If you’re truly plugged-in you’re already familiar with SocketSite’s Complete Inventory Index (Cii). But if you’re not:

The goal of the Cii is to paint a complete picture of housing inventory and new development in San Francisco; listed, unlisted, pipeline, and potential. In fact, we believe it represents a fundamental shift from the abstract to the tangible with regard to what’s in the works throughout San Francisco.

We’re now tracking the size, status, probability, and available inventory for over 200 new developments throughout San Francisco (30,000+ condominiums in total). And we’re keeping tabs on another 15,000+ “net new housing units” (including rental units) that are either proposed or on the drawing boards. All told, it’s a potential inventory of 45,000+ housing units (i.e., the majority of San Francisco’s overall housing pipeline).

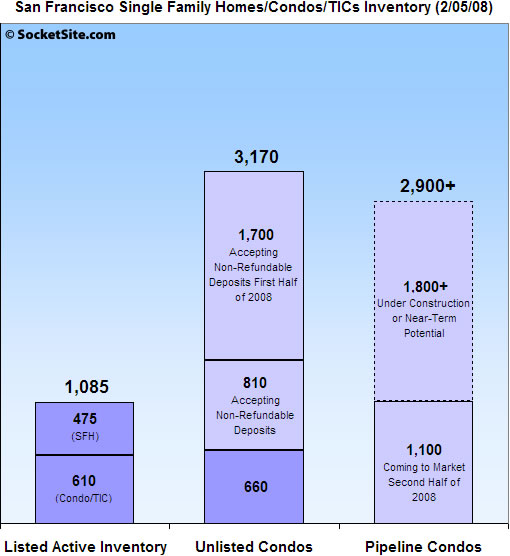

As it stands, in addition to the roughly 610 San Francisco condominiums (and 475 single family homes) that are listed and available for sale on the San Francisco MLS, we estimate that there are approximately 660 condominiums that are not listed, but are currently available for purchase and occupancy. These condos include unlisted inventory in buildings such as The Potrero and SoMa Grand.

We also estimate that there are currently an additional 810 condominiums that are actively competing for the attention of buyers and accepting non-refundable deposits in sales offices throughout San Francisco (examples include Infinity, Arterra and The Hayes). And within the next five months, we expect to see an additional 1,700 condominiums begin marketing, accepting deposits, and competing for sales as well (think BLU, Argenta, and the second towers of Infinity and One Rincon Hill).

Looking forward, we see an additional 1,100 new market rate condominiums that are likely to start marketing/selling by the end of 2008, and another 1,800 that are either already under construction or that we believe have a chance of breaking ground within the next five months. And beyond that (and for building by building updates), you’ll just have to keep plugging in.

∙ SocketSite’s Complete Inventory Index (Cii): Q3 2006 [SocketSite

∙ SocketSite’s Complete Inventory Index (Cii): Q1 2007 [SocketSite]

∙ SocketSite’s Complete Inventory Index (Cii): Q3 2007 [SocketSite]

Socketsite: for the 200 new housing units, are there any metrics as to when the last of the 200 new developments will be completed? Or the average length of time the 200 new projects will take?

I hope my questions made sense. Thanks!

just to be clear

instead of the current supply of 1085 units(or 4 months) that we are currently being fed by realtors, there is actually a supply of 4255 units (15 months) on the market now and 1100 more units (4 months supply) coming to market in 2H 08

whoa nelly!!!!!!

Thank you socketsite for producing this. You are truly providing a great service to the community by providing transparency to a smoke and mirrors industry./

It seems you’ve been calculating the Cii for a while now, and I think it would be helpful to show how the totals change over time. Might I suggest that you start stacking the three bars in your chart to represent the total inventory for each quarter in order to compare with prior quarters?

Condo sales for Jan 08 stand at 103 – down about 40% from Jan04/Jan05/Jan06. Listed condo sales averaged about 3,400 per year for 2004-06 (280 per month). So, if 2008 stays down by about 40%, that’s a run rate of about 2,000 for the year (or 170 listed sales per month). The DataQuick reported sales (for SFH & condos in SF) in recent months have been running about 50-80 units higher than the MLS total. Some have attributed this difference to DQ somehow capturing unlisted sales (presumably most of these would be condos). So, if we add say 70 units to the 2008 average pace of 170, we get a combined listed-unlisted run rate of about 240 units per month. The current condo inventory is 610 listed units + 3,170 unlisted units. The estimated months of supply implied by this is therefore about 15.8 (3,780 / 240). This is not quite at Miami’s level – but it’s still pretty high.

It’ll be interesting to see how this plays out. Ultimately, this will be good for condo buyers: tons of inventory and most of it new construction and markedly lower prices.

The SFH selection though is really odd. Almost half the the inventory is located in district 10. District 7 only has one listed SFH available for under 5 million. I wonder if people are afraid to list period or are selling their homes off market?

scary. scary. Keep repeating to yourself: “I have a long-term perspective.”

LOL @ Spencer. “Fed by realtors.” Realtors are kept out of the equation, initially, and many of the properties AREN’T EVEN FINISHED YET.

And I’ll tell you what, I look at statistics such as these and the first thought that comes to my mind is this. Older condos are going to be the first entity to see larger price adjustments.

just stating the obvious:

some of the “coming to market” condos may never get built… so although it’s good to know they’re out there, I wouldn’t put too much stock into that.

but there is a sizeable amount of inventory off the MLS, which is why it’s nice to see the Cii once in a while.

fluj: welcome back. Glad socketsite’s got you hooked.

“LOL @ Spencer. “Fed by realtors.” Realtors are kept out of the equation, initially, and many of the properties AREN’T EVEN FINISHED YET.”

i didn’t count those in my analysis. opnly thre properties in the left and middle column. Have you actually got a hold of any of those straws you’re grasping for?

I know we’re doing “snapshot in time” with the dates, but as of today, MLS inventory is over 1,200.

There should really be a separate index for new south of market condos/lofts because it seems like that is a market unto itself. I know I wouldn’t consider living there and many others feel the same way, thus for us it doesn’t really matter if there are lots of new towers and thousands of units. The condos are too expensive and the neighborhood is simply not for families. For those who like the south of Market area and are into high rise living, (and of course can afford $1000/sq. ft) there are lots of options that didn’t exist 5 or 6 years ago.

I also think it’s a little premature to be including the second Rincon Hill tower and any other tower that hasn’t even broken ground yet in the middle column.

3475 units available in Q3 07 vs. 4255 units available in Q1 08.

that’s a 22% increase in inventory in 6 months.

I know you counted the middle, Spencer. That was your error. The middle column includes such unfinished and not particularly realtor related properties as the Arterra, Infinity and the Hayes not to mention other forthcoming properties. No straws bro. Just you dissing realtors with a broad stroke.

Spencer/FSBO – not quite sure where you’re getting your sales per month numbers from as MLS does not account for all of the sales (especially in new developments). While Dataquick’s median price numbers leave a lot to be desired, their overall sales numbers are considered pretty accurate. Dataquick shows 6,294 sales for SF county for all of 2007 as follows (find the Bay Area articles at http://www.dqnews.com/):

1 402

2 375

3 640

4 568

5 616

6 633

7 564

8 577

9 469

10 526

11 479

12 445

That equals approximately 525 sales per month. So this means a current supply of 4.9 months of inventory and a supply of 8.1 months of inventory when including the additional 1,700 near term availabilities. Generally a 6-9 month supply is considered a balanced market, less than that is considered a sellers market and more than that a buyers market. So the supply/demand equation still looks decent. However, slower sales and increasing supply have pushed this up from a rate typically below 3 months of supply in SF, so the increase to almost 5 months is obviously not positive.

Many thanks to Adam/Socketsite for this research – with the large amount of new construction in the city of late the MLS numbers do not come even close to painting the whole picture.

OK FLUJ. Let’s just look at the bottom of the middle column. Why has that inventory gone up 300% over the past 6 months. Who are the people who are choosing not to put properties on MLS?

225 in Q3 07 vs. 660 in Q1 08

Spencer – the thing that aggravates Fluj (as well as others like myself) is comments from you like … ‘providing transparency to a smoke and mirrors industry’ … and ‘have you gotten hold of any of those straws you are grasping for’ … etc. So much of the posts on this site are people lashing out at each other … not addressing the topics or posts in general… etc. Nobody is an expert, in my opinion. Everyone knows that with new developments only a minute handful of the actual overall total of units are actually listed in the MLS. It has nothing to do with smoke and mirrors.

Miles – My understanding is that the DQ numbers include both condos and SFH’s. My analysis above focused only on condos since that is where the growth in supply is occuring. As I indicated, I’m inferring that the delta between DQ sales and MLS sales (DQ is always higher) is largely due to unlisted condos sales. It was just a SWAG on my part – I don’t know anything about DQ’s methodology. It does seem like the two markets (condos / SFH) are going to diverge somewhat given this big increase in condo supply (and maybe differences in credit availability for potential buyers). I agree with your point that the overall market still looks pretty balanced (particularly compared to other regions), but I think that condo prices are likely be under pressure.

Given the rising inventories, I’d like to hear from potential buyers who are actively looking.

Are there more units being listed that you’d want to buy and that are being offered at ‘market price’ (however you define that)?

I liked the comment about showing these graphs in three dimensions, showing what’s happened over time. In a time series, Adam is showing the third column going down substantially (thank god) as “potential” projects are delayed or cancelled.

“In a time series, Adam is showing the third column going down substantially (thank god) as “potential” projects are delayed or cancelled [sic: 1 ‘L’ in canceled].”

The projects will get built. Developers may be walking away from options on land at one price because they project new lower prices and the land prices don’t work out. But it just means the owners of the land just have to accept lower prices.

If the land owners want to sell, they’ll take the lower price, and the projects will get built like they were supposed to. It’s not like developers are clamoring to build offices at the start of a recession, so there isn’t much competing use for the land. Thus, almost all of the projects will get built. The story isn’t over for those projects, it’s just the market sorting itself out.

As for fluj’s comment, I thought the very same thing. That will *initially* put even more pressure on the condos that aren’t brand new. But that market will also sort itself out and then this inventory puts pressure on even the new ones, as the inventory rises.

And the comment that south of market is a different neighborhood and should be factored out, that is so not true. If condos south of market were selling for $1, even you, anono, would move there, thereby removing one more unit of demand (or adding one of supply) to the non-SOMA market, thereby putting downward pressure on non-SOMA prices. So it’s just a pricing issue. When the market is in equilibrium, the increased supply of SOMA condos affect the prices of the non-SOMA condos. Although markets are not always in equilibrium, they tend to reach it.

Inventory has been ticking up. Quality of listings down. Prices still too high. Top Tier places still selling like hot-cakes.

Eddy, what is a “Top Tier place”?

Partially agree with eddy. Not many five star listings on the market but wasn’t expect to see them this early in the year anyway. More three star listings. Not as much junk.

Still expensive and competition for great houses but not as much. More choices and less urgency South of Market.

tipster,

you really think south of market condos will ever be priced low enough that families and the sub 200K income crowd will move there in any meaningful numbers? There are virtually no parks, schools or hospitals, and the entire neighborhood is getting pretty expensive. Prices would have to come way down, from $1000+/sq ft. to $500/sq. ft. That is not going to happen. People bought up thousands of units of ordinary apartments (“ordinary” may be a generous description) in places like Palms, Beacon, Berry St. buildings and others for very high prices and all of the new projects South of Market will be similarly priced.

South of Market is simply not like any other part of the city I would consider living in, and won’t be anytime soon no matter how much prices drop. I find it sterile and boring, with not much difference between the buildings- at least the ones where a 2br is available for less than $1M. However, when the $600K units at the Infinity show up count me in.

The people choosing not to put properties into the MLS aren’t realtors and I’m pretty sure you already know that.

I’m not picking on anyone, but why do people keep using the $1,000/sq.ft. metric for Soma? This is a fantasy number, folks.

Take a look at the MLS and just scroll through listings in D9. Most all of the Soma and South Beach listings are out there at $700 to $800 per square foot, not $1,000. Nicer ones are higher than $800, worse ones are below $700, but $700 to $800 is the basic range.

Even the posters on here who bought at Infinity and ORH usually brag about how they got a great deal because they only paid like $850 per square foot for new construction.

So why is everyone throwing out $1,000 as a magic baseline?

TopTier = gut remodels, high end finishes, sweet views or great locations, parking and good floor plans.

@sanfrantim,

I am a condo buyer in the market, but decided to remove myself from the market about 4 months ago, because I could see the quality of the inventory improving. However, the prices for 1-2 bedroom condos are still high, but I am starting to see some better deals on SOMA lofts. I, however, agree with “anono” and do not want to live in SOMA. I do not have children or a family (single male), but I prefer living in a neighborhood. I currently live in mid-market, and am anxious to move to a condo in a neighborhood. The 1-2 bedroom condos in neighborhoods have not decreased in price. I would expect those expensive SOMA lofts with no established neighborhood and lots of vehicle traffic to further drop in prices.

On Dude’s point, the median numbers for listed SOMA condos are $580,000 list price, $657/sf, and 933 sf. And average DOM is 84, and only 5 of 67 units were sold last week. So places are not leaping off the store shelves even at these serious price discounts. Even the medians for the top quartile are $874,000 and 1529 sf.

We don’t have much farther to go to get to the $500/sf level that anono says is not going to happen, and we are heading quickly in that direction. $1000/sf really is a fantasy. Something may be going for that, but that is the rare unit and far from typical.

magic 8 ball says:

500/sq ft median in Soma in Q2 09.

anon@3:58PM – are you looking at listings for District 9 – F? I’m seeing prices that are a bit higher than the ones stated above.

FSBO, I was looking at Altos’ numbers. I think they organize by zip code. 94103 here.

@ sanfrantim: I WAS actively looking until last week. I am interested in a 2/2 new development (condos) in SoMa/SoBe, but as many as there are of these, the options are very limited, considering size and price, as I’ve mentioned before. At these prices, I’m saying “no thanks.” A unit that I WAS interested in is $900/sq. ft., and at the moment, I don’t feel it’s worth it. So until these developers/sellers realize that we’re not living in 2005/2006 anymore, then they’ve just lost a buyer.

For those looking at SoMa Lofts a quick check of craigslist shows there are similar lofts in East Bay going in the $300-400 sqr ft range … just saying

badlydrawn and other EB boosters:

The EB is not an option for everyone. I’m tired of reading posts on this thread that accuse citydwellers of snobbish attachment to SF. My husband works in downtown SF and I work in Silicon Valley. We know many other couples in the same situation. We aren’t city snobs. It’s about the commutes.

“I’m tired of reading posts on this thread that accuse citydwellers of snobbish attachment to SF. My husband works in downtown SF and I work in Silicon Valley. We know many other couples in the same situation. We aren’t city snobs. It’s about the commutes.”

Then don’t read them, it doesn’t apply to you. The downward scroll works nicely on most computers.

Crockergal:

You can’t tell if a post doesn’t “apply to you” if you don’t read it.

Burble, I wasn’t trying to accuse people of being snobbish and I understand there are a variety of issues that drive people’s housing decisions (heck I could live anywhere in the US and keep the same job and salary but I choose to live in SF) … I was just pointing out that the same SoMa loft can be purchsed in East Bay for about half as much.

Personally what has me looking at East Bay is a friends experience with a recent purchase of a 3 bedroom near the Castro. He got a nice place is doing some remodeling and all is good. Except, he is in the classic situation of being ‘house poor’. A big chunk of his money is going to paying for the mortgage and remodeling, he has taken on a roommate to help with expenses, and he rarely goes out in order to keep his spending down. He even talks about ‘cashing out’ his recent purchase and moving to something new even though he bought less then 2 years ago.

I am not trying to knock his decision and it is certainly reasonable to expect to make sacrifices, like curtailing spending and taking on roommates to buy a home, especially in a city as expensive as SF.

However, I can’t help think that he could have found the same 3 bedroom in the East bay and paid half as much and be much less stressed out, spend time in SF, and have a similar commute to his San Jose job.

It’s a personal decision for everyone but I, personally, am having trouble reconciling spending 800k on a home and commuting to Silicon Valley (which is a long commute from SF as it is) versus spending 400k on the same home across the bay and having about the same commute and still have money to go out and go on vacations and such and not feel ‘trapped’ in my new home.

I am not trying to attack anyone’s decisions I guess I am just trying to spark a bit of discussion about the huge price differential between living in the city of SF compared to living in other nearby parts of the bay.

I know it’s a bit offtopic but I thought the comments surrounding price per square foot justified a quick comparison.

Burble, I haven’t looked much on the Peninsula/SB, but I’m sure you have, given your commute predicament.

Are any of those areas (Daly City, So SF, San Bruno, Pacifica) seeing the price declines that parts of the EB are seeing?

Wow, people are getting a little testy!

“My husband works in downtown SF and I work in Silicon Valley. We know many other couples in the same situation.”

Don’t sweat it! The upcoming recession/depression will take care of many of these employment “problems”. 🙂

“Are any of those areas (Daly City, So SF, San Bruno, Pacifica) seeing the price declines that parts of the EB are seeing?”

Generally yes, depending on area. Lafayette and Orinda are probably holding out better than Daly City or So SF, which are holding up better than Walnut Creek. Regardless of the gradations, prices on the peninsula are falling:

http://www.insidebayarea.com/sanmateocountytimes/localnews/ci_7920648

you really think south of market condos will ever be priced low enough that families and the sub 200K income crowd will move there in any meaningful numbers? There are virtually no parks, schools or hospitals, and the entire neighborhood is getting pretty expensive.

No families in Soma? Has anyone been by Delancey Street Cafe? (At least I think that’s what it’s called). Back when I was living in the area(2000) you wouldn’t see a baby for days. A year or two ago I was there – a bulletin board packed with baby photos.

And I recently met a mom with two kids who sold her place in Noe and moved to SOMA.

Families are moving to SOMA.

I used to live there seven years ago and NEVER saw a kid. Then last year I was at Delancy Street Cafe(?) and whoa – a bulletin board packed with baby pictures.

This crowd probably doesn’t realize it but the area is convenient to two very up-and-coming private schools (Friends and Live Oak). I met a family with two kids – they sold their place in Noe and moved to SOMA. SOMA is not an island.

badlydrawn:

You are right, your post was not accusatory at all. It just triggered a response that had been building up for a while.

Frankly, I would love to have an Arts and Crafts house in a sunny neighborhood over in the EB. We actually bid on some places over there before I got this job in SV.

Foolio:

I’ve been looking at Millbrae because BART is there so it could work pretty well, also the schools are supposed to be good. It’s really expensive but it seems like things aren’t moving at all, so maybe prices will come down. The question for me, and probably for a lot of other people on SS is, how long will that take?

@ anon at 10:27AM

Regarding the sub $200K income crowd, a couple with a combined annual income of $150K can afford a mortgage payment of $4K/month using the 32% back-end rule. At 6% on a 30-year fixed, that pays ~$660K of mortgage. Assuming they’ve saved 10% down, they can buy ~$730K of property (they’d better love ramen noodles, but the math would work).

And according to the MLS, there are 155 properties currently listed for $730K or less in district 9, and 55 of them are 2-bedrooms. I believe Soma Grand is selling 2-bedrooms in this price range as well.

So the long-winded answer is yes, the sub $200K income crowd will be able to live there, especially now that prices are falling, and will likely keep falling through 2009. No idea if families will want to live there, but they at least have the ability.

Dude,

Does your 32% rule in the mortgage calculation include any other debt (car payment, credit card, student loan)? And a mortgage of 660K – that would be a jumbo (at least for now) at 6%. Rate seems low.

Thanks.

fred – admittedly, the 32% assumes the couple has no other debt.

Let’s assume 28% max ratio and 6.55% interest. They can finance ~$550K, which is a purchase amount of ~$610K with 10% down. There are 84 properties listed for $610K or less in district 9, 22 of which are 2 bedrooms.

This still ignores closing costs, HOA dues, etc. More importantly, it also ignores that our hypothetical couple is better served renting an equivalent unit for a fraction of the cost of owning and waiting for prices to fall to reasonable levels. But that’s another topic altogether.

Not to belabor this – I was just trying to convey that a couple making the median SF income ($75K/year each) has options.

ok thanks, too bad we can’t all be rich like Satchel and Tipster 😉

150K salary can afford a $730,000 home with a $4K per month mortgage. I don’t think so.

150K salary can maybe afford a $500k home with a $3000 mortgage.

I don’t think anyone making even $200K should be paying more than $600K for a home.

“150K salary can afford a $730,000 home with a $4K per month mortgage. I don’t think so.”

Most likely, a couple with 150K total salary is in AMT, with a marginal tax rate of 44%(AMT + state). That 4K/month mortgage is really 2200/month after the tax deduction.

2200/month won’t rent them anything nice.

A couple with total salary of $150K is likely not in AMT if they contribute to retirement accounts, and certainly would strain to purchase a 700K plus property today (no I/O ARMS anymore?)

I guess when I posted above about how expensive SOMA is I was focusing on new(ish) 2 BR 2 BA 1PKG condos. We bought the same thing in the Mission for substantially less. I don’t see many of these in SOMA selling for less than 850K- plus double the HOA’s I’m currently paying, and I can’t even imagine moving to someplace like Soma Grand much less raising a kid there (I work at the new Federal Building and I don’t think you could pay me to live at that location). I have no doubt there are some families in SOMA, but not many. And those private schools?

You need to be making a heck of a lot more than 200K to buy the condo in SOMA and send the kids to private school. At that point, you can move to Marin or the Peninsula or Albany and just stick the money into a more expensive house. At least the mortgage interest and property taxes are deductible. $20K private school tuition for a five year old is not.

“Most likely, a couple with 150K total salary is in AMT, with a marginal tax rate of 44%(AMT + state). That 4K/month mortgage is really 2200/month after the tax deduction.”

This is wrong on so many levels, but it is a common misconception among buyers (and one that is reinforced by advertising, REIC, etc.).

First, the AMT for income under about 175K is 26%. The California brackets are more compressed than the Federal ones, but at a $150K income level we are only talking about marginal rates of 35%, at most, under the AMT regime. Not that any couple here with income of only $150K (assuming W-2 income) really has any serious AMT issues anyway.

The Federal brackets are fairly generous, and the 28% bracket is the MAX that would apply to joint incomes under about $200K (2008 figures). So, even under the regular tax regime, incomes of only $150K are only facing at MAX 35-37% marginal rates (much lower on a blended basis, of course).

Arguments and illustrations that directly deflate morgage interest payments by assumed marginal rates miss a number of VERY important considerations, and so should basically be ignored.

First, property tax must be taken into consideration. $4k morgage (PITI) equates to a morgtage of roughly $750K, which of course will not buy you too much in SF. Assuming some downpayment (maybe 10% – just for the argument), you are looking at a property of $835K, which means an additional $9.5K in prop 13 taxes. Insurance (not deductible) needs to be added in there too, say another $2-3K annualized?

Second, these simple translations of PITI ignore the value of the standard deduction for married couples ($11K for 2008). In other words, you need to spend (waste) $11K on interest payments on your mortgage before you derive any benefit from your interest “deduction”.

Bottom line, before buying, one really needs to run the numbers. Just for the heck of it, I am going to run the numbers, and I’ll post them later. My strong suspicion is that a $4k interest payment (together with the additional property tax that is associated with such a purchase) when all is said and done will wind up being equivalent on an after tax basis to a rent of somewhere north of $3500 (at the assumed $150K income level) but like I said, let me run the numbers and I will post them later!!

“2200/month won’t rent them anything nice.”

Posted by: John at February 6, 2008 11:59 AM

I rent a very nice 2bdrm place in Pac Hts with parking for less than that

I’ve posted this a number of times, but it bears repeating. $3.1K per month gets me a 4/3 (+ unwarranted bathroom in the lower garage level), 2800-3000 square feet in one of the nicest neighborhoods in District 4, unobstructed ocean views from every room of the house (except my office – yeah, it has an office! – and 2 of the three bathrooms), and 1000+ square feet of garage/workshop space. The deals are out there, prop 13 assures it (lots of people paying only $2K per year tax on houses worth $1.5MM+, so might as well hold on to the place and “save it for my kids”), but I guess they require a little looking and a willingness to consider neighborhoods other than the glamour ones.

The median FAMILY income (Money Magazine) for SF is $88,450. If we use that no., you’ve got only a handful of families that can afford to buy.

“First, the AMT for income under about 175K is 26%.”

Check it yourself. income under AMT reduces exemptions at 7%. The EFFECTIVE tax rate under AMT is 26% + 7% + 9.3%= 42.3%.

You only get fed AMT tax rate of 28% if your income is above around 500K.

John,

Exemptions are small relative to income levels of $150K. Reduction of them does not affect much, I’m afraid….

Anyway, though, I DID run the numbers, using the (perhaps) unrealistic $150K joint income figures.

Bottom line, at $150K joint income, and assuming NO other deductions than state income tax and property tax and morgtage, a $4K mortgage payment is equivalent to a $3,229 per month rent payment, for an effective savings of just over 19%. Under more reasonable assumptions, the savings are LESS.

Note that these are unrealistic assumptions, especially because there are other deductions available to nonproperty owners, primarily 401(k), IRA and HSA deductions, but these are ignored for the purpose of the comparison. Additionally, the nondeductible expenses of HOA and insurance are also ignored. The net effect of ignoring these available deductions and these obvious nondeductible expenses would drive the comparable rent figure higher. My guess is (at the $150K income level), a $4K mortgage payment is equivalent to a $4K rent payment.

For those who are interested, here are the numbers.

Home is assumed to cost $835K. 10% down. Mortgage of $750K leads to approximately a $4K deductible interest payment per month (PITI is ignored, as that makes the comparison even more unfavorable for the homeowner!).

With NO OTHER deductions, the joint filer at $150K W-2 income (no dependents) incurs a Federal tax liability of $26,093 and a CA tax liability of $8,719, leading to a total tax bill of $34,812 (all 2007 numbers). Bracket inflation for 2008 means that 2008 numbers will be LOWER. As expected, AMT issues are not existent at these income levels, although they might come into account if the homeowner has children. THis possibility was ignored, as the presence of dependent children results in an even more unfavorable comparison for the homeowner (children come with tax benefits “built-in”!).

Adding deductible interest expense on a home of $48,000 and deductible state property tax of $9,500 (1.14% * the assumed $835K price) changes the tax liability. The new numbers are Federal tax liability of $12,029 and state tax liability of $4,025, leading to a total of 16,054. In other words, the “tax deduction value” is equal to $18,758 (34,012 minus 16,054), or $1,563 PER MONTH.

Mortage of $4K plus monthly property tax of $792 = $4,792 TOTAL of cash expenses that are deductible. Subtracting out the value of the tax benefit ($1,563) yields a rental equivalent $3,229, NOT the $2200 figure John referred to.

IMPORTANTLY, monthly HOA and maintenance and insurance needs to be added to these figures to get a true rental equivalent price. Maybe an additional $500 total? Maybe $750? Neither of these would be off the mark. Additionally, we assume a small down payment ($85K), and this would generate at least $2K income on an after tax basis even if invested in California triple tax free GO’s. Maybe another $125-175 per month, depending on how far out the yield curve you invest. So, an estimate of north of $4,000 is not off the mark. In fact, my initial guess of $3,500 was low.

Last, I want to stress that everyone has some deductions at the $150K level, even if only 401(k)/IRA and state tax. These deductions serve to RAISE the effective cost of purchasing a home versus renting it, as the taxpayer’s effective tax rate is lowered (coordinately lowering the value of individual property tax and mortgage interest dedusctions).

So, the TRUE choice is buy and $835K home or rent something for about $4K per month, at the $150K joint income level. For me the answer is obvious (even more so in my case, because I rent a $1.4MM home for $3.1K per month, AND my effective tax rate is much lower even though my income is significantly higher than $150K – thank you George Bush for our investor tax cuts!!).

Satchel,

Thanks for running the numbers. I wish everyone would do this level of analysis when thinking about buying. My wife and I saw a mortgage broker recently and he fed us the same garbage that John did (marginal rate times interest and prop. tax paid) but running the numbers with our tax person led to very different results. The tax savings was nowhere near what we thought it would be.

Satchel – I would echo CS’s comments on a very comprehensive analysis. It’s surprising how much the simple marginal rate method overstates the tax benefits. You have to work up through the brackets and thresholds with actual numbers to get the real net benefit. The hypothetical couple might only take home 58 cents of the last incremental dollar they earned, but you showed us that, in most cases, the deductions are worth a lot less than 42%. And, as you point out for you cap gains / carried interest guys, the mortgage deduction is worth even less. (Almost makes me feel sorry for Steven Schwarzman and John Paulson.)

Thanks for reading my ramblings. For some strange reason (related to the fact that this housing bubble is really going to morph into something devastating for the US economy shortly), I feel some need to get some sensible analysis out there!

About tax issues and SF real estate specifically, the picture darkens even more when you consider the incomes required to support these prices as well as the level of the prices themselves.

In general, single payers will pay higher effective tax rates, and so the rent vs. buy calculation above skews a little more towards buying. Similarly, as “earned” income goes up, the value of the tax deduction increases somewhat. As far as I can tell, these considerations (plus the desirability of having stability when one gets into his child-raising years) are primarily why one would expect to find the rent vs. buy decision to change as one moves up the desirability of housing ladder. In a simplified way, a 1/1 condo shoebox should cost MORE to rent than to buy, because the owner should accrue some economic benefit. A nice large 4/4 SFH should cost less (in equilibrium) because the owner is accruing significant tax (because his income is higher) and noneconomic (stable place to raise a family) benefits.

But because SF prices are so high, things are a little screwy. Only interest on a maximum of $1MM of acquisition debt ($100K additional if you add a HELOC in there) is deductible. If you are in the market for a nice SFH to raise your family, even $1.1MM doesn’t get you too much right now. So, many people are facing the full brunt of at least part of the cash interest cost.

Also, at higher income levels, taxpayers begin to face the phaseouts of itemized mortgage deductions (among most other deductions) – over about $150K for singles and $230K for couples – something the REIC will NEVER talk about of course, but which should be considered when we’re talking about $1MM properties. These phaseouts THEMSELVES are being phased out under the 2003 tax revisions, but the Democrats are going to remove this benefit for those making over $150K and $230K as soon as they can (the phaseouts of the phaseouts expire in 2010, unless extended, meaning that the old phaseouts will “snap back”). What a mess!

Good stuff Satchel. This is another area where the risk management folks at the RE brokers (assuming they exist) should be apoplectic. The amount of misinformation being put out there by RE agents on this issue is amazing. I recall when we were in the market 10 years ago how one well-known SF realtor (I’ll call him “Dalmatian”) was trying to sell us on buying a 2-flat and fed us an analysis of the tax benefits from depreciation on the rental unit. One quick call to my tax guy drew hearty laughs as he explained that Dalmatian was either an idiot or a crook because my income was too high to realize any breaks from depreciation. We promptly switched realtors.

A quick look at local realtor web pages reveals rampant misinformation about tax benefits as well as “guarantees” about investment returns — here is one: “with interest rates heading back down, property values WON’T be falling in SF.” A realtor has no obligation to give tax or investment advice, but if he/she does and it turns out to be wrong, liability would be tough to avoid. And with property values heading down, the “I would not have bought it but for this erroneous information” case could result in significant damages — the decline in value. The brokerages really have to put an end to this.

I saw this article on another blog today from OC and is relevant to the discussion about affordability…..I agree with their analysis BTW. you need a $200K salary or income to buy a $600K house. if you make less than this, you shouldn’t be buying anything in SF.

$191,106 income needed to buy O.C. home

February 6th, 2008 · 72 Comments · posted by Jon Lansner

Got a spare $191,106? That’s the household income required to buy the typical O.C. home (estimated price tag: $585,000) in 2007’s third quarter, according to the Center for Housing Policy. That ranked O.C. as No. 5 for biggest salary needed to buy a home among 201 major U.S. markets. (San Francisco was first, by the way!)

The good news — and this is a stretch at optimism — is that this required lofty paycheck is 10.88% less than the $214,447 required to buy a year earlier. (That ranked us #4 for ‘06.) You can thank a 7% price drop for much of that “improvement.”

The center used homebuilder home pricing and a proprietary salary database to arrive at that affordability measure. It assumes the buyer puts 10% down and pays his loan plus mortgage insurance, taxes and homeowners insurance. The assumption is that total house payments are no more than 28% of household income.

Dear Socketsite:

Any chance the time series data can be published in a spreadsheet so I don’t have to assemble my own?