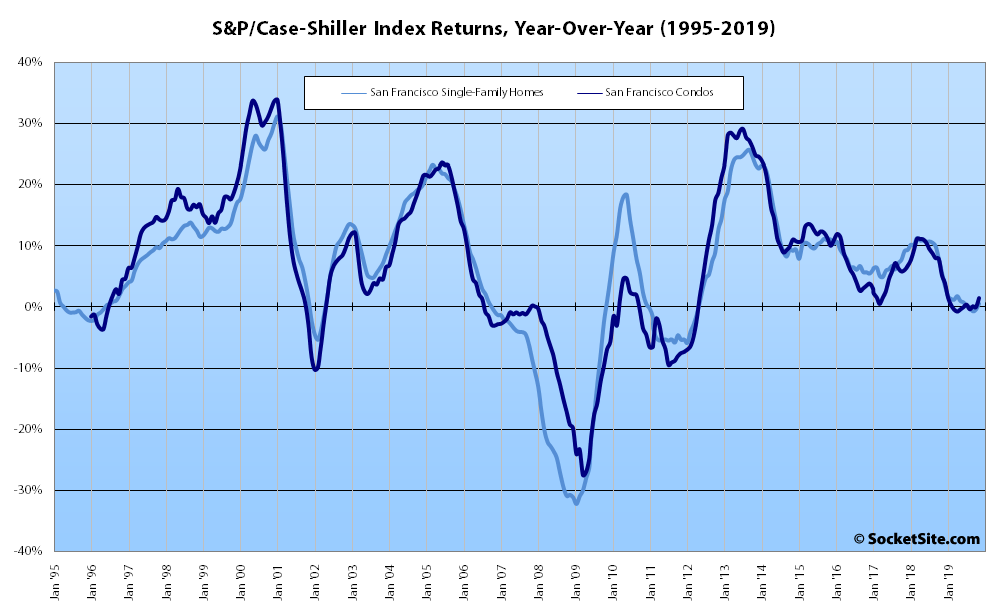

Having dropped a total of 1.5 percent from July through October, the S&P CoreLogic Case-Shiller Index for single-family home values within the San Francisco Metropolitan Area – which includes the East Bay, North Bay and Peninsula – inched up 0.2 percent in November and is now running 0.5 percent higher on a year-over-year basis, representing the first year-over-year gain for the index in four months.

At a more granular level, the index for the bottom, least expensive, third of the market shed 0.6 percent in November but remains 1.9 percent above its mark on a year-over-year basis (versus a year-over-year gain of 6.2 percent at the same time last year); the index for the middle third of the market, which peaked in 2018, was unchanged in November, resulting in a year-over-year gain of 0.1 percent; and while the index for the top third of the market inched up 0.6 percent in November, it remains 0.1 percent lower on a year-over-year basis versus a year-over-year gain of 4.9 percent in November of 2018.

At the same time, the index for Bay Area condo values, which peaked last July, dropped 0.9 percent in November and is down 2.0 percent since mid-2018 but managed to record a year-over-year gain of 1.5 percent.

Nationally, Phoenix is still leading the way in terms of home price gains, up 5.9 percent on a year-over-year basis, followed by Charlotte (up 5.2 percent) and Tampa (up 5.0 percent). And of the top-20 metro areas tracked by the index, San Francisco ranked second to last in terms of year-over-year gains at 0.5 percent, ahead of only Chicago (which was up 0.4 percent) and versus an average gain of 3.5 percent nationwide.

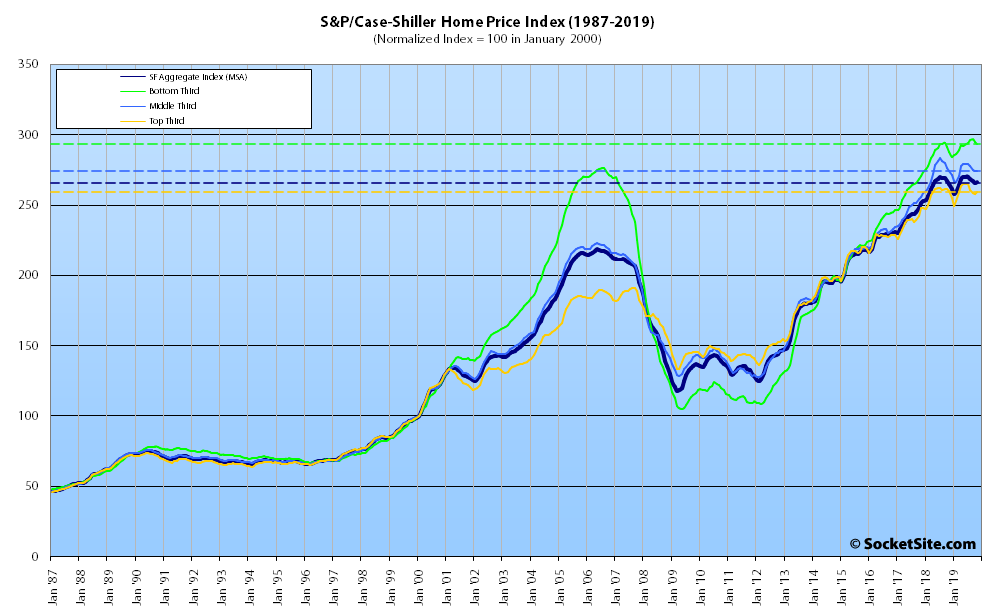

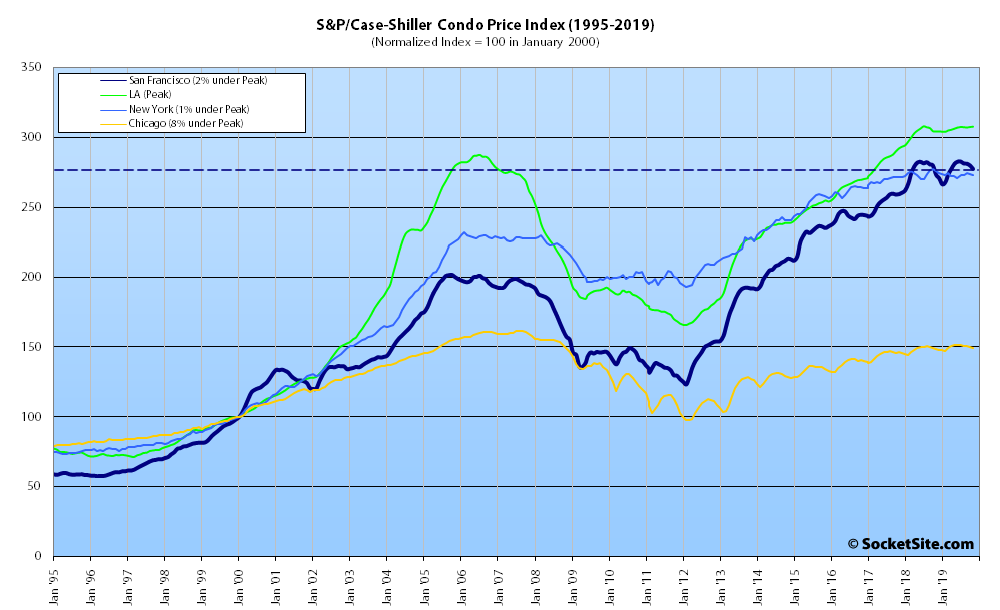

Our standard SocketSite S&P/Case-Shiller footnote: The S&P/Case-Shiller home price indices include San Francisco, San Mateo, Marin, Contra Costa and Alameda in the “San Francisco” index (i.e., greater MSA) and are imperfect in factoring out changes in property values due to improvements versus appreciation (although they try their best).

Looking a lot like ’07. Up, flat, down, rinse and repeat.

yeah, one more hump in this cycle in the summer of 2020 and then down for a bit.

Do you think we can hit a new high? Some impressive closings in January already…

well it depends how you look at it. I don’t think we will see any Glen Park sales do better than 143 Laidley ($9.7m) or 1783 Noe ($7.4m) in price or $/ft. We may see the highest $/ft in Noe, and will for sure see the biggest top $ with 235 Jersey. In Bernal we will not see the 2018 heights in $/ft of 2 bonview or 160 Bonview.

So kind of like when 350 Jersey sold for $7.2m and I said that was a new high mark, but that was only on pure dollars it wasn’t the biggest $/ft. and around and around we go. But my take is we stay roughly where we are at for 2020 in the Single Family subset.