by the end of the year, the estimated cumulative need of tenants seeking new office space in San Francisco is back to 6.0 million square feet, which is 25 percent above its mark at the end of the first quarter but roughly even with the same time last year.

Excellent news. Let’s make it easier and more efficient to build more housing to reduce commute times for everyone.

“3.0 percent above the mark at the same time last year”

If the rates stated are the actual prices – i.e. nominal not “inflation adjusted” figures – then it sounds like they’re tracking the CPI, more or less…I think that’s what is called a “plateau”

I thought SF’s economy would cool given the geopolitical uncertainties, but it’s not happening.

Huh? Rate increases went from ~12% a year in 2012-15, to ~3% (aka “inflation”) in the last 2-1/2…how is that not “cooling”?

SF added 1.3 M square feet (big new supply) and prices stayed constant (i.e. demand matched the new supply). Plus vacancy rates dropped. I don’t see that as ‘cooling’.

Well yes, 1.3M on ~100M. I guess one could call that “big”…or maybe not. We seem to speak different dialects of “Superlativese”.

On the top chart, it looks like more square footage was absorbed last quarter than any quarter since 2012, at least. Is that that the wrong interpretation?

As we reported in April, “the net absorption of occupied space was a record 2.25 million square feet in the [first] quarter, driven by the delivery of Salesforce Tower (415 Mission Street) and 350 Bush Street, which together total over 1.8 million square feet and were delivered 97 percent pre-leased.”

“cooling” = rents dropping. That is not happening.

Rent hikes dropping from 12% a year to 3% a year = “not as hot as previously”

Ha. “not as hot as previously”? What’s another, one word long, description of that state? Would you say it’s maybe … cooler?

Touche. Brevity sacrifices precision. But, of course, rents are still rising, i.e. getting hotter. So “getting hotter but not as quickly as previously” is more accurate. Not “cooling” by any reasonable stretch.

my hope is SF gets tapped out due to prop M/lack of room, and the overflow moves to oakland…

There are lots of posters on this site hoping for that. The rents in SF and SV are well above the East-bay and you would think that some outflow would happen, particularly when so many employees are commuting in from there. If not in Oakland, then in Pleasanton, Walnut Creek etc. where there is much more room and a deficit of jobs/housing.

I suspect those local suburban governments will be in opposition to any sizable office development.