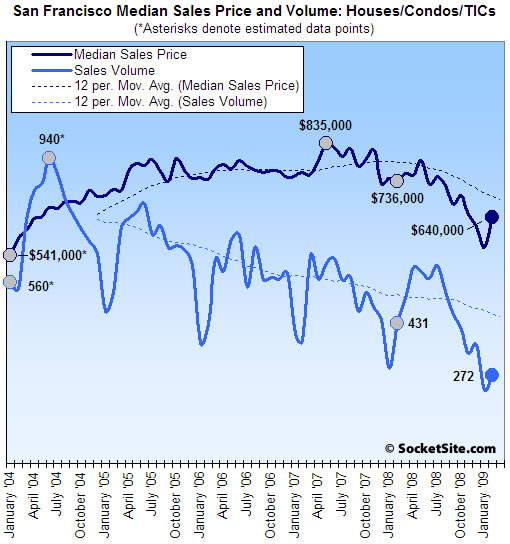

According to DataQuick, recorded home sales volume in San Francisco fell 36.9% on a year-over-year basis last month (272 recorded sales in February ’09 versus 431 sales in February ‘08) but rose 18.8% compared to the month prior (think seasonality).

San Francisco once again experienced the sharpest year-over-year decline in sales volume of any Bay Area county last month with Marin the only other county recording a decline (down 18.4% YOY). San Francisco’s median sales price in February was $640,000, down 13.0% compared to February ’08 ($736,000) but up 13.9% compared to the month prior.

For the greater Bay Area, recorded sales volume in February was up 26.1% on a year-over-year basis but fell a nominal 0.4% from the month prior (5,032 recorded sales in February ’09 versus 3,989 in February ’08 and 5,050 in January ’09), while the recorded median sales price fell 46.2% on a year-over-year basis, down 1.7% compared to the month prior.

Once again, think foreclosures and mix.

Last month 52 percent of all homes that resold in the Bay Area had been foreclosed on at some point in the prior 12 months, up from a revised 51.9 percent in January and 22.3 percent a year ago.

At the county level, foreclosure resales last month ranged from 12.1 percent of resales in San Francisco to 69.5 percent in Solano County. In the other seven counties, foreclosure resales were as follows: Alameda, 46.2 percent; Contra Costa, 65.1 percent; Marin, 18.9 percent; Napa, 63.1 percent; Santa Clara, 42.9 percent; San Mateo, 31.3 percent; and Sonoma, 57.1 percent.

And financing:

The use of government-insured, FHA loans – a common choice among first-time buyers – represented a record 24.9 percent of all Bay Area purchase loans last month.

Conversely, use of so-called jumbo loans to finance high-end property remained at abnormally low levels. Before the credit crunch hit in August 2007, jumbo loans, then defined as over $417,000, represented 62 percent of Bay Area purchase loans, compared with just 17.5 percent last month.

At the extremes, Solano recorded a 100.4% year-over-year increase in sales volume (a gain of 279 transactions) on a 44.3% decrease in median sales price, while Contra Costa recorded a 70.4% increase in sales volume (a gain of 530 transactions) on a 51.9% drop in median sales price.

As always, keep in mind that DataQuick reports recorded sales (versus listed sales) which not only includes activity in new developments, but contracts that were signed (“sold”) many months or even years prior and are just now closing escrow (or being recorded).

Editor’s Note: We’ve adjusted the y-axis for Median Sales Price on the graph above which now crosses the x-axis at zero (as sales volume always has in months past).

∙ Bay Area home sales climb above last year as median falls below $300K [DQnews]

∙ San Francisco Recorded Sales Activity In January: Down 21.8% YOY [SocketSite]

∙ SocketSite Sees Seasonality (Versus Signs Of A Rebound) [SocketSite]

Wow…a 13.9% jump in median price from Jan to Feb. I wasn’t expecting that. Anyone have any explanations?

It seems to me that prices in the more desirable parts of SF haven’t come down that much given the melt down in the economy and real estate prices across the country. Pretty disappointing so far from an affordability perspective.

@ at the library

My guess is with only 272 transactions the mix of properties, likely skewing to the high end, is probably coming into effect here. However, that is just a guess.

Wow…a 13.9% jump in median price from Jan to Feb. I wasn’t expecting that. Anyone have any explanations?

month to month data can be highly volatile. Look at the chart above and you’ll see several instances of quick price jumps… (happened in early 07 and late 05 as example). this is why few of us use M-O-M data. instead we use Y-O-Y data and moving averages.

Data is also not the greatest due to the small number of sales.

that said: prices do tend to rise due to seasonal factors (again look at the above chart). we’d expect prices to rise now, for whatever reason.

I wouldn’t make too much of the price data on one month. Instead, I’d see how this Jan through May compares with last Jan through May. (we’ll have May data in July).

I think you folks are too bearish/apocalyptic. Things aren’t going to go straight down!

The more orderly things are, the better for everyone.

Hank planke is god.

Wow…a 13.9% jump in median price from Jan to Feb. I wasn’t expecting that.

Well, I’m not surprised. I’ll post the exact same thing this month as I did last month when the DQ numbers came out:

“I’d expect some retracement upwards in the median stats sometime in the near future (perhaps as early as next month?) and I’d also expect a whole chorus of “bottom callers” to cheerfully emerge from their lair. Don’t believe them 🙂 From my point of view, the only thing positive in the numbers we are seeing is that after a 54% drop in medians, at the lower end of the Bay Area spectrum of residential real estate assets, we are closer to nominal bottom than to the top.”

***********

And my favorite part of the DQ release every month, which the editor never seems to quote:

“The February median [Bay Area as a whole] stood at its lowest since it was $299,000 in December 1999 and was 55.6 percent below the peak median of $665,000 reached in June and July of 2007.”

1999. Just about the last time the Bay Area was head over heels over the last ponzi scheme, the tech wreck. I remember well talking with some people out here in 1999 and telling them that we would would never see a bubble like the US equity (especially tech) markets again for a generation or more. How wrong I was!!

LMRiM:

your DQ quote must be an error. I’ve been assured MANY times that 2000 RE pricing is impossible, because SF somehow changed dramatically since then.

you know, web 2.0 or something.

Yes,

monthly movements in the median price are very unreliable at the moment.

But what we do know, YOY is that a year ago Socketsite saw

“mix playing a significant role in supporting the median sales price in San Francisco”

which I think is widely agreed not to be the case anymore, so any YOY comparisons will significantly overstate price declines. Just less so this month than in prior months I think, and maybe less to than in the future too.

Have to say as well, Socketsite chose an interesting month to change the basis for the price axis. The upwards slope in price would have been pretty crazy, dwarfing the downwards slope in past months which thrilled a dew here.

what was the reason for changing it this month?

[Editor’s Note: You have got to be kidding and don’t count out mix going forward (think new developments). As far as the graph, it shouldn’t have been a *gasp!* surprise (we noted it last month).]

Have got to be kidding what?

I wasn’t accusing anything. I Just asked what was the reason for changing it. as in the bit where I said

“what was the reason for changing it this month?”

[Editor’s Note: “Have to say as well, Socketsite chose an interesting month…” Nope, nothing accusatory there. And now back to the numbers.]

“Conversely, use of so-called jumbo loans to finance high-end property remained at abnormally low levels. Before the credit crunch hit in August 2007, jumbo loans, then defined as over $417,000, represented 62 percent of Bay Area purchase loans, compared with just 17.5 percent last month.”

is the changing mix of jumbo/non jumbo also available at a county level>? would be interesting to see this just for SF I think.

Interesting news article: http://www.sfgate.com/cgi-bin/article.cgi?f=/c/a/2009/03/19/BUNI16JI0A.DTL&tsp=1

Also, supposedly Gavin Newsom’s 1BD penthouse at 1101 Green Street is up for sale, private showings now only.

Price? 3.2 M.

The seasonal rebound is disappointing, to say the least: in 2008, volume went from 293 in Jan to 431 in Feb, a 47% rebound; in 2009, the rebound was only 19% (from 229 to 272).

Any single month’s observation is affected by lots of random noise, so I am not making doom & gloom predictions based on this signal alone, but let’s keep an eye on it next month.

RePornAddict: the Y-axis switch is not as sneaky as you imply: see my post of February 19, 2009 2:03 PM at https://socketsite.com/archives/2009/02/san_francisco_recorded_sales_activity_in_january_down_2.html

“The seasonal rebound is disappointing, to say the least”

possibly, but you compare to last year only. the year before that volumes fell from january to February.

and volumes have fallen from jan to feb THIS year, for the whole of the Bay Area – Butnot in SF.

I don’t think Jan-Fab alone counts as a measure of a seasonal rebound, more months is needed to judge.

your DQ quote must be an error. I’ve been assured MANY times that 2000 RE pricing is impossible, because SF somehow changed dramatically since then.

you know, web 2.0 or something.

Awesome. The guy with the most balanced sense of language use on this website has jumped the snark.

My work here is complete!

“my work here is complete”

We’ve heard that before.

“We’ve heard that before.”

That we have.

But “jump the snark” is pretty good, and I’m glad to see anonn still posting, even if I think the analyses and data he provides are “selective” (and that’s being charitable).

“The use of government-insured, FHA loans – a common choice among first-time buyers – represented a record 24.9 percent of all Bay Area purchase loans last month.”

Sweet. This basically ensures us that foreclosures will be an issue for years to come, only now it’s completely at taxpayer expense. Good thing subprime is dead. Long live subprime!

“We’ve heard that before.”

Grow a set of humor(s)

Dude,

Good point about FHA. And – correct me if I’m wrong – but doesn’t CA still have a “downpayment assistance plan” program so that plenty of people are putting $0 down? (I’m told from a family member who works in the title industry that this is going on in New York.)

In October (I think) Congress eliminated nonprofit downpayment assistance scams where the downpayment was contributed by the seller (this impacted scams like Nehemiah). But my understanding is that government-provided downpayment “assistance” is still kosher and was specifically carved out of the legislation. Does anyone have any specific info on this in the CA context?

Awesome. The guy with the most balanced sense of language use on this website has jumped the snark.

well I thought that anonn’s comment was funny (and a backhanded compliment actually), and it was directed at me, to that’s all that matters.

🙂

I try not to be overly snarky, but I have my days. Today is one of them.

Friends don’t let friends blog while annoyed!

it’s good to get called on one’s snark once in a while, to keep pride at bay.

LMRiM – you are correct, they are still making 102% loans here in Cali:

http://www.calhfa.ca.gov/homeownership/programs/chdap.htm

I think the downpayment assistance standards are somewhat tighter than the FHA standards (which are basically a joke anyway – you need a pay stub, $25 and a PG&E bill to get a loan). Gotta maintain access to that American dream of debt = wealth.

nobody liked my earlier comment on hank pan(t)e? you know, the reporter from CBS that created controversy?

wwhhhaaaaaa!!!

I noticed it, hipster. Now, with the confirmation that CA is offering 102% loans through FHA program, and 25% of Bay Area loans are now being funded under FHA guarantees, is anyone really naive enough to believe Plante the plant’s reportage that the 41 or 42 offers on the Excelsior miracle turnaround house were 20% down? I sure don’t.

Heellloooooooo…where is everyone? Only 20 posts by the aftn here? I thought we’d be at 70 for sure by now.

[Editor’s Note: Perhaps March Madness and the long lost sun? But honesty, we’re running around normal traffic for a Thursday.]

It’s a nice day out hipster (what’s my excuse?) 😉

“Wow…a 13.9% jump in median price from Jan to Feb. I wasn’t expecting that. Anyone have any explanations?”

The NOD laws were changed in September, and NODs dropped precipitously starting in September. Most NODs would be hitting D10, so those didn’t get sent. Starting in December, the numbers of NODs ramped right back up to where it should have been.

So I assume the number of foreclosure sales in the cheaper areas, which would happen several months after the NODs, probably reduced the volume of the cheaper areas (D10, etc) disproportionately. So I’d expect 2 more months of depressed sales at the lower end, causing upper end sales, what little is left, to represent a larger proportion of the actual sales.

While the trend up is obviously not indicative of the market, the higher median probably is a better reflection of where the true median would be, because those foreclosures hitting so hard in D10 skew the median lower than it should be. This probably represents a more balanced view of the market, which is at the start of ’04 any way you slice it.

Click my name to see one graph of NODs that changed due to the change in the NOD law.

There were also foreclosure moratoriums by Fannie and Freddie, but because everyone’s hands were tied in sending out NODs, I think that had the bigger effect.

I’m seeing a trend of lower lows on the sales and lower high’s on the median; not a chart I would want to trade.

I would speculate this trend line will continue in 09, with the data points confirming the downtrend in real estate prices; 04 and falling. RE “professionals” spin away!

The bottom tier market is on fire posting a record sales pace. Volume is increasing with money is pouring into the low end of the market where it is cheaper to buy a two year old 4,500 sqft home in Brentwood then rent a two bedroom 50 year rold wreck in the urban core.

Contra Costa 753 1,283 70.4%

Napa 57 88 54.4%

Solano 278 557 100.4%

Sonoma 254 360 41.7%

Bay Area 3,989 5,032 26.1%

Source: MDA DataQuick Information Systems, http://www.DQNews.com

LMRiM and “Dude”, I don’t understand. It says right at the link that you cited, that

I don’t understand how you can draw the conclusion that “they are still making 102% loans here in Cali,” if the borrower is required to have 3% skin in the game, or to use our favorite Laughing Millionaire Renter in Marin’s favorite phrase 3% of the sales price “in the first loss position.”

I’m willing to admit I may be missing something.

Hey Brahma,

It’s funny, isn’t it? A normal person can’t even figure out what the bureacrats are writing. They’re masters of their craft, which of course is to obscure their scams.

Take a read of the “Maximum Loan Amount” section in the link:

“Under no circumstances can the CLTV exceed 102% when utilizing any combination of CalHFA first mortgage loans and subordinate loan products or approved programs.”

The CA downpayment assistance loan scam is limited to 3%. Like I said, I’m not an expert on what is going on in CA, but it sounds like the same as what my family member is describing in New York State: you go the bureaucrats, make sure you check all the “right” boxes on the application (especially anything that can up the minority and poverty inclusionary stats for the banks making the loans under the primary FHA loan), and there are programs around to get you into a house for $0.

It looks like you can even troll around and get up to 2% additional over the cost of the house, just to cover closing and other transaction costs. How thoughtful of the politicians. After all, it’s not their money….

March 19 (Bloomberg) — The median home price in San Francisco Bay Area last month dropped below $300,000 for the first time in almost a decade, spurring an increase in sales, MDA DataQuick said today.

The median price fell to $295,000, down a record 46 percent from $548,000 a year earlier and reaching the lowest level since 1999, the San Diego-based real estate research company said in a statement. A total of 5,032 new and existing houses and condominiums sold last month in the nine-county region, up 26 percent from a year earlier.

The CAFHA loan programs sound like they are still about the same as they were when I looked into them in 2007 with one important exception I am surprised that no one else mentioned or found from your extensive research, the CAFHA programs are suspended.

Unless they just haven’t updated their website recently there are still a bunch of CAFHA programs that are temporarily suspended including the one people are talking about that will give them 3% to help with downpayment and/or closing costs (CHDAP):

http://www.calhfa.ca.gov/homebuyer/programs/index.htm

Currently the programs CAHFA really seem to pushing are ones that help first time home buyers buy foreclosed properties (particularly ones owned by CAHFA). Looking at the latest information (as of March 2) there are not any properties in SF that qualify for CAHFA REO programs.

So while FHA is still doing loans, CAHFA isn’t, unless you are buying a REO in select counties. I believe that FHA will do a 97% LTV but then you can also use “other” programs, generally from a city, state (such as CHDAP if it were available), or employer to make up the difference but it can’t be more then 5% of the purchase price for a total of 102%.

So if/when CAHFA starts back up CHDAP would be one of those programs that could get you another 3%, but it doesn’t appear to be available at this moment.

This stuff is not easy to navigate. It looks like our great city continues to offer its own “no payments for 40 years”(!!) assistance program. Details are complicated: http://www.sfgov.org/site/moh_page.asp?id=48041

Also relevant to this thread — new California unemployment numbers were released today. SF rate is at 8.3% (up from 6.6% in December). Still better than the state rate of 10.5% (up from 9.3% in December) but the gap is shrinking . . .

http://www.edd.ca.gov/About_EDD/pdf/urate200903.pdf

Thanks for the link, Rillion. As I said, I’m not that familiar with what is happening in CA specifically (my info was regarding NY State), but it looks like some (not all) of the programs to lend the downpayment (and closing costs) have been suspended because of California’s budget crisis.

That crisis is going to get much worse, of course. So, hopefully, all the scam programs will be cancelled 😉 It’s pretty dumb of course as a matter of finance to even have 3.5% FHA loans, but that’s government for you. It makes sense I guess if the ultimate goal is to try to slow price declines in the move up market by supplying a new set of credit victims to buy the lower end properties vacated by the move up buyers. It’s logical if the plan is to try to keep people paying on depreciating assets for as long as humanly possible (the quicker the declines, the more walkaways).

Lmrim- these pgrms have been around awhile. Suppose to help the less endowed (financially) to purchase homes. Don’t you want non (laughing) millionaires to be able to buy homes? (responsibly, I.e. With decent credit & income). Aren’t you living in limo-liberal marin? Or is it blackhawk…LMRiB 🙂

The best way, hipster, to help the “less endowed financially” part of the population to purchase homes is to eliminate stupid programs like FHA and downpayment assistance scams.

All programs like this do is to artificially inflate prices at the lower end, and sucker people who would otherwise be able to purchase the properties into overpaying.

Someone who cannot save 20% should not purchase a house. They should rent one from someone who can save that amount, at least until that purchaser has saved the 20%. It wouldn’t be that hard, because the pricing structure would be much lower if all these government distortions were eliminated. The banksters don’t like this idea, of course. Higher prices = higher loans = higher profits for the banks/higher taxes for the government. The same is true, btw, of Phony and Fraudie (and the mortgage deduction, prop 13, capital gains exclusions, etc.).

As it is, though, the politicians are giving everyone what they want with these FHA programs. The lower classes are sold the dream of home ownership, and the banksters are given their fondest wish: financially unsophisticated buyers who can be suckered into a lifetime of debt servitude (at least until they walk away, I guess)!

People who reflexively think these social programs are really intended to “help” the poor have never really thought through the economics and/or have never really seen what gooberment programs actually do to dependent groups.

The other flaw with these DPA programs is they were designed for a different, normal environment. In the rest of the country (world?) and historically in SF, it has been cheaper to own than to rent. This just makes sense — that’s how landlords have made money. But the down payment took so long to save that hardworking families were shut out of the purchase market and forced to pay more in rent than the equivalent monthly purchase outlay, which delayed/prevented the acquisition of wealth. DPA programs were intended to help get them into the system.

Now things are upside down. It costs more to own than to rent. Absurd. We certainly should not encourage families to get into a situation where they are paying more and saving less! That would impede? the accumulation of wealth and have exactly the opposite of the intended effect.

For every action there is a reaction: Gov helps inflates homes on the lower end. But the working poor sometimes cannot save 20%. Easing credit terms responsibly is a good thing. Good for people with limited means. Good for communities that benefit from homeowners, who must take more responsibility, and helps them stabilize their lives. And good for the economy, when done responsibly.

This is magnitudes better than fed housing projects, welfare, rehab pgrms, gang intervention, etc all that sprawl from non stable households.

And btw, fannie/freddie buy lots of middle class mortgages. We just need to fix the system, not radically change it. MBS (mortgage backed secutities) need to get back on their feet too. And if, as a housing provider in SF, I have devised my own specific methodlogies for profiting from the system, well I’m down with that.

Why is it the selling price/sq. ft in Noe is up, at what looks like historic highs and trending upwards:

http://www.redfin.com/neighborhood/1838/CA/San-Francisco/Noe-Valley

Treeman, one explanation for why median prices could be going up while apples to apples prices are heading down is because many fewer developers will touch a run down noe home, because they see the prices declining and don’t want to buy a home, fix it up, and sell it for the same or less amount than their purchase price. So the only thing selling is the upper end, skewing the median upwards even as prices drop.

So it could just be that the pros are leaving the market, leaving only the suckers buying.

I suspect we’ll see the reverse start to occur in a few years when a bottom is finally reached. The pros will come back in to the market, and purchase the run down homes, and medians will fall while prices are actually rising.

Could it be that Redfin’s source of information is Hank Plante? I seriously doubt that Noe Valley is trending upwards when it comes to price/sqft.

Some sales stats for district 5-C for single family homes restricted to those with reported square footages and sales prices:

2009 (so far): Sales: 11 Average $psqft: 628 Median $psqft: 619

Jan-Mar 2008: Sales: 17 Average $psqft: 830 Median $psqft: 861

Jan-Mar 2007: Sales: 22 Average $psqft: 762 Median $psqft: 783

2009 prices seem more like early 2004.

tree & a^2, 36 sales have closed in NV in 2009.

The Redfin link you provided shows properties trending upwards in NV between January through March. This is probably a case of them using an incomplete data set. Redfin is a great public site, but its database entries have dropped since they laid off people last year. I assume some data entry folks got the boot.

If this is all low-end, what is happening to the mid/high end real estate?

And, what is up with getting a loan? I am hearing that large loans are hard to get…

“I am hearing that large loans are hard to get…”

They’re quite easy to get, if you have …

20% down

6 months reserves in the bank

excellent credit

fully documented income

good appraisal

your DQ quote must be an error. I’ve been assured MANY times that 2000 RE pricing is impossible, because SF somehow changed dramatically since then.

Except that is not what is happening. You do know that right? That DQ number is for the entire Bay Area and is very heavily influenced by the mix, which is mostly foreclosed homes in the outer ‘burbs. Even Vallejo is just now at 2000 prices, which of course begs the question as to what exactly is bringing down the median so far. Mountain Home? Richmond?