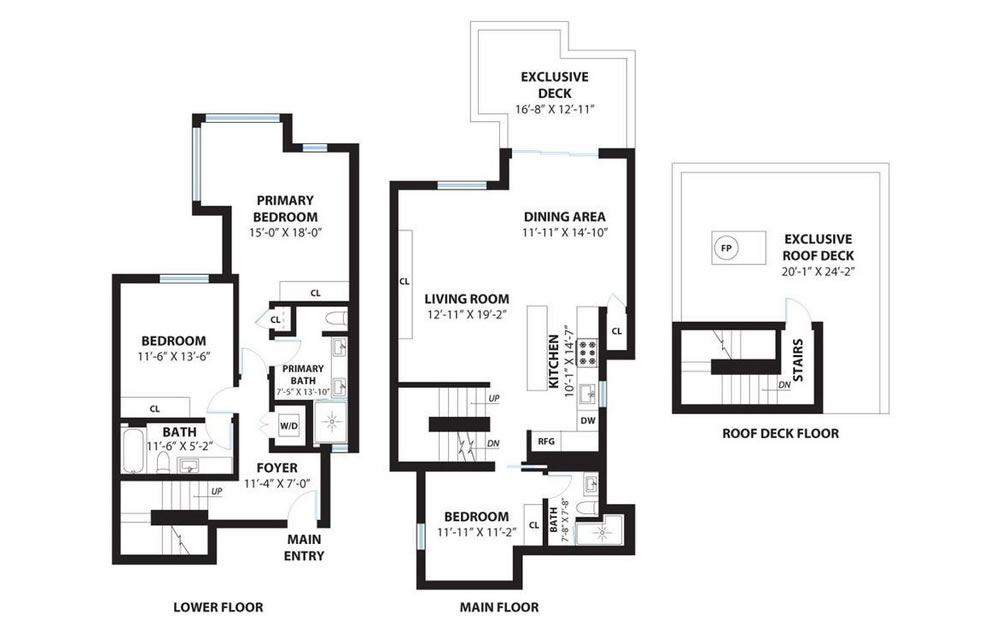

Measuring nearly 1,500 square feet, with three bedrooms, three baths, a deeded parking space and a private roof deck with “HUGE VIEWS,” the two-level penthouse unit at 1637 McAllister Street, “the pinnacle of luxury,” sold for $2.1 million in November of 2016.

Conveniently located “in the heart of SF’s dynamic NOPA District,” the “ultra-cool” condo returned to the market priced at $2.3 million three months ago, a sale at which would have represented net appreciation of just 9.5 percent over the past seven years.

Reduced to $2.095 million in October, the resale of 1637 McAllister Street has now closed escrow with a contract price of $1.9 million, representing a net 9.5 percent drop in value for the high-end NoPa condo, below its 2016 price, on an apples-to-apples basis. And yes, the widely misreported index for “San Francisco” condo values is “still up 20 percent!” over the same period of time.

Breaking News! Real estate prices don’t always rise. Who knew?

I have been reading this site since it started. 2006, I think. At the time, there was a lot of speculation in the market. Many of us could see it it as it was happening and weren’t surprised by the events of 2008. 15 years on, the continued editorial slant of schadenfreude does get tiring. Homes aren’t like the stock market…you don’t always get to pick when you buy and when you sell.

The market sucks right now. We all get it.

You know, it’s funny. I don’t recall seeing any of the commenters on this site who want housing prices to go down in order to accommodate those who already living here and not working “in tech” to find and keep housing, who want gentrification to slow down or cease, who want less competition for housing from investors solely buying rent-controlled units here in order to evict their residents and “Airbnb it!” complaining about “the continued editorial slant” when prices are monotonically increasing.

Does “The market suck” for them during those periods? Or does the market only “suck” when prices are coming down? Enquiring minds want to know.

What I have seen on this site, the SFGate comment section and other local media, and heard in the general discussion is that somehow San Francisco was a special place exempt from the basic economic principle of supply and demand, so there was “no way to build our way” out of the housing shortage and any new housing would only “ruin neighborhood character” and lead to gentrification. So, for many decades, most of the same people lamenting the city’s housing shortage strangely fought tooth-and-nail to uphold the development restrictions and burdensome procedures that contributed to making SF one of the most expensive and difficult places to construct new housing—of any kind. For example, witness the years long battle by neighbors in the Sunset to block the 90-unit *affordable housing* project at 2550 Irving Street, including appealing the permit *twice* to the the Board of Appeals, and trying to get a legal injunction, after* the project had already been approved by the Planning Commission and the Board of Supervisors.

So, while I find all these smug articles about upscale houses and condos fetching lower prices in the current market to be repetitive and dull, it is satisfying to be proven right that the law of supply and demand applies even to the city if San Francisco.

You have not been “proven right,” and the resort to a “simple” or “basic” economic “law”(sic) instantly betrays either a non-disinterested position and/or a superficial knowledge of economics . Thank you for mischaracterizing those of us against gentrification and/or who question ham-handed wielding of orthodox macroeconomic hoo-haw, but crude S&D theory as taught in Econ 1 for Dummies is not a sophisticated, quantifiable metric that accurately models non-fungible, non-homogenous, highly illiquid, speculative asset markets.

Building a glut of expensive “market rate” housing, in a ZIRP environment along with explicit and implicit subsidies that encourage gambling, does nothing to put downward pressure on “workforce” housing. What it does do is create a feedback loop of gentrification that increases land values, attracting development but pushing up development costs, putting upward pressure on prices that increase land values, until either credit dries up and/or the manipulated conditions that spawned the speculation end and the mania drifts to other pastures.

You can’t build your way out of a bubble. What you can do is overbuild for the bubble, making the hangover much worse. Clearly we’re at an impasse, but may I interest you in millions of sq ft of vacant office space that no one wants at any price?

What I read in your long diatribe beers is that you (A) hate to be proven wrong and will never admit it, and (B) you agree that price IS impacted by supply, even in San Francisco.

Also, what “impasse” have we reached since my comment was not directed to you, nor have we engaged in any sort of discussion or debate? What I think you mean to say is you are angry someone dared to post a comment you disagree with, which is a sign of dogmatism, not an “impasse.”

Moreover, I think you know the commercial real estate you reference declined in value not so much do to overbuilding—not in a development environment strictly controlled by Proposition M and its subsequent regulations— but rather due to the sudden and explosive rise of remote work brought about as one of the lasting impacts of the pandemic. But, I am glad you dis bring up the millions of square feet of vacant real estate in the city as they provide a text book case of prices plummeting when supply far exceeds demand. And, this is real estate that is now cheaply available for the companies who do still want to rent in S.F. (such as AI startups, etc) or to be repurposed for educational, residential, or other uses. And, commercial buildings in San Francisco are still finding buyers, just not for as high a price as they once fetched. So, once again, you acknowledge the basic market principles of supply and demand *do* apply even to

the magical land of San Francisco. Thank you for (indirectly) admitting that much.

It is also interesting that your response referenced “gentrification” and “expensive ‘market rate’ housing” when the example I gave was about neighbors in the Sunset trying for years to defeat an entirely affordable housing project. It seems their concern was less about “orthodox macroeconomic hoo-haw,” and more about the “poors” moving in next door.

The simplistic argument that WFH is the sole cause of the collapse of SF commercial real estate and that S&D theory explains all market activity has its appeal, but some people take a more nuanced view that the causes are many and more complex and include, as has been noted elsewhere, increasing “tech” monopoly and monopsony, layoffs, the end of ZIRP and QE, less capital flight and money laundering, and collapsing social infrastructure abandoned to an economy heavily based on financialization and war. Without the foregoing, there would have been little or no overbuilding to begin with, but then, neither would there have been a bubble.

Generally, a “bad” market in anything is defined as prices dropping.

We have both been following and commenting on this site for a long time. More often than not, the bias here has been to highlight how much money some individual lost on one property transaction somewhere in the city. And falling prices this time haven’t helped anybody. Even with prices down, monthly payments are sharply higher. Let me know if you think homes are more affordable now than they were 2 years ago.

It’s a fact…nearly anyone who purchased prior to rates increasing and has a loan at 4% or lower (that’s most them) is way ahead (based on monthly payments) if they don’t plan on selling for awhile. Much of their housing value is in their loan. I’m sure this blog will be able to find a few examples of people who purchased in 2019 and are reselling now for 50% less but that isn’t the situation for most homeowners. Also, as far as I know, interest rates have increased everywhere…not just San Francisco.

There is one commenter in particular who, apparently, lives out-of-state and enjoys stopping by to explain why San Francisco is doomed. It just gets old.

Those of us who post may be regulars but I suspect there are a lot of lurking visitors who are brand new every week, and this message is not old to them. Both buyers and sellers need to be aware of the current state of the market and these posts do that.

I’ll chip in to the contrary. It’s nice to balance the inevitable characters one encounters at any social function who can’t help tuning up their bragadelia song – when the market happens to go their way.

How might we decouple the impact of higher rates with the impact of a potential decline in popularity of San Francisco in general (due to work from home, etc)?

I’d add layoffs, the end of QE, less foreign capital flight, and problems with AirBnB to your mix of normalizing rates and WFH, which makes unraveling cause and effect more problematic.I don’t think it has anything to do with a decline in the “popularity of San Francisco” per se, although there may be a young coder cohort that is moving because there are no longer three boba joints per block. Now there are only two..

i think the young coder class has been increasing for the past 2 years. the decline is in upper middle class folks with kids. by the way, why would anyone pay $2.3M in 2016 or even $1.9M now to live in a 1500 sq ft condo in this location. its still absurdly overpriced and you can get more value now in SF.

A buyer would be paying a premium for the penthouse here. 1500 ft.² does seem kinda small for 3 bedrooms & 3 bathrooms, but the pictures above make the bedrooms, at least, seem reasonably sized. And they get a dedicated roof deck that looks to be about 485 ft.² going by the floor plans.

This isn’t a place intended for an upper middle class couple with kids, it’s a pad for two or three roommate millennial coders that want to throw parties on the weekends when they aren’t working and impress their friends. Unfortunately for the seller, that is just the demographic that is being laid off in droves from companies currently situated in San Francisco. They were lucky to get rid of this for only a 9.5 percent drop in price.

Nope. Lots of young techies have been moving out of the Mission over the last couple months, roughly coinciding with the new wave of layoffs (I know: correlation is not causation), and the last few weeks especially, more than enough to offset the comparatively smaller inbound contingent of AI fluffers. It’s not like the techxodus of covid summer, but it is noteworthy.

“Lots of young techies have been moving out of the Mission over the last couple months”

– And you know this how? Just curious.

Very simple: i ask them when I see them keeping an eye on the moving van while it’s being loaded. Even if I didn’t get verbal confirmation, techies are easy to spot and there aren’t many “upper middle class folks with kids” living in old apartments on Capp, in coder cubicles at NEMA or Madelon, or in faux lofts on Harrison, “upper middle class” and “kids” being the qualifiers here.

So you really have no basis. Got it.

Yes, it’s anecdata. Just like covid spring, when anyone could see that a massive exodus was under way, but many scoffed (perhaps you?) until it was finally reported in the New York Times many months later.

Another source is U-Haul clerks, but that is also anecdata. There is no regularly updated data I’m aware of on neighborhood migration in SF, so the deniers can keep whistling past all the obviously vacant units in the Mission (and who knows how many other units are vacant), until the Times reports on it sometime next year.