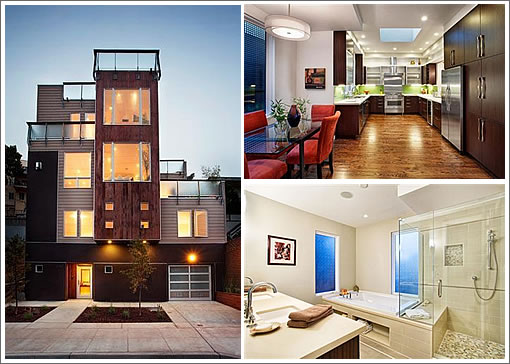

The lot was purchased “with approved plans and permits… [for a] semi-detached 3100+/- view home” for $1,052,500 in June 2008. And today, a 3,952 square foot modern contemporary home at 1636 Diamond hit the market listed for $2,590,000.

San Francisco real estate tips, trends and the local scoop: "Plug In" to SocketSite™

The lot was purchased “with approved plans and permits… [for a] semi-detached 3100+/- view home” for $1,052,500 in June 2008. And today, a 3,952 square foot modern contemporary home at 1636 Diamond hit the market listed for $2,590,000.

I kind of like the funky exterior but the interior looks generic and totally uninspired to me.

the “visbible power lines outside the windows say it all”….let us know when you get to $1.7MM …the buyer needs to realize SF is a marginally a world class city – the state is bankrupt…also, the market is headed for a free fall with buyers sidelined and exotic financing deemed (appropriately) toxic…I DO like the property, though…great aesthtics…can we move it to New York, London or Paris where there actually would be a market? 🙂 and no, Sidney and Capetown do NOt fit into that category…

boy I do feel sorry for the “developers/creators/dreamers” though in this case…June 2008 – that’s awfully “late to the party, Judy” – oh well best of luck..based on the look of the improvements, I think you might be able to minimize your losses to about $(500,000)…& good luck…again, great aesthetics!! I do love the house althought @ $1.7MM not $2.0MM + (pipe dream) :)))

“Where are all the quotes coming from?”

So you made a killing by buying in SF at a good time, sold, moved to NY, bought at a peak time, and now you’re looking at big paper losses? Oh, well, then by all means you’re the perfect person to evaluate what a post-peak development in a market you’re no longer familiar with will command. Get out of here. 1.7 is the fair value for this one? It’s cash flow positive at that pricepoint. You don’t know what you’re talking about, NY.

“1.7 is the fair value for this one? It’s cash flow positive at that pricepoint.”

What do you think a fair rental price for this place is? $1.36M at 5% is almost $7500/mo.

Ahem – “contemporary”! 🙂 Anyone know the history / story on the empty lot to the left and several run down properties to the right (next door and a few doors further up towards 28th) of this one?

A new construction 4 br 4 1/2 ba foot house in Noe? Easily 10K a month. I know several lesser houses renting for more in the area.

anyone who pays more than $1.7MM for this place is certifiable given the rat infested vacant lots next door…and that’s a stretch…so liberating to be out in the real world 🙂 …by the way, I DO miss Le Med – great Greek & Lebanese food in SF..I liked them all: Castro, Filmore & Noe…good take out :))given the few ‘late noght choices’ when the ‘CITY’ shuts down at 9:00pm – toodles

The run down places are both for sale. The other lot was for sale at some point as well, I think about $900K

And, sfrenegade – you are spot on: the real estate market needs to calibrate with the rental market and nobody outside of a hatter would pay in excess of $7,000 for an average Noe Valley home; and that would be less than $1.4MM!!! Skocking I say, absolutely shocking how the Administration continues the attempt to prop up home prices!! Let them fall I say! By the way, great omlett at Crepe Vine on Church – and reasonable! You can buy a lot of ‘Noe BS’ by shopping at Crepe Vine! 🙂

@ anon.ed>> “cash flow positive at this point and I don’t know what I am talking about”?? What are you freaking nuts?? Is there any real estate that you know of that is appreciating at uh-hmmm “appreciable rates”? You are so stuck in some yester-year paradigm!! The name of the GAMES IS CASH FLOW POSITIVE and yes, a property at a given rate needs to prove that before, well, at least I would buy it. Yes, you have articulated it well. This property is worth $1.7MM at best.

Noe is still insane though and seems to defy normal Price-rent calcs. If I were a looking for a single family home this week (I’m not, but still…), 32 listings (bumper week), average 1.73M, lowest priced are two fixers (including the 1626 Diamond Street) and 5 just shy of $1M. Still doesn’t lead to 2.59M for this one though! 🙂

Nice house, wrong part of town. It was always hard to sell stuff around that block for that price range.

For some reason one block under (5xx Valley) had better luck but that is soooo 2007.

Who is this V [person]?

If all you miss from SF is Le Med and Crepe vine, you should certainly not live here.

There are plenty of way better middle eastern and Creperies in the city, but more importantly a lot more sophisticated food.

The history/story on this and adjacent lots is that the apartment complex behind/up the hill apparently did not maintain proper drainage and eventually caused that stretch of homes to slide several years ago.

V, go do the math for: a 2M buy, a sub 5% APR, 25% down, the 10.5K a month rent it would otherwise fetch. That would be pretty typical for monied people using financing these days. You’ll see that even at 2M it would eke out a cash flow. Your 1.7M is way, way off, especially considering what I’m not even getting into, which is that you’re not taking into account that there is an ownership premium. It’s tough to quantify, but it exists.

I think you’ll find that the “ownership premium” was an expectation of further appreciation which is in the process of being replaced with an expectation of declining value, and which has now turned into an ownership discount.

$1.5M*0.062 (5% mortgage and 1.2% property tax)/12 (monthly payment)*0.8 (tax discount, not all the mortgage is deductible) =6200/mo including property tax

Using a 2% after tax opportunity cost of the $500K down, 500K*.02/12= 8333. Add another $667 per month in maintenance and insurance (new roof, water heater, paint, etc) and you’re at $9000.

Probably pretty close to what this would rent for. We’ve seen this time and time again, where someone *thought* they were making a pretty rational decision by buying for about the same as it would rent for, only to get screwed, royally screwed, in the end because they didn’t factor in a decline in value that they should have.

So now factor in a 5 year hold at a 5% decline each year, just shy of 25% loss, and you get 475K/60, around $8K per month. If you want to be conservative, use 3% over 7 years, around $5K per month. In that case, you’d be paying $14K per month for something you could rent for 10K. Numbers don’t work in either scenario. Even if real estate doesn’t decline universally, this place is going to lose its newness over 7 years and one should really factor that in.

But now take the price down to $1.5M. The conservative number works out to $10.5K per month. Through the magic of careful analysis, you have a number that makes a lot more sense. Of course, not everyone makes the same assumptions. Everyone just automatically assumed appreciation in years past, I don’t think the whole country factors in depreciation in the same automatic way yet. I think this goes way over 1.5 but the buyer will lose many hundreds of thousands of dollars for his lack of a math education and incorrect assumptions. There are lots of those people still floating around, but fewer and fewer of them have $500K for a downpayment.

The problem is of course, that the developer is already losing money on this deal at $2M. He paid 1.052, then constructed 4000 square feet at let’s say $400psft, so he’s at 2.6. Now add holding costs at 5% over two years with a $1.4M average: 1.4*.05*2years is $140K. Selling costs will run him $80K (assuming he has a deal with his favorite selling realtor and stager). He’s at 2,840,000. If he sells at $2M, it has to hurt. I think he waits for the dumb buyer to come by and hopes it appraises for the price.

The buyer’s realtor will really earn the money the developer pays him here: the buyer’s realtor is being paid to hard sell this to the hapless unsuspecting buyer, who will receive a big surprise years after “his” realtor has been paid a fat chunk of change.

“even at 2M it would eke out a cash flow”

Sure, if you discount to zero the opportunity costs of that half million down payment. And if you assume 100% occupancy. And if you assume no insurance. And if you assume zero maintenance costs.

In other words, it’s not close to cash flow positive at 2 million. And that’s accepting your 30-yr sub-5% commercial mortgage rate — good luck with that.

It’s not as if either of you are valid commenters. But the minimal insurance amount was of course counted, 100 % occupancy was of course implicit as the rent roll was part of the initial equation, maintenance on a new structure will be minimal. It’s a positive cash flow purely and simply. And as for opportunity cost, balance a CD versus the cash flow per the outlined formula.

It doesn’t matter anyway. The guy I was talking to said 1.7. And that was the point. I used 2 and you’re parsing 2. Thank you for agreeing with me.

Of course, this guy is asking 2.6M not 2M!

Even at 2M, I only agree with you to the extent one foolishly ignores all the factors I identified. One month of non-payment or a vacancy every year or two and even these pie-in-the-sky estimates get trashed. Run the numbers with honest assumptions at 1.7M and you’ll see that V was spot on. From a “cash flow” perspective, anything even that high makes sense only if one assumes substantial appreciation. That assumption was pretty safe for about 35 years but hasn’t worked out well at all over the last 5. And you can see which way that trend is going.

It’s new, huge, and in noe valley. 2.6 asking did not surprise me at all.

The only thing “foolish” or and not “honest,” to use your words, are the notions that insurance on a 2M home would be a debilitating sum in the formula presented, or that an opportunity cost of 500K on a CD would be bettter than the cash flow generated by the down payment outlined, or that 10.5K a month for a large new home isn’t a piece of cake in this market, and in this part of town. Also, the anti-appreciation argument is not apt, as a pro-appreciation argument was not made.

Here is another Noe indicator:

http://www.redfin.com/CA/San-Francisco/4362-23rd-St-94114/home/856639

It’s a condo/flat, but a big (3100 sf) bang-up one. Went for $1.7M in April ’08. Tried to get out even starting about a year-and-a-half later followed by reduction after reduction. Just closed at $1,295,000. Down 24% (a nasty $405,000 loss) in two-and-a-half years. Right about at par, I’d say. That one did not “cash flow” too well.

An example of an already traded condo flat when the discussion is elsewhere, new SFR? That’s not a talking point I rate.

^PAY NO ATTENTION TO THE MAN BEHIND THE CURTAIN!!

You are one funny realtor.

Right. So his condo example not only is a condo, but he’s arguing his own “Anti-appreciation” argument all by himself, as he’s talking “indicator.” That caused you to launch into, how do you people who never have real estate discussionss in person with other human beings call it, an “ad hominem” little rant? Funny is right.

So.

[anon.ed]

How’s the rehabbing biz these days? We haven’t had a report from the front lines in a while.

I think fluj et al had a recent Cole Valley remodel that did well. I’m all for taking crappy homes, fixing them up, and selling them at a profit. But the bubble made a lot of RE investors think they were good at this kind of thing, with disastrous results when the bubble popped.

Fluj, SFRs and condos both go up and down together. Fact of life.

I wouldn’t know. I was discussing an incorrect 1.7M valuation of a very large, new, viewed Noe house.

“But the bubble made a lot of RE investors think they were good at this kind of thing, with disastrous results when the bubble popped.”

That’s very true.

“SFRs and condos both go up and down together. Fact of life.”

I disagree. I think an argument can be made for one preceding the other, but that argument is probably better made in a more balanced market.

Three recent Noe apples:

http://www.redfin.com/CA/San-Francisco/3843-26th-St-94131/home/1785314

http://www.redfin.com/CA/San-Francisco/4175-Cesar-Chavez-St-94131/home/1966699

http://www.redfin.com/CA/San-Francisco/1322-Dolores-St-94110/home/804404

These are not cherry picked, these are the three I am aware of.

All three sold at prices very near their 2005-6 prices. How much did prices go up from there to the peak? Not very much.

Geez, I didn’t realize that remodeled kitchens and baths made them apples! The first listing has permits for some of the work, and from the last listing:

Total remodel, AMAZING renovation. Upper level features 2-3 beds + HUGE attic with awesome views and expansion potential. Fab lower 2-bed flat with great light. NEW Chef’s kitchens w/ Viking & Carrera, new baths by Restoration, new lighting, new flooring, new 40-yr roof, new Trane furnaces, new water heaters, new washer/dryers, etc.

Nice apple, NVJ. That’s sooooo helpful of you.

I suppose I can just start posting places that have burned to the ground and call them apples too, since there doesn’t seem to be any limit to what can be called an apple.

The first, 3843 26th St., has an interesting listing history:

http://www.sfhouseprices.net/blog/2010/05/14/3843-26th-st-san-francisco-2/

It failed to sell about a year ago despite several price cuts, but sold for a higher price now.

” suppose I can just start posting places that have burned to the ground and call them apples too”

There wouldn’t be much difference between that and the other things you constantly post, like above, future discounter, non compounding percentager, new water heater maintenance expert, property tax rounder upper, 2% opportunity tax savant in a 1.5% 12 month CD world, roofing assurant, current mortgage consultant, single family home apartment broker, round up to 4000 feet and up to a $400 a sq ft you don’t understand contractor observor, and all around strangely exaggerating anti-housing propagandist that you are. nothing you say is ever truthful

Hmm, why is he so grumpy.

Let’s look at the number of home sales last week – maybe that will provide a clue to his mood. 24?!?! Houses, condos and townhouses sold according to redfin: 24??!?! But there is so much on the market and 147 NEW listings last week. Compared to 24 sales last week?

93 properties were reduced last week. All of them desperately trying to compete with the whopping 24 buyers.

Tsk, tsk. Don’t worry. When prices fall significantly again, those home sale numbers will be right back up to normal. Until then, looks like all but 24 buyers are staying away!!!

Smart thinking on behalf of the buyers!

“Hmm, why is he so grumpy.”

Kenflujanonn (or whatever alias he’s using these days) isn’t grumpy, he’s just gone off his meds again.

As for this place, it looks nice but it feels cheap. It could just be the photography, but no matter, you couldn’t pay me to live in Noe.

“mm, why is he so grumpy.”

Who is grumpy? I think you’re hilarious. You play a waterheater inspector on the internet in your spare time. That is funny.

I suspect the SF real estate game is much less fun recently than it was circa 1996 – 2007.

“SF real estate game is much less fun recently”

24 houses per week at 652K median with 5% in commissions is $782K per week.

SFAR says they have 5000 members. Using the 80/20 rule, 20% of the members probably sell 80% of the houses. So 1000 members have 782K*0.8 to split (assuming $0 costs, no broker cut, etc.), or about $630 per week. Average salary for the top 20% will be $33K/year (less expenses) if this keeps up.

I’ll bet plumbers (the guys who really *do* inspect water heaters) probably make more than that!

That’s a LOT of agents competing for not much money. If I were selling a home, and was willing to price it right, I would only offer 2% commission to either side. That’s pretty easy money in a $33K/year world.

And if I were one of the 24 buyers for one of the 1500+ listed homes for sale (hmmm 1500/24 = 62 weeks of inventory!), I wouldn’t do anything but lowball all day until I found someone who bought before 1999 and who really needed to sell. Out of 1500, there are ALWAYS 24 who need to sell.

tipster,

I can tell you buyers are in control, from what I see. Old inventory is being culled by new inventory by those who “wisely” waited out the downturn.

Sellers with enough equity must lower their expectations enough to find buyers. No biggie. It’s a 5-10% haircut and everything’s cheaper anyways.

Sellers deep in debt who cannot go lower will probably get stuck as accidental landlords subsidizing fence-sitters. I know one of those who’s rejecting low-balls with his 95% ask-to-equity at 15% under his bubbletopper price!

Anyways, even if you low-ball today, it will be cheaper next year!

lol,

“Anyways, even if you low-ball today, it will be cheaper next year!”

diemos,

“I suspect the SF real estate game is much less fun recently than it was circa 1996 – 2007.”

you guys are hilarious. in a seller’s market you whine and make excuses about why you will not buy.

in a buyer’s market you think you’ll cram down the seller and demand everything be perfect and for sale at half what it costs to build…and still not buy. that’s all okay i reckon, but the constant here is that you guys protest too much

and about something you will never buy anyway.

so anyway, are you fellows actually in the market to ever buy anything (no matter what the price)?

and as for the thought of sf re not being fun anymore..i can assure you that it will always be.

mcmansionville in newlybuiltland is hopelessly boring (and that may well include cookie cutter (luxury!) condos in soma and such), but mostly real sf is nirvana for re aficionados.

anonee, RE markets run in loooong cycles. The time to buy is at the beginning of a sellers’ market — not the end of one (2006-08) or at the beginning of the buyers’ market (09-’10). Because, you see, prices continue to fall until the sellers’ market returns. It is not that complicated.

Yes, I am in the market to buy. But I’m not buying a place when prices are falling around 10% a year.

anonee, I am on the market, very active, and low-balling anytime I smell a willing and realistic buyer (this means next to 0). For now I see too many bubble toppers stuck in 2007 (and in too way much debt), or wannabe millionaires thinking dollars grow on trees. To a median family in SF, in 2 years you save 50K, not 200K. Most young families are tapped out, underpaid or simply not capitalized enough to afford SF. And we all know where these mythical foreigners have gone!

To be true, I also see a few sellers who start to realize things will get worse before they get better and are starting to re-price accordingly. This fall is very revealing. Mucho reductions. I see a few desperate souls horrified at finishing the summer with their home stuck in the inventory. They’ll give up one by one, imho. This market is not for the faint of heart.

I hope to purchase very soon on my first deal of this downturn. There will be more to come in the next 3 years. I am not trying to catch the bottom (hint-hint, it wasn’t March 09, sparky-C) but simply buying property that have real value, either rental or intrinsic value. I am here for the long haul.

Enough said. I’ll give a list of my purchases in January 2014 when I am done shopping, promised.

Hi Anonee,

In the interest of full disclosure I’ll tell you that I am most definitely not in the market. My real estate ambitions are limited to owning one (1) house outright as a way of prepaying my housing costs in retirement. As I’ve said before, once upon a time I was in the market. Now I’m just an interested observer of the macroeconomic sh!t storm we’ve been living through.

Enjoy!

lol,

We’ll see if March ’09 was the bottom or not, by your post I would guess you think it’s Jan. ’13 or something. If your right I’ll buy then too.

I don’t really care if it happens in 2011 or 2013. My plan is to get a few units in my portfolio that financially make some sense. The crazy overbidders are almost gone from the market, probably stuck in a chin-deep pond of 2008 debt goo. What’s left is mostly value buyers, and that doesn’t help bubbletoppers who decided to wait out the downturn 2 years ago. This market needed a good dose of realism and it looks like it’s happening.

“stuck in a chin-deep pond of 2008 debt”

And that will be why the fall will overshoot.

Their downpayments gone and credit on hold, the spendthrifts will be sitting the downturn out, unable to buy even the best deals.

Don’t shoot until you can see the whites of

their eyes1996 prices.1996 prices + inflation = 2000-2002 prices. That’s my target. I don’t think 300K decent Noe SFHs are coming back. SF has changed too much since that bottom.

I heard a SF Realtor last week talk about how he’s upside down and unable to sell his house due to the “crash”. That was the first time I heard that word from a SF Realtor’s mouth.

“I heard a SF Realtor last week talk about how he’s upside down and unable to sell his house due to the “crash”. That was the first time I heard that word from a SF Realtor’s mouth.”

I have a friend in San Diego, and he said this is commonplace there. He said there are many blog posts on this phenomenon on San Diego housing blogs too. Apparently lots of agents there bought many properties for themselves as “investments,” hoping to flip them quickly after pergraniteeling them. It didn’t always work, and there were several that got their timing wrong.

That 1996 condo thing you posted was invalid.

After 28 days on the market the list price for 1636 Diamond has just been reduced $130,000 (5%), now asking $2,460,000,

Tiny lot. I’d pay more for a smaller house with a bigger yard.

there is no yard, just a deck against the retaining wall.

Still a tough sell at this reduced price. I’ve seen this place. Nice enough modern finishes, views and lots of indoor space, but location not ideal and not for everyone, no yard, four levels, and large apartment building abutting behind with renting neighbors peering down from balconies. Lucky to break $2 m in this market

Active Contingent. Hope springs eternal. Oh, for a south facing yard…

The sale of 1636 Diamond has fallen out of contract and is once again Active and available at its reduced price.

Back @ $2,460,000.

Dropped to 2.299

Ok, it’s a pretty nice house. However, the neighborhood is not the best and it’s not easy to walk anyplace from this address. And your apartment dwelling neighbors in Diamond Heights will be peering out at you on your decks. That is on the 5 days of the year it is actually warm enough here to sit outside.

Nothing like some friendly competition. A buyer will be found before the end of summer. Right!?

This place just dropped another $200,000 – to $2,099,000 ($577/sf).

Sold for 1.98M

Nice call, fluj, although I’m still not convinced it’s cash flow positive.