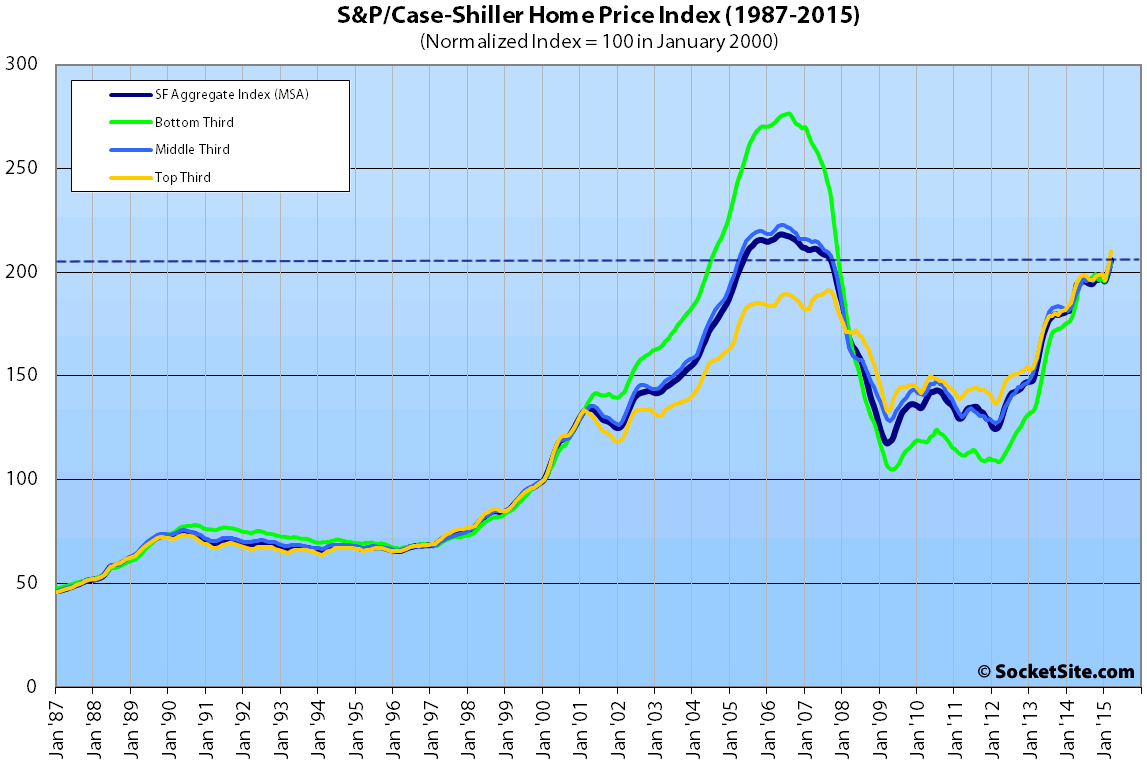

Single-family home and condominium values within the San Francisco Metropolitan Area gained 3.0 and 4.5 percent respectively from February to March, according to the latest S&P Case-Shiller Home Price Index.

The San Francisco index for single-family homes is running 10.3 percent higher on a year-over-year basis and is within 5.7 percent of a 2006 peak, having gained 52 percent since January of 2010.

The index for the bottom third of the market gained 1.8 percent in March and is running 12.8 percent higher versus the same time last year; the index for middle third of the market gained 3.1 percent, up 10.2 percent year-over-year; and the index for the top third of the market jumped 3.9 percent in March to a new all-time high and is up 10.1 percent year-over-year.

According to the index, single-family home values for the bottom third of the market in the San Francisco MSA are back to just above June 2004 levels (26 percent below an August 2006 peak); the middle third is back to just below April 2005 levels (8 percent below a May 2006 peak); and values for the top third of the market are now 9.8 percent above an August 2007 peak.

San Francisco condo values gained 4.5 percent in March and are running 13.2 percent higher on a year-over-year basis, 11.3 percent higher than at the previous cycle peak reached in October 2005.

For the broader 10-City U.S. composite index, home values gained 0.8 percent in March and are 4.7 percent higher on a year-over-year basis but remain 16.0 percent below a June 2006 peak.

Our standard SocketSite S&P/Case-Shiller footnote: The S&P/Case-Shiller home price indices include San Francisco, San Mateo, Marin, Contra Costa, and Alameda in the “San Francisco” index (i.e., greater MSA) and are imperfect in factoring out changes in property values due to improvements versus appreciation (although they try their best).

NIMBY + Moratoria + Historically Low Borrowing Rates + Frothy Tech Valuations + Rent Control + Finite Land Space + Prop 13 + Tight Lending Standards/High Quality Borrowers + Quaint Zoning Regulations + Sclerotic Planning Process

Completely wrong.

Three words: Desirability, lifestyle, location.

That’s all that matters.

“desirability” includes nearly all the factors soccermom rattled off though

No, none of them do. My 3 factors are.

Soccermom is completely right, Futurist is completely wrong. Such an overly simplistic point of view.

Right. So finite space has no bearing on desirability, you say.

The power and clarity of simplicity can speak volumes.

All of her so called factors can be found in almost all big cities. NY, Paris, London,etc. to name a few.

Actually maybe I should have just said “location, location, location”. That’s what really matters.

yes, her factors can be found in other desirable cities. and that has precisely what to do with your failed attempt to refute her points?

It doesn’t speak volumes in this case, which is airtight. So whatever you are smoking, please share! I am from NY, know it well, and there is nothing like Prop 13 there. Rent control is much weakened, is not affecting construction anymore, and new construction has been rampant for about 10 years now. The city has much developable land in the outer boroughs that is also near transit. Tech jobs are a relatively minor part of the economy there. I’m sure others who know those other cities could demolish your argument for those places.

+1

Yeah, and how does “desirability” explain the sharp run up from ’02 to ’07 and the subsequent crash and the recent re-run up? Pretty strange that “desirability” seem to go up and down so much.

is it? jobs is one simple answer.

“Desirability, lifestyle, location.” soccermom’s points are more valid. You could apply your 3 points to many many cities futurist.

All pre-existing conditions except:

1. Historically Low Borrowing Rates

2. Frothy Tech Valuations

3. Tight Lending Standards

Hmm…

Not really. The following two are different this time around.

“Tight Lending Standards/High Quality Borrowers” — not the same as the last bubble.

“Quaint Zoning Regulations + Sclerotic Planning Process” — things have worsened on these fronts for builders. The historic review process has become a monster. And building/planning has also become more difficult to negotiate for various reasons, whether bureaucratic, political, over democratization, or plain old bad management.

Well, except that there was that Potrero hill foreclosure last week that showed that >100% LTV lending for speculative buys is alive and well this time around.

It just isn’t being done by heavily regulated banks, but by other financial institutions.

I guess so? Wasn’t it 70% of the projected LTV, post flip? What wasn’t displayed was the underwriting or lack thereof of the borrower/projects. The Potrero borrower had bucks, I happen to know. Anyway, OK. There’s that. What of the other points I raised? They are positively not the same as the last bubble. You did not have Campos and his ilk flouting the [Eastern Neighborhoods Plan], either, come to think of it. Ole Willie Brown and Gavin wanted building, building, and more building. They didn’t gladhand both sides like Lee.

But beyond that one Potrero case there were small firms doing that bubbleesque type of lending and much larger Blackstone type firms looking to muscle in.

Building wise, if the Campos thing sticks that’s annoying, but I sure see a whole bunch of cranes and construction driving around town.

Yes, lots of cranes. Do you doubt there would be a lot more cranes if DBI wasn’t so screwy?

And…never mind the moratorium (or threat of it.)

SF RE status: it’s complicated

A++.

word

Indeed. There’s been talk of a plateau, but clearly that’s not happening. SF is by far the biggest monthly change, plus the largest YOY change. Good times.

Yes, very good times indeed. I’m not complaining.

Economics 101: “Desirability, lifestyle, location” = high demand

“NIMBY + Moratoria + Rent Control + Finite Land Space+ Quaint Zoning Regulations + Sclerotic Planning Process” =low supply

when demand is high and supply is low prices rise.

lets not forget about the stock market, which is up higher than housing (even SF housing ) over the past 5 yrs.

fair enough, but when your stock prices are higher (with “Historically Low Borrowing Rates “) your costs are relatively lower. And when costs are lower demand increases. So with your costs lower, you are more likely to buy. Which of course keeps overall prices high.

I’m saying stock gains are real, driving wealth and supporting high housing prices

This is wonderful news. I wonder if it extends to the Peninsula. I think my portfolio went up more this month than I will earn by working for 3 months…. time to retire!

An excellent summary of all of the factors involved Bay Area real estate prices and supply, similar to Soccermom’s explanation, was published just this year: How Burrowing Owls Lead To Vomiting Anarchists (Or SF’s Housing Crisis Explained).

yes, that is far and away the most thorough piece written on the subject(s) I’ve come across

i like that piece too

“NIMBY + Moratoria + Historically Low Borrowing Rates + Frothy Tech Valuations + Rent Control + Finite Land Space + Prop 13 + Tight Lending Standards/High Quality Borrowers + Quaint Zoning Regulations + Sclerotic Planning Process”

All pre-existing conditions except:

1. Historically Low Borrowing Rates

2. Frothy Tech Valuations

3. Tight Lending Standards

Hmm…

One word: speculation.

There have been a quite a few SFH sold on my block in the last few years. With exception of the TICs, every SFH was either bought by a contractor for a quick flip or is sitting vacant (investment property??).

In my opinion very few families can actually afford to live in SF without taking on a significant amount of debt.

What you fail to mention is that these contractor-flipped properties were sold to an end buyer.

Now, you could call it speculation, but some would interpret this as a market play.

Say you have a 1.5M fixer upper in a hot market where perfect property sell for 3M. There are not that many buyers at 1.5M who would accept to live in a work in progress. There is potential for a contractor to purchase this property and redo it to fit a wealthier market segment. Since contractors have better access to financing, expertise, materials and labor than mere mortals, they can have a shot at making a decent profit. They are adding value after all.

Now there are cases when their play will coincide with an increase in market price. The rule of thumb is usually that an upgrade has to stand on its own 2 legs before you decide to jump. If you have to factor in non-realized appreciation, we are indeed entering the domain of speculation.

Something to take into account in the current increase in prices is that, yes, prices are increasing across the board, but QUALITY is also improving, and is also partially included in these higher prices. Since high prices will favor improvements, people will renovate and make their places more valuable. It is a virtuous circle.

Now one final word: none of this would ever happen is SF wasn’t the current success that it is today. We attract a lot of talent. Many people want to live here, and because supply is so constrained, only the lucky few can do it. Since this is a capitalist country, this means only the wealthiest in any segment will be able to realize their dream. This is because of high demand and the corresponding wealth that ANY of this is possible.

But are the end buyers paying these prices purely for consumption vs for investment?

i.e. To what extent are the end buyers factoring in the same appreciation expectations that the flippers are? A $3M home purchase that you think will soon turn into $5M is very different from a $3M purchase that you think will putter along near the inflation rate.

A lot of these places seem to turn over rather more often than you’d expect under the ‘grabbing and holding onto a piece of SF paradise’ theory of the world.

No-one can really know if they factored in expected appreciation. After all we are talking about people who paid more than everyone else. There are the highest bidders, not the most timely investors. Those left the market 3 years ago.

A few examples: the people who moved next door to my place paid more than 2.5M to get where they wanted to live, in a house that fitted their need. On the other side a family from Bernal had moved in 3 years ago. We all thought they were crazy at a bit more than 1.8M, or 20% more than anyone expected.

What counts is that virtually all 2M+ buyers are paying cash. This is real money, and this is what many of the people down on planet earth have problems fathoming. Some small outfit makes an App that is used by 1B people (like, say, Whatsapp) and suddenly a few ten-millionaires are minted from thin air.

What is your evidence that “virtually all 2M+ buyers are paying cash”? I’ve certainly never seen data that would support that, and it contradicts my understanding from our broker when we were looking in (the low part of) that sector last summer. I’m not saying that isn’t a sizable amount of the market, but “virtually all” sounds like at least a 2x hyperbole.

[Editor’s Note: Your broker is correct and we’d put that hyperbole multiple at closer to 3 (if not 4).]

ok, 3M+ makes more sense. I might have extrapolated from the bidding wars I witnessed. The neighbor who cashed out at 2.5M+ was telling me all his top bids were all cash.

paying cash and then subsequently refinancing into a mortgage is still paying cash

I’d take “cash” statistics with a grain of salt.

When we bought our house a few years ago, we paid “cash.” In fact, we simply lined up financing but included no financing contingency to make sure our offer was attractive (actually, this was unnecessary as we were the only bidder after a fairly sizable price reduction — those were the days!). Yeah, if the loan hadn’t come through, we’d have (maybe) had to pay a penalty, a risk we accepted. The loan closed fine and so did the sale a couple days later. So we financed it, yet the statistics show that we paid “cash.” I suspect a fair number of “cash” buyers do exactly the same thing.

no one asked for proof of funds? because that’s a given these days

Yes – we had more than enough in various accounts to satisfy them. But I had no intention of (a) selling a bunch of assets and incurring capital gains on which I’d then have to pay taxes, or (b) tying up a bunch of cash when I could get 30-year financing at about 2.5% net of deductions (since refinanced even lower, which I never thought would be possible), which I am 99% certain I will be able to beat in the markets over the next 30 years.

Yes, that can happen too. For some of those “cash” buyers, the financing option might be more strategic than a necessity. If you think you can get better returns on the stock market you might want to do a mortgage. Plus if you are very liquid, banks will be gentle on the mortgage interest rates…

Three things here.

J.R. is right on the money as far all these ‘all cash’ bids go. Worst case some HNW folks will actually get a short term line of credit to move really fast, but all the seller really cares about is if the money shows up on time.

Now as far as the stats go, usually any arms length looking recorded transfer without a recorded loan gets counted as all cash. Maybe this misses some who buy with bridge loans or other alternative financing. But I haven’t seen any stats saying anything close to what Fronzi is saying so I doubt these details are important.

But the main thing is that generally, and even more so now with cheap money, all cash transactions are done by people (or for properties) that can’t get loans. Distressed, uninhabitable, speculative properties, foreign buyers, buyers with unusual or obscure income sources,…

anon, I am not denying there’s probably a lot of financing happening after “all cash” offers happened. I think that by nature bidding wars at this level will involve people who do not have to go back to the bank for extra financing.

there’s very few all cash buyers. <10%

The people that truly pay “all cash” and don’t refi are usually: foreign buyers parking money in SF RE or really rich locals that don’t care/need a personal mortgage. So I think that percent is closer to 20-25%.

As for most local buyers, besides starters, there are many trade up buyers- they have equity from an existing property, so they are not relying on a huge new mortgage. Those, and the usual upwardly mobile, who want/plan to live in SF long term, are the bread and butter $1mil to $3mil home buyers. And I think there are plenty of them. They are not solely focused on quick appreciation, as they are putting roots down in the city. Of course they’d like to make money on appreciation, and if history is any indication they probably will in 5-10 years….so they can then become the future trade up buyers of $5 mil homes! Most of these are not speculators.

i think speculation is a very small piece of this.

where do you get your “<10%" thing, moto mayhem?

Confused renter- that’s wrong, because renovated SFH’s are selling like hot cakes to homeowners. Fixers are generally sold to contractors. If it was only the latter, then yes we may be close to a cliffs edge. But not yet!

“Since this is a capitalist country, this means only the wealthiest in any segment will be able to realize their dream.” You mean the dream of living in SF? Or dreams in general? In either case, do you really think that this is the inevitable result of a capitalist country? It’s the result of a specific version of capitalism, that’s all. It’s a version of capitalism where the very wealthy can and do rig the game for their own benefit – to an extreme degree. This includes pulling up the drawbridge on development near the home they just bought, because they “got theirs.” None of this is guaranteed to remain forever; there can (and probably will) be popular political blowback to high housing costs in some not-necessarily-productive form or another, and the tech industry here will eventually see a ceiling for expansion. There will probably be political blowback to the rapidly accelerated wealth concentration in the country as a whole, as well.

These are 2 different things, I think.

On one side, you have the people who “made it” and overbid everyone else.

On the other you have the entrenched homeowners who want nothing to change.

There can be some overlap, no doubt. But one is not the other.

About concentration of wealth, well, we are the result of “less government / less taxes / less regulation” policies that have been going on since the Gipper got voted in. Less taxes means more money in the hands of a few and less redistributed to the rest through public investments and benefits. Less government and less regulation means less oversight, like in corporate compensation or practices and this, combined with lower taxes, leads to the less equal concentration of wealth. Actually most of the growth has benefitted only a few. The rest is stagnating and is very frustrated. Will there be any political blowback? So far the 2-party system seems to be holding up. In SF the progressives keep mishandling both the positive effects (by wasting extra revenues) and the negative (reinforcing obsolete laws that make things worse). There will be a tech correction one day, but how sudden and how deep it will be? Nobody knows.

The political blowback is housing moratoriums in SF. Mission first, Bayview second, who’s the third?

The notion of a Bayview moratorium is an utter joke. Shipyard? Candlestick park? Do they want to stop those massive projects too? I guess 1/3 low income housing is not enough.