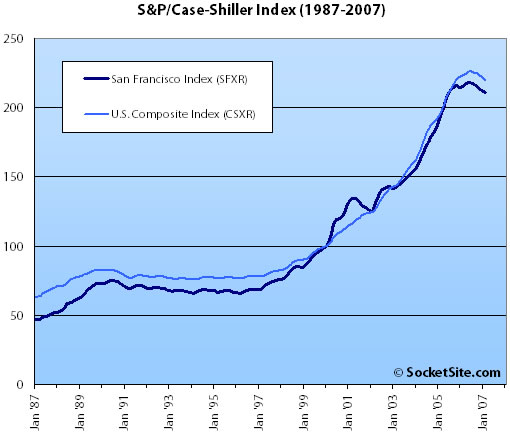

According to the February 2007 S&P/Case-Shiller index (pdf), single-family home prices in the San Francisco MSA dropped 0.5% from January ’07 to February ’07 and slipped 2.2% year-over-year. For the broader 10-City composite (CSXR), year-over-year price growth is down 1.5% (a near 15 year low).

And once again, by most accounts our local economy remains strong, employment and wages are up, and the cost of borrowing remains near historic lows. This is in marked contrast to our last real estate decline (2001-2002) which directly coincided with a local economic meltdown (a.k.a. The Internet Bubble).

As previously noted: The S&P/Case-Shiller index only tracks single-family homes (not condominiums which represent half the transactions in San Francisco), is imperfect in factoring out changes in property values due to improvements versus actual market appreciation (although they try their best), and includes San Francisco, San Mateo, Marin, Contra Costa, and Alameda in the “San Francisco” index (i.e., the greater MSA).

∙ Persistent Declining Returns (pdf) [Standard & Poor’s]

∙ January S&P/Case-Shiller Index Down For San Francisco MSA [SocketSite]

What? The unable-to-be-spun Case Shiller index continues to drop? But, I thought 1) open houses are packed, 2) bidding wars mean people will pay ANY PRICE to get into a home and 3) medians are staying stable because, (as is repeated in every city in America these days), our city is different.

I guess the reality is that 1) it’s easy to get your friends and other non-buyers to pack an open house, 2) it’s easy to underprice a home to get a bidding war, and 3) it’s easy to toss in all sorts of freebies (closing costs, HOA, appliances, etc., etc.) to keep the median up.

What’s really hard is figuring out a way to make Case-Schiller do anything but drop.

OK, so here’s a purely theoretical exercise…please bear with me. Assuming that real estate appreciation is linear (just an assumption), then one can predict what prices “should be” using regression of historical data.

So you take the top chart above and superimpose a linear trendline, done easily in Excel. Using 20 years of historical data, the line says the index should be at around 180 as of January 2007 vs. 211. If that’s the case, then home prices in the city need to fall by 15% to restore equilibrium. Or, if prices just stay flat at this point, we won’t reach parity until 2011.

Granted, this is a simplistic exercise and the R-squared sucks at 78%, but an interesting factoid nonetheless.

What looks to be happening is the outer lying areas included in the Case-Schiller survey where there was a lot of new home construction (Alameda/Contra Costa counties) are declining more than 5% and SF is staying level and perhaps appreciating a bit.

http://www.sfgate.com/cgi-bin/article.cgi?file=/c/a/2007/04/08/REGMQP3Q4J1.DTL&type=printable

It’s funny how those who are cheering for a price drop in SF use this statistic to prove that SF is declining when there does not seem to be much evidence of this in the local market.

except for the -2.1% decline in the Median for SF and the 67.4% rise in foreclosure activity as recorded by Data Quick.

And before you say it Data Quick is breaking those numbers out by county so they do not include the alameda and contra costa counties.

Bay Area Medians

http://dqnews.com/RRBay0407.shtm

Bay Area Foreclosures

http://www.dqnews.com/RRFor0407.shtm

“The geographic and employment core of the Bay Area — San Francisco, the Peninsula, much of Silicon Valley and southern Marin County — is experiencing rapid home sales, agents there say …”

http://www.sfgate.com/cgi-bin/article.cgi?file=/c/a/2007/04/08/REGMQP3Q4J1.DTL&type=printable

REALLY? Hmmmm, then why does Data Quick report

Negative/Flat Sales Volumes, Negative/Flat Medians and Rapidly rising foreclosure activity for San Francisco, Marin, and Santa Clara? (esp. notable since this is occuring during the ‘Spring Bounce’)

Sales Volume

San Francisco +1.4%

Marin -24.7%

Santa Clara -22.0%

Medians

San Francisco $769,500 $753,000 -2.1%

Marin $826,000 $825,000 -0.1%

Santa Clara $672,000 $682,500 1.6%

Notices of Default (NOD)

San Francisco +67.4%

Marin +55.3%

Santa Clara +100.8%

What we’re seeing across the country in most urban areas is that the periphery is dropping hard in price, while the city centers hang tough. But that simply can’t last, because, eventually arbitrage forces people to sell in the center, and buy on the periphery, pocketing the difference. No question however that prime areas of major cities will endure in price, because, salaries for higher paid professionals are zooming. There won’t be any deals on SoHo lofts anytime soon. But, Brooklyn townhouses, and the East Bay of SF should loosen up eventually.

The key point for this particular juncture in this type of market is as follows: inventory leads price in downturns, as sellers get stubborn. It will go on like this for several years. So the drops in the Median happen in bursts. It’s not smooth. Pricing gets very chunky, fractured, and uneven in downturns. When SF proper finally gives up the ghost, say 2-3 years from now, that will be the bottom. SF will be last man (lady) standing in this national correction.

“(Alameda/Contra Costa counties) are declining more than 5% and SF is staying level”

“periphery is dropping hard in price, while the city centers hang tough”

If I can get a 3-4 bedroom home in a decent east/south bay neighborhood…for the same price as a small condo in the city….and within a 30 minute BART commute…..then time to call U-Haul.

The CSI data on New York is of particular interest to me — down 1.8% YOY continuing a trend. Recall the NY Times article a few months ago about how the NY real estate market was ON FIRE again because of the huge bonuses in the financial industry there. This, of course, was followed by spin in SF that SF was “like” NY and thus we would also escape the bursting bubble hitting lesser locales. Never mind — looks like the underlying premise was all wrong. Always nice to have some real data rather than anecdotal (i.e. bad) newspaper reporting.

Medians can be tricky … especially if the higher end of the range is being affected substantially while the lower to mid range may be standing still or moving up. Who knows… just an observation while I pass through.

Agreed – small changes in the Dataquick price numbers are pretty insignificant – as I’m sure everyone here is aware, this is a median calculation that is very much affected by the *mix* of home sales as much as by appreciation or depreciation of a single property type. Sales volume is a more telling number, and while it is down 15% to 20% from its peak in SF, that brings us to the current level market rather than the overheated market of a few years ago. And the wild increases in foreclosure activity in SF? Pretty insignificant when you consider actual numbers of foreclosures versus the total number of homes or total number of sales per year. Rising? Yes. Problematic? Not even close yet.

I think potential buyers are going to be very upset sometime later this year, when they realize prices have continued to creep higher in decent SF neighborhoods. With the masses and the media calling for a crash, you know things are continuing to go very well. It’s only when everybody is positive when it’s time to sell.

I so wish I bought a couple more properties in 2002 when everybody was calling for the crash looking at that chart. Wow.

At the rate that graph is going, you’ll get another chance to buy at 2002 prices in the not-too-distant future.

“I so wish I bought a couple more properties in 2002 when everybody was calling for the crash looking at that chart. wow.”

Or in 1990. After only 8 years you could have been even. wow.

For what it’s worth, the Chronicle today published the 3/07 CAR median price data for single family homes– and states that the median price for a single family home in the SF Bay Area increased 5.6% for 3/07 over 3/06.

However, the median in the city of SF was down 2.5% year over year.

Dan, do you mind posting the Chronicle link showing a 5.6% YoY increase in SFHs in the Bay Area? I think that number is actually about right, in terms of the last 12 month’s appreciation from the many examples I’ve seen. 5.6% return on a 20% downpayment is 25%, not bad for just living in a house.

Thnx in advance Dan!

“For the Bay Area, the report showed home sales volume down 16.7 percent compared with last year and median price up 5.6 percent, to a new record of $785,380.”

http://sfgate.com/cgi-bin/article.cgi?file=/chronicle/archive/2007/04/25/BUGAOPELMV35.DTL&type=business

Prime – it’s great to see you’re on record in support of the Chronicle numbers! They are based on the latest CAR report which shows San Francisco County DOWN 2.5% YOY.

http://www.car.org/index.php?id=MzcyNDM

Assuming 20% down that’s a 12.5% loss on your investment over the past year. Leverage works both ways.

Also worth noting what Thornberg says in the same article:

“The median price is a bunch of hogwash,” he said. “You can have prices looking like they’re up when they’re down, because it is incredibly subject to where slowdowns are occurring. If there is more slowdown in a (lower-priced market), then you could show the median price going up just because there is a shift in the type of product being sold.”

Thanks Dan! Great news that SFHs in the Bay Area are at a new record. I’ve always believed prices in 2006 went up anywhere between 3-8%, depending on how good your location is in SF. This data just goes to prove it. Thnx again!

*****

“For the Bay Area, the report showed home sales volume down 16.7 percent compared with last year and median price up 5.6 percent, to a new record of $785,380.”

http://sfgate.com/cgi-bin/article.cgi?file=/chronicle/archive/2007/04/25/BUGAOPELMV35.DTL&type=business

Wow, a direct quote from Prime: “This data just goes to prove it.”

What’s amazing is that “this data” shows prices in San Francisco County fell 2.5% over the past year.

http://www.car.org/index.php?id=MzcyNDM

“For the Bay Area, the report showed home sales volume down 16.7 percent compared with last year and median price up 5.6 percent, to a new record of $785,380.”

http://sfgate.com/cgi-bin/article.cgi?file=/chronicle/archive/2007/04/25/BUGAOPELMV35.DTL&type=business

Yup the Median is up and the CSI is negative … just another example of why the Median is a poor way to measure home value.

Remember, kids Medians are NOT prices.

“You can use statistics to prove anything….27% of people know that.”

Homer Simpson

“Assuming 20% down that’s a 12.5% loss on your investment over the past year. Leverage works both ways.”

Taking into consideration a 6% sales commission and some staging cost, I would say the 20% down payment investment is down 50% and not 12.5%. Leverage works beautifully. Both ways in fact.