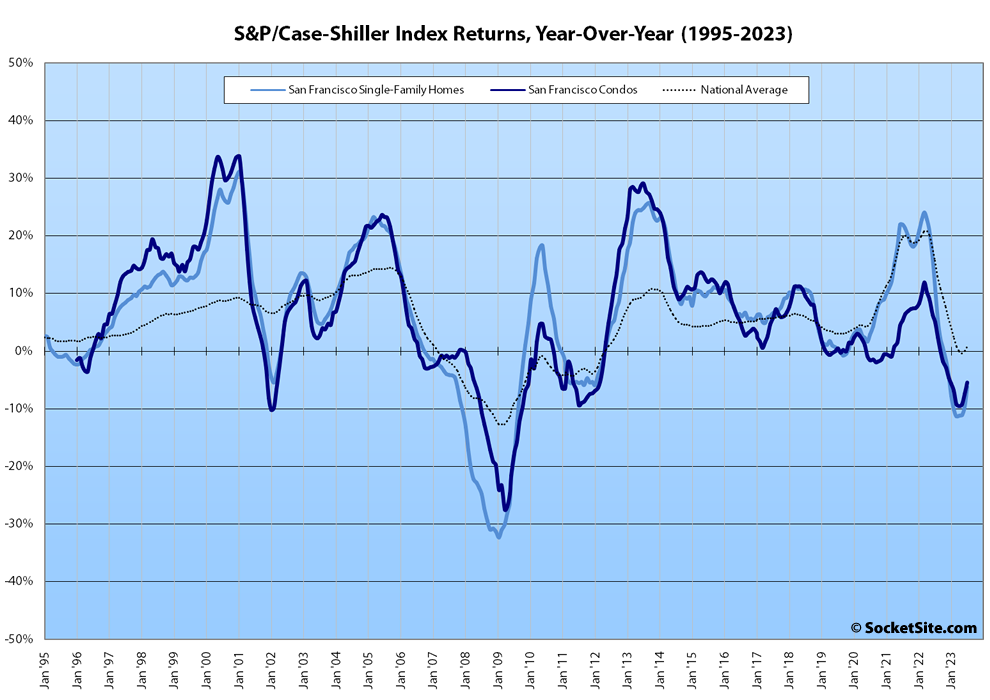

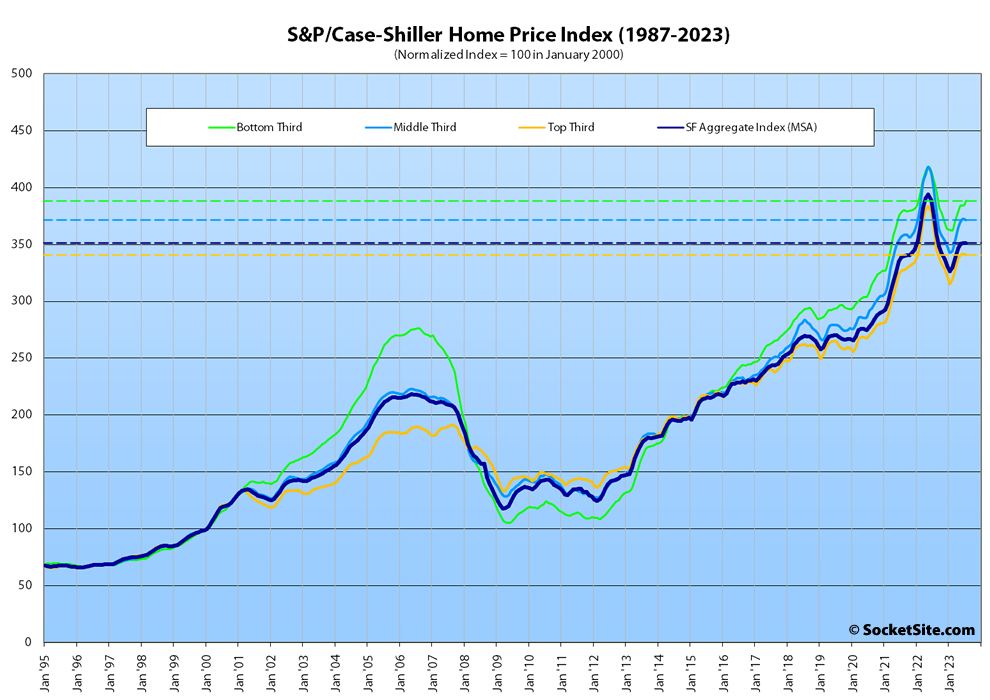

Having inched up an upwardly revised 0.2 percent in June, the S&P CoreLogic Case-Shiller Index for single-family home values within the San Francisco Metropolitan Area (i.e., “San Francisco,” which includes the East Bay, North Bay and Peninsula) inched up 0.1 percent in July, driven by uptick for the least expensive third of the market, but was down 6.2 percent on a year-over-year basis and 10.8 percent below last year’s peak.

At a more granular level, while the index for the least expensive third of the Bay Area market ticked up 1.1 percent in July and was only down 4.9 percent versus the same time last year, the index for the middle tier of the market inched down 0.2 percent and was down 6.5 percent, year-over-year, with the index for the top third of the market slipping 0.1 percent for a year-over-year decline of 6.0 percent.

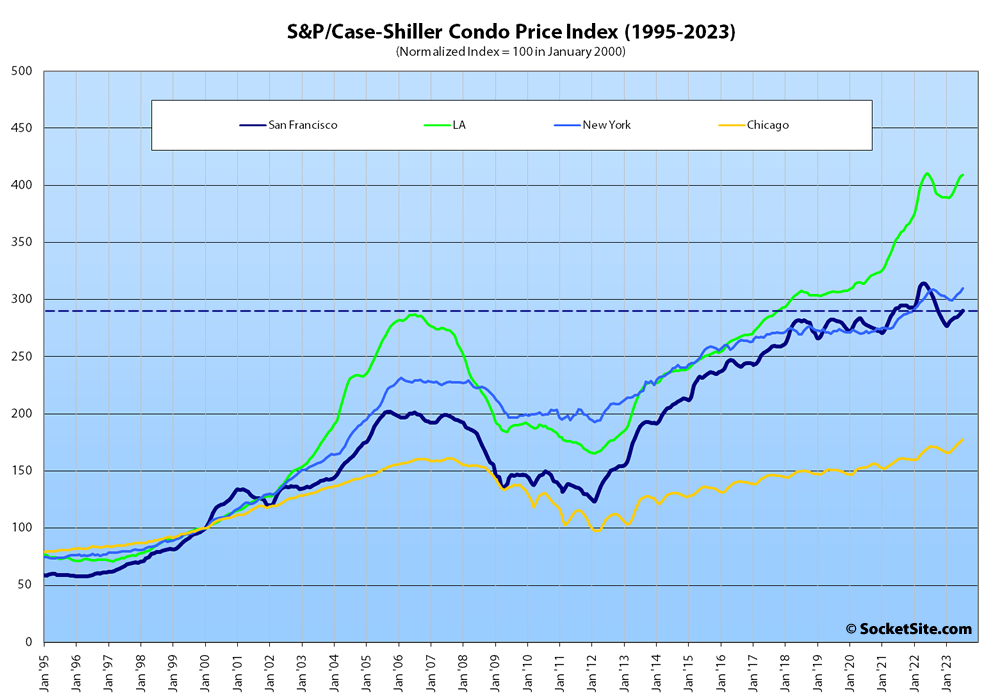

At the same time, the index for Bay Area condo values, which remains a leading indicator for the market as a whole, ticked up another (1) percent but was still down 5.4 percent on a year-over-year basis, with the indexes for Los Angeles, Chicago and New York all recording small year-over-year gains of 0.5 percent, 3.6 percent and 0.5 percent respectively.

At the same time, the national home price index inched up 0.6 percent from June to July and was one (1) percent higher than at the same time last year, marking the first year-over-year gain in four months, with Chicago up 4.4 percent, followed by Cleveland (up 4.0 percent) and New York (up 3.8 percent), versus the 6.2 percent decline for San Francisco, a 5.5 percent year-over-year decline for Seattle, and the average rate for a benchmark 30-year mortgage having ticked up another 40 basis points since.

Our standard SocketSite S&P/Case-Shiller footnote: The S&P/Case-Shiller home price indices include San Francisco, San Mateo, Marin, Contra Costa and Alameda in the “San Francisco” index (i.e., greater MSA) and are imperfect in factoring out changes in property values due to improvements versus appreciation (although they try their best).