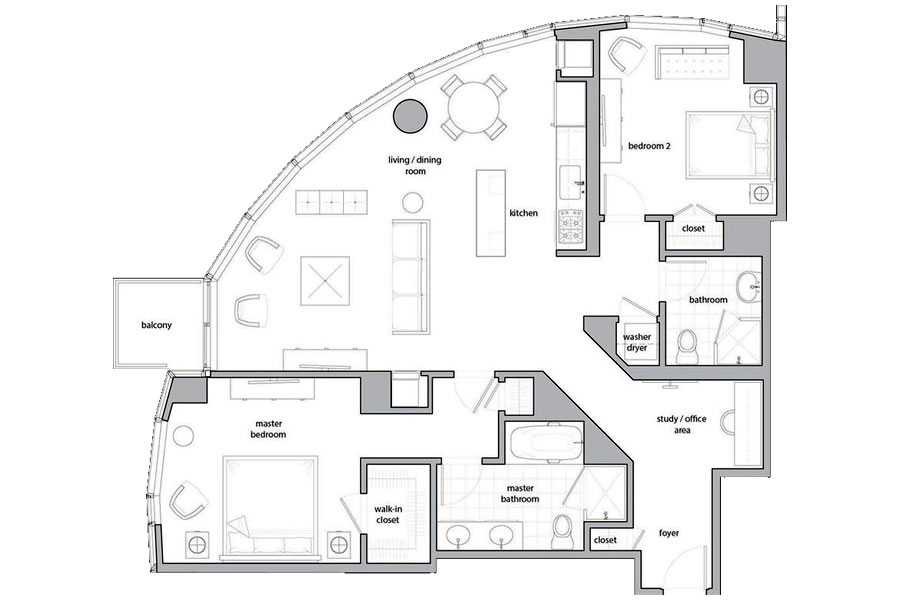

Purchased for $1.85 million in July of 2013, the 1,340-square-foot unit #35E at the Infinity, a “signature corner 2BR/2BA with stunning views of water, city or Bay Bridge from every room,” returned to the market listed for $2.799 million in November of 2015.

Reduced to $2.699 million in early 2016 and then withdrawn from the MLS that October, 338 Spear Street #35E was re-listed for $2.499 million last August, reduced to $2.399 million in September, reduced to $2.299 million in November and then withdrawn from the MLS anew a little over a month ago.

And on March 1, the sale of 338 Spear Street #35E quietly closed escrow with a contract price of $2.245 million or roughly $1,675 per square foot, the price at which the condo was then listed anew on the MLS three days later and then recorded as sold on March 6 for another “full-price” sale with an official two days on the market according to all MLS-based stats and reports.

This can’t be right. Case Shiller says prices have risen about 45% since July of 2013, yet this place sells for 21% more than its 2013 price.

Based on the short hold, this might have been an investment. Subtract 7% for realtor fees, staging, transfer tax and you’re up 14%. With 30% down, they made about 45% due to leverage, assuming the rent (or equivalent rent) covered their costs. Had they put that money in the stock market, unleveraged, they’d be up 65% with a lot less hassle.

who puts 30% down, do the math using 20% and what do we have?

Keep in mind that the actual 2013-era purchase would appear to have been without the benefit of any leverage (i.e., 100% down).

Interesting connection to a “SS celebrity”. When the REALTORs are selling…

It is getting pretty obvious that ‘Elvis has left the building’ for this RE cycle.

But people will have to keep up appearances though. It’s almost a punchline that the result of all RE industry “analysis” is that “there’s never been a better time to buy”, but it is obvious that it has to be that way. It’s clear to many that since agents are paid as a percentage of sale price that they have an incentive to overbid, but the only thing worse than a smaller commission is no commission at all.

Looking at the last cycle, from late ’05 to ’09 was a pretty bad time to buy (even buying at the flat top you were essentially underwater due to selling costs), but what business can afford to go without revenue for 4 years? A scrupulous agent may advise you to underbid in a weakening market, but even when the writing is on the wall it is asking too much for anyone to endure a 4-5 year dry spell.

I can only speak for the markets I semi-follow: noe in SF and then palo alto and menlo park where I live and work. I’m pretty sure there isn’t a single SFH owner who purchased late ’05 to ’09 (should actually be mid ’08 since the credit and housing markets were paralyzed after the election and into in early ’09) in those neighborhoods who regrets that decision.

would I buy now? not sure/probably not, but I can say I was extremely nervous when I pulled the trigger in June 2009. I’m not sure it is ever easy/comfortable unless you are buying a 2nd or 3rd home with the earnings from your last week/month/quarter.

also, all things being equal, agents should care if prices are rising or decline. 2% of $3M isn’t too different than 2% of $3.2M. the difference is that when prices are on the decline, turnover slows way down. CA sellers are less likely to sell, especially if their holding costs are low and buyers, interestingly get more nervous. prices stay sticky but agents have to hussle more on both sides.

[Editor’s Note: Bay Area Home Sales Drop, 9-Year Low in San Francisco.]

Hard to have it both ways. Every time the editor adds to the litany of apples to apples ROI losses, people chime in that the data points should be ignored in favor of the wider Case-Shiler averages. But then can you also say that not a single SFH owner fell in line with the wider Case-Shiller averages during the last cycle?

It’s a common fallacy to look at a market cycle and think: “If only people had ridden out the cycle”, but if everyone had ridden out the cycle and not capitulated on price then there would have been no cycle!!

I think I’m missing your point. C-S should indicate that buying 05 to 08 and holding until now in the areas I mentioned turned out pretty well. obv, C-S is bay area wide, but a) we know that noe, menlo and PA have outperformed and b) almost any property there would be top-third in the index, and top-third suffered less 08-10. first republic prestige index was perfect for this (custom produced by C-S). sadly it is no more but its pre-crash peak was Sep 2007 at $3,084,670 (533.17). The last number I can find is Sept 2014 at $3,449,566 (596.25). you’ll have to take it on faith that 2015 and 2016 (and even 2017) were pretty crazy down here.

were there better things (in hindsight) to do with your money? generally yes, assuming you had access to leverage. however, you should purchase a home because you want stability for your family; not because you think you can time the market and flip

I bought my condo in SF in 2007. I did okay. Basically got a 24% annualized return over a decade on the principal. Sure I would have done a lot better if I bought in 2011 obviously, but glad to have had the condo to live in during those years.