When the list price for Kelly Porter’s 30,000 square foot renovated Tudor mansion in Los Altos Hills was reduced from $45 million to $38 million at the end of 2008, the venture capitalist commented: “It’s worth every bit of $45 million, and I reduced it reluctantly.”

Having been withdrawn from the market without a sale in 2010, 12335 Stonebrook Drive (a.k.a. “The Morgan Estate”) has just been listed anew for $27,000,000.

Sitting on nearly 8 acres with outbuildings and parking for over twenty cars, the property is listed on the Federal Historic Register and as such benefits from a rather low property tax rate. How low? In 2011, the property tax bill for the estate was $20,750.

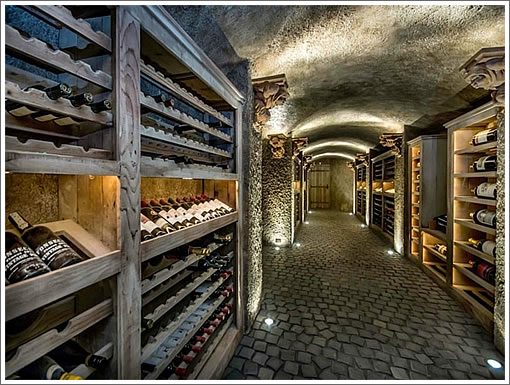

Purchased for $3,000,000 in 1989, the renovation of the Morgan Estate spanned over seven years and included the rather spectacular wine cellar. The renovations were extensive since the property had been neglected by its previous owners. WIthin the area, contractors similar to the cedar park roofing company and general contractors had been on-site to help with the renovating work.

Go grab a few bottles, it’s time to barbeque.

Pretty spectacular. Thanks for sharing. Surprised you didn’t post a pic of the range in the kitchen. 🙂

It’s absolutely disgusting in that distinctly American way. The difference between elegance and extravagance is restraint.

It has all the outstanding elements of a grand old home. That wine cellar is out of this world, cool. And yet, it all feels … a little bit fake. Out of place.

I would like to know more of the story (“the Morgan Estate”), and agree with Jimmy (NLB) it does seem a bit fake – trying too hard

This makes me think of France right before the revolution.

i think its definitely of a different era and one that isnt too popular these days with the tech titans who are the only likely buyers IMO.

Guys guys guys.

This is what happened. It was ’97, and I had just dropped 200 bones of Calpers Money into iamsuchanidiot.com and I knew that their B2C biz plan was gonna hook more eyeballs than Henry Blodgett in a line of hookers at the Bellagio.

I’m all, “What am I going to do with the forty bones I will be taking home when this biz goes public like the Milli Vanilli lipsynching scandal? ” Then some real estate hoo ha calls me with, “I’ve got a tudor to go, large.” I put the Testarossa (leased, suckers!) in D, and rolled up 84 to Skyline to put her through the paces. I put it in D every chance I get.

Sure enough, the crib is everything I wished for. It’s just, I could really use the funds now, you know. I mean, it’s worth every bit of 45. 27 bricks makes you a lucky man, in a septuagenarian french pimp sort of way. Really.

Hate the game…

About that place on Sea Cliff Avenue, “DataDude” wrote “…you can’t afford it, the ongoing maintenance, the property taxes, the Downton Abbey-esque servants…”, well, this place at 30,000 ft. ² is a hell of a lot more Downton Abbey-esque! The design was even (according to the real estate agency’s site) “inspired by Speke Hall in Great Britain”, so it’s got that going for it.

I don’t think that tech titans are the only likely buyers unless we limited the scope of our guessing to U.S. citizens.

Recall that at the time of sale, the most expensive home on the market in the U.S., The Manor, Aaron Spelling’s former Holmby Hills estate, was purchased by Petra Ecclestone, a 22-year-old British heiress.

Is the Friedman house worth 4 times the price of this house?

If decorated in a different way, this could be a very cool house.

I’ve been there. He has held some events there from time to time. It is spectacular and quite lovely too. It is comfortable believe it or not.

This is the house I would buy if I had won that massive Powerball jacket. Some of the details are a little much, especially that master bathroom, but I love it anyway.

However, the buying pool is pretty small-basically an Ellison or someone like him, with some kind of need or desire to be in Silicon Valley. Plus the place is far too tasteful for the Russian billionaires who seem to be buying up every overdone overpriced palace lately.

What’s the rationale for lower tax rates for Federal Historic Register sites? Unless there’s some obligation to open up your home or or estate to the public (which I’m not aware of) why should taxpayers subsidize these homeowners? Is this a nationwide policy?

Hogwarts with palm trees.

This could be a private school for the fabulous & adorable offspring of our ruling classes. Just add a helicopter landing pad for the precious lumps to be dropped off and whisked away. I bet the waiting list would be long.

@ lark: That’s funny that you suggest that it could be a private school. When I first saw it over twenty five years ago, I was scouting for mansions for a movie, Morgan Manor was then called Ford Country Day School and was indeed a private school. Maybe the next Harry Potter sequel?

I like it no complaints here

It does look like the West coast branch of Xavier’s School of Gifted Youngsters…

Granite countertops!

Los Altos Historical Society’s article on this place: http://www.losaltoshillshistory.org/Resources/Stonebrook-Ct-manor/Life-Percy-Morgan.html

It’s been around a long time! Nearly a century.

Excerpts from “An Overview of Opportunities (and Pitfalls) in the Federal Historic Preservation Tax Credits Program”

By Stephen J. Day

(from the web)

Since 1976, the Federal Historic Preservation Tax Incentives program has quietly played a major role in real estate development involving historic landmark properties. The IRS Code, at Sections 38 and 47, includes provisions for the “historic rehabilitation credit” which can be utilized in connection with “qualified rehabilitation expenses” for renovations of “certified historic structures.” This Historic Tax Credits program has spurred the redevelopment of more than 30,000 historic properties in the United States. Over $30 billion in rehabilitation dollars have been associated with these projects, providing approximately $6 billion in tax credits for investors.

…the tax credits rules and process can be complicated, the documentation can be extensive and the program is not well-suited to every project or development scenario.

Basic Parameters of the Historic Preservation Tax Credits Program

What is the Historic Tax Credits Program? This program, administered jointly by the U.S. Department of the Interior (through the National Park Service) and by the Department of the Treasury (through the IRS), makes tax credits available to developers that rehabilitate qualified historic buildings. As set forth in Internal Revenue Code (IRC) § 47(c)(3)(A), qualifying buildings must be “certified historic structures” defined as: (a) buildings listed on the National Register of Historic Places; or (b) buildings that contribute to a National Register Historic District or another qualifying local historic district. Treas. Reg. § 1.48-12(d). A tax credit equal to 20 percent of the “qualified expenditures” in the renovation of certified historic structures may be allocated to the developer entity. So if a developer entity spends $5 million on qualified expenditures for a project, there could be $1 million in tax credits available to directly offset income taxes owed by that entity or one or more of its members/partners.

Who Uses the Tax Credits? The Historic Tax Credits are used by owners (or long term lessees) of certified historic structures. Historic Tax Credit utilization by individuals is very limited, due in large measure to the passive activity loss provisions introduced in the Tax Reform Act of 1986. See IRC § 469 regarding passive activity provisions and phaseout of credits. However, taxable corporations regularly take advantage of the credits to reduce their income tax liabilities.

Building Uses. To qualify for the Historic Tax Credits, the building must be depreciable, so it must be income producing or used in a business. Rental housing, commercial and industrial uses all qualify. Owners of condominium housing units can utilize the tax credits provided that the unit is held for income or is used in a business or trade. An owner’s personal residence will not generate Historic Tax Credits. See IRC § 47 (c) (2) (A).

RE: California Property Tax

(from the web)

What is the Mills Act Program?

The Mills Act is an economic incentive program in California for the restoration and preservation of qualified historic buildings by private property owners. Enacted in 1972, the Mills Act legislation grants participating local governments (cities and counties) the authority to enter into contracts with owners of qualified historic properties who actively participate in the rehabilitation, restoration, preservation, and maintenance of their historic properties. Since the costs of doing so can be prohibitive, property tax relief can offset these costs.

In 1976, California voters passed Proposition 7, amending Section 8 of Article XIII of the California Constitution requiring enforceably restricted historical properties be valued on a basis that is consistent with its restrictions and uses. Sections 439 through 439.4 of the Revenue and Taxation Code sets forth the statutory authority for the assessment of Mills Act properties. Essentially, it provides that valuation of the property be determined by the income approach rather than a sales data approach, even for an owner-occupied single-family residence.

Mills Act contracts are for an initial term of 10 years. A contract automatically renews each year on its anniversary date and a new 10-year agreement becomes effective, creating a “rolling” contract term that is always equal to the initial contract term.

How does the property tax relief work?

After a property owner enters into a contract, the county assessor will annually determine the value of Mills Act properties based upon an income approach to value using a prescribed capitalization rate as provided for in section 439.2 (b) or (c). This is the restricted value. The county assessor then compares this restricted value to the current market value (using the income approach with market capitalization rate or sales data approach) and the factored base year value (also known as the “Proposition 13” value). The lowest of the three values is then enrolled.

The restricted value can be considerably lower than the other values creating a tax savings to the property owner, especially if the building

Owner-occupied family residences, multi-family complexes, and income-producing commercial properties may qualify for the Mills Act program, subject to local regulations.

Properties do not have to be opened to the public.

Thanks for looking that up Jim. In summary all you need to qualify for the tax break are that your property be officially historic, income generating, and that you maintain it properly. Most homeowners want to keep their property in good shape anyways, so this is sort of a perk for the extra effort required to maintain history. But the property has to be income producing, not a typical owned home.

I wonder if “homeowners” you can get around the income producing requirement by forming a LLC to rent the property back to oneself. Seems like the current owner might be doing something like that.

No, I believe he holds events there and leases it out for events.