If a reader is correct, 2151 Green Street ended up selling at auction on 10/15 for $3,066,001, one dollar over its opening bid. That being said, 2151 Green Street is still listed as an active short sale seeking $6,900,000 on the MLS.

Somebody appears to be confused, perhaps another plugged-in reader can confirm if it’s the reader or Realtor.

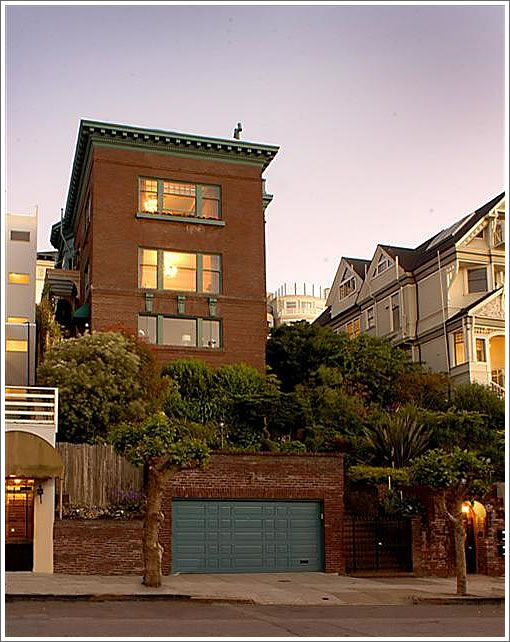

Purchased along with the adjoining empty (and since separated) lot for $9,000,000, 2151 Green Street had returned to the market in 2008 asking $10,950,000 for the six bedroom Cow Hollow mansion.

∙ Listing: 2151 Green Street (6/5) – $6,900,000 [MLS]

∙ But Hey, $550,000 Is Simply A Rounding Error To A Proper Industrialist [SocketSite]

∙ Another District Seven Mansion Heads For Foreclosure (2151 Green) [SocketSite]

∙ The Scoop On 2157 Green Street (Could You See The Foreshadowing?) [SocketSite]

JMO but it is sad when they sub-divide the already small SF lots.

In my area they are trying to subdivide 2 lots into 3. Just keep cramming in the structures and open space/greenery be damned.

They both could be right. The bank may have bought it back at the auction, so now it is REO, and they are listing it for sale (though technically no longer a “short sale”)..

[Editor’s Note: If the bank bought it back it wouldn’t have been at a dollar over asking and the selling party and listing (which is now 135 days old) would have changed from the mortgage holder to the bank.]

or they could both be wrong. if it is a short sale at 6.9 how could the starting bid on the auction be 3.066? was the extra 3.9M in debt in the form of a second or HELOC? are the lots being sold separately?

if true, congratulations to whomever showed up with 3.066M in cash.

Hi,

My accessible records have not been updated yet if it sold on 10-15-09.

2151 Green Street currently appears to be 2 separate parcels owned by 2 independent parties.

LOT 0557-061 HOUSE 0557-062

Party 1 appears to have purchased the entire property (House plus Lot) on 10-17-2003 taking out a First Mortgage of $3,445,000.00.

It appears that Party 1 sold the House to Party 2 on 11/09/2007. Party 2 took out a First Mortgage of $6,300,000.00.

Perhaps the LOT was sold for $3,066,001 and the HOUSE is being marketed for $6.9M ?

Thursday

10/15/2009 2:00:00 PM Address: 2151 GREEN ST

City: SAN FRANCISCO

State: CA

Zip: 94123

County: San Francisco

APN: 0557-020

Sale Status: Sold 10/15/2009

TS Number: CA09246768ED

ASAP Number: 3150577

Notice of Sale Amt: $6,913,767.84

Opening Bid Amt: $3,066,000.00

Sold Amt: $3,066,001.00

Sale Location: At the Van Ness Avenue entrance to City Hall, 400 Van Ness Avenue, San Francisco, CA 94101

Trustee: Quality Loan Service Corporation

Trustee Phone#: (619)685-4800

I’ve been trying to keep track of what’s happening here, but I haven’t heard anything, to be honest. I do know that both lot and existing home were owned by the same person before he moved back to Iran. This is just a problematic property on so many levels. Trying to develop the lot would be horrifically expensive and an engineering nightmare. There’s a 20+% grade between Green and Vallejo – I can’t imagine trying to build something into that while shoring up the homes on all three sides. Its only real value is as a side “yard” to 2151 – and that property on its own needs extensive rehabbing; plus you have to undo the ghastly damage done by the previous owner. At this point, I can’t even guess the real value of this place.

“Reader Versus Realtor”

after not reading SS in ages, then seeing the 1440 Kearny fiasco…. next post is “Reader Versus Realtor” from the Editor.

It is that way in your head isn’t it?

fwiw – it is still in the MLS as a short sale. since it’s an “mls only” listing expect it to be on the MLS until it’s reported to the Board.

back to ignoring SS until it stops behaving like a soap opera… same characters, same story lines, boring as hell unless you’ve got nothing better to do with your ENTIRE day

I don’t see how this can be true if still listed active on the MLS. Unless the realtor is just a complete idiot and doesnt even know what is going on with his own listing. But if it did sell @ auction that the bidder got a absolute STEAL at $450 p.s.f!!

hangemhi took his nasty pills today.

I thought that when you “bought” a place at auction on the steps of city hall, what you are buying is the deed of trust – in otherwords, just the debt against the place.

Once you buy the debt, it is your job to go through the court process to gain title through the foreclosure. These trustee sales are just the bank trying to offload the outstanding debt onto some other poor soul who will then go through the hoops required to gain title.

Unfortunately, there may be other debts secured by the building, other liens not yet filed and taxes and claims of all sorts that you can take on when you actually gain title.

Truly buyer beware.

But until the new owner of the debt gains title, the building should still be the seller’s to sell however they can – if they can.

“I thought that when you ‘bought’ a place at auction on the steps of city hall, what you are buying is the deed of trust – in otherwords, just the debt against the place.”

That’s not right. You are confusing buying the (promissory) note with the deed of trust. If you buy the promissory note, then you’re just buying the debt.

If there is a trustee sale based on a deed of trust, you’re buying the property. A deed of trust is a way to avoid having to go through formal judicial foreclosure. Instead of judicial foreclosure, the trustee forecloses on the property (after following proper procedure, e.g. NODs, etc.), and either conveys it to the bank for the amount of the defaulted mortgage or sells the property and pays the lender the proceeds.

The mls says that listing agent is not a member of the local board of Realtors. So this is a courtesy listing. That means that he can’t access the mls online and put the listing in himself. All changes must be made through the Board. Examples are a price reduction, status change, a withdrawal, a cancellation or closing.

Although it takes a few days to make changes through those channels, it should reflect it by now if he notified them right after the sale. Only time will tell if he did and the board is slow or he didn’t and it just languishes on the mls until the listing expires.

IF someone bought this for 3 mil, that will be the deal of this cycle. I cannot believe there was no bidding against, at that level.

Is that the real sale ? just a factual question here.

Whoever the party of interest is getting the $3 MIL they certainly could have done better, whatever the process was, if it was open.

I’m with Louis — this is quite curious. The lender who foreclosed seems to have gotten what they wanted. But was there no other mortgage? If so, one would think that lienholder would have stepped in and bought it (maybe that’s what happened). Or did the owner just skip town and walk away from millions in equity?

FWIW, my armchair analysis, who’s on first. The parcel map shows APN 0557-061 Lot and APN 0557-062 House as pointed out by SL123. This also seems to be how the taxes are billed. However, on the SF Recorder’s website, all the action is taking place on APNs 0557-019 and 0557-020 (which is the foreclosure cited by resp). It can take up to a month for a transaction to show up on the recorder’s website, and I don’t see anything there yet (with regards to the foreclosure). I can confirm that a NOTS was filed by Quality Loan Service Corporation on June 26 for the APN which was foreclosed upon (0557-020). There appears to be a deed of trust with WaMu on Nov 9, 2007 and BARCLAY FINANCIAL GRP got in on the action April 22, 2008.

Talk about trying to make something out of nothing. The out of town realtor is probably just lazy and has yet to go through the motions to remove the listing.

Too many questions at this point. Very interesting.

I guess I’m the “Reader”. Couple of things: The listing agent (“Realtor”) is not from out of town, office address is on Market St., apparently he’s just not a member of the SF Assoc of Realtors, so I’m going to guess that he is probably not a Realtor. It definitely was sold at auction last Thursday. But more interestingly, my source at the steps said that the buyer who paid $1 over was the previous owner. Now, I don’t know if he meant the foreclosed owner or the fellow who sold it to him. I’ll wait for the deed to record and report back when I find out. Very interesting.

Interesting. Sounds like the guy who sold it to the just foreclosed owner now in Iran is the new owner. I hope that is what happened. Only question is what became of the vacant lot?

If that’s the case he effectively shorted the house – sold it and now, if true, has bought it back at a lower price.

[Editor’s Note: If the bank bought it back it wouldn’t have been at a dollar over asking and the selling party and listing (which is now 135 days old) would have changed from the mortgage holder to the bank.]

Not necessarily true. We often credit bid debt well below the UPB and just above where we want to sell the property… as for the listing not changing, well we have seen stranger things on the MLS haven’t we?

an interesting twist for sure; it will all be revealed in the end.

not sure you can buy your own note back at auction and not be liable for the deficiency.

not sure you can buy your own note back at auction and not be liable for the deficiency

first, you are not buying the note at a foreclosure auction. second, the owner of the note if you were to buy it is not on the hook for any deficiency, only the borrower. If you go the judicial foreclosure, then any deficiency remains. non-judicial, and the deficiency is wiped.

MLS updated to withdrawn. Certainly gives some more plausibility to the story.

The story continues: The 2151 Green Street Scoop: Wait For It… (and it appears our reader was rather right).

“I thought that when you ‘bought’ a place at auction on the steps of city hall, what you are buying is the deed of trust – in otherwords, just the debt against the place.” That’s not right. You are confusing buying the (promissory) note with the deed of trust. If you buy the promissory note, then you’re just buying the debt. If there is a trustee sale based on a deed of trust, you’re buying the property. A deed of trust is a way to avoid having to go through formal judicial foreclosure. Instead of judicial foreclosure, the trustee forecloses on the property (after following proper procedure, e.g. NODs, etc.), and either conveys it to the bank for the amount of the defaulted mortgage or sells the property and pays the lender the proceeds.