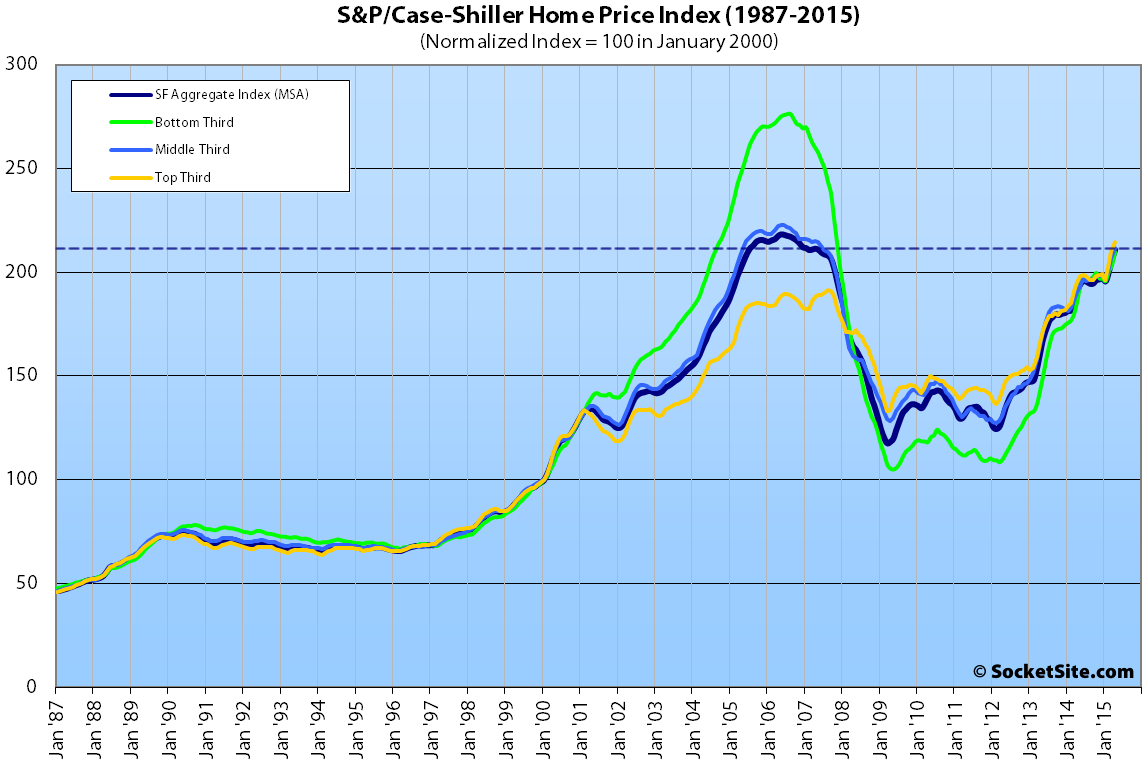

Single-family home values within the San Francisco Metropolitan Area gained 1.3 percent in May, while condominium values gained 1.1 percent, according to the latest S&P Case-Shiller Home Price Index.

The San Francisco index for single-family homes is running 9.7 percent higher on a year-over-year basis. And having gained 58 percent since January 2010, the aggregate index is within 2.2 percent of its 2006 peak.

The index for the bottom third of the market gained 1.4 percent in May and is running 9.1 percent higher versus the same time last year; the index for middle third of the market gained 1.7 percent, up 11.3 percent year-over-year; and the index for the top third of the market increased 1.3 percent to a new all-time high, up 9.8 percent year-over-year.

According to the index, single-family home values for the bottom third of the market in the San Francisco MSA have doubled since 2009 and are back to just below September 2004 levels (23 percent below an August 2006 peak); the middle third is back to June 2005 levels (3 percent below a May 2006 peak); and home values for the top third of the market are at an all-time high, 13.6 percent above their previous peak in August of 2007.

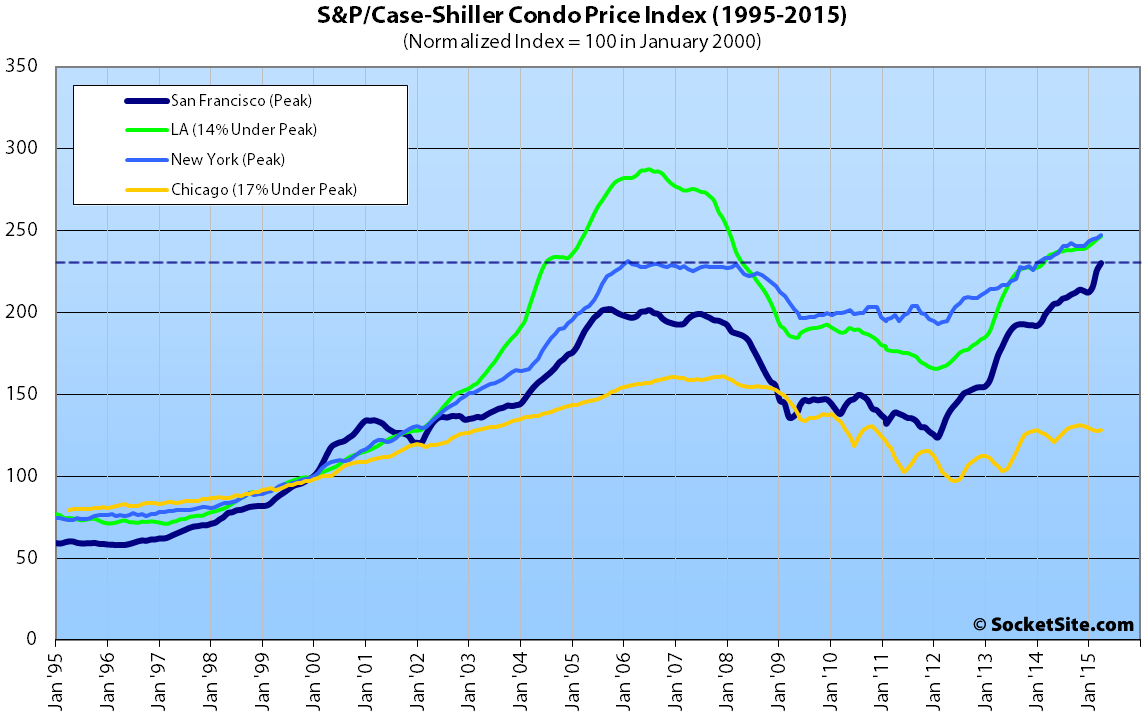

San Francisco condo values gained 1.1 percent in May and are running 13.4 percent higher on a year-over-year basis, 15.1 percent higher than at the peak of the previous cycle in October 2005 and a new all-time high.

For the broader 10-City U.S. composite index, home values gained 1.1 percent in May and are running 4.7 percent higher on a year-over-year basis but remain 14.3 percent below a June 2006 peak.

From David Blitzer, the Managing Director and Chairman of the Index Committee at S&P Dow Jones Indices:

“Nationally, single family home price increases have settled into a steady 4%-5% annual pace following the double-digit bubbly pattern of 2013. Over the next two years or so, the rate of home price increases is more likely to slow than to accelerate. Prices are increasing about twice as fast as inflation or wages. Moreover, other housing measures are less robust. Housing starts are only at about 1.2 million units annually, and only about half of total starts are single family homes. Sales of new homes are low compared to sales of existing homes.”

The long-term average annual home price appreciation for San Francisco measured 4.2 percent back in 2006, at which point the city was deemed “bubble-proof,” in part due to the inability to build on large swaths of underdeveloped land, such as Treasure Island.

Our standard SocketSite S&P/Case-Shiller footnote: The S&P/Case-Shiller home price indices include San Francisco, San Mateo, Marin, Contra Costa, and Alameda in the “San Francisco” index (i.e., greater MSA) and are imperfect in factoring out changes in property values due to improvements versus appreciation (although they try their best).

Does case do a London profile? Would be nice to see that overlay.

My basic hypothesis here is that so long as the three tiers are moving in unison were are not likely to see any one tier experience a burst. Things seem to be moving in conjunction.

i bought my place in Jan 2012. I ahd no idea that would be the exact bottom. I got really lucky as I see now that Jan 2012 IS the EXACT bottom on the condo chart

Not that I would claim to be a “technician,” but consider the slope of these two time periods in the upper chart:

1. 1998 to 2001/2002; and

2. 2012/2013 to now.

They appear to be very similar.

If you want to believe “the trend is your friend,” and ignoring any other potentially relevant information, we have somewhere between 3-5 years left.

Also. To cover the inevitable “Generalize much?” comment. I actually do and my psychoanalyst notes that it good for my sense of wellbeing.

So remember, “Let’s be careful out there.” Gotta love Hill Street Blues!!