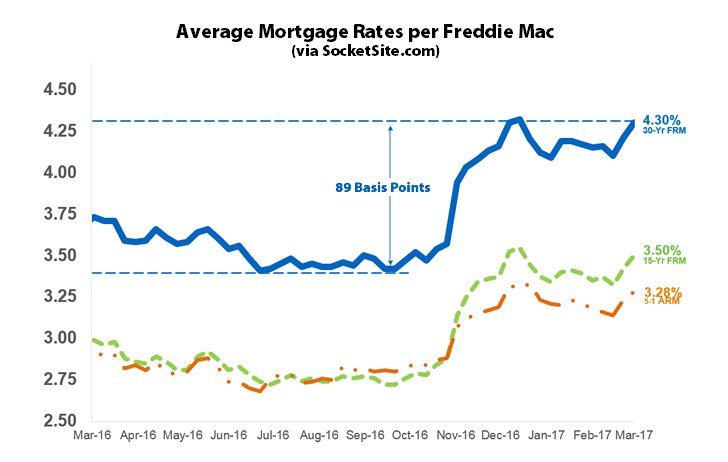

Measured prior to the Fed’s rate hike yesterday but with the probability already priced in, the average rate for a benchmark 30-year mortgage ticked up another 9 basis points over the past week to 4.30 percent, nearing the 4.32 percent rate in place at the end of last year, which was the highest rate on record in three years.

Having jumped 76 basis points over the past four months and 89 basis points since July, the current 30-year rate is now 57 basis points above the 3.73 percent rate in place at the same time last year, according to Freddie Mac’s Primary Mortgage Market Survey.

And according to an analysis of the futures market, the Fed’s next rate hike is now expected to occur as early as June, the current probability of which is 53 percent.

It will be interesting to see how the housing market will react to 100 bp increase. That has to be a huge increase monthly on a 800k mortgage! It will be fun to watch if rates climb back to 5% range even. Assuming a recession doesn’t happen first.

It was in the late 70’s or early 80’s when bank CD rates were 15%+ so I assume mortgages were even higher. It was a big recessionary period then and your run of the mill SFH in the central or Outer Richmond or Sunset districts could be purchased for less than $100K, depending on condition.

Will the above happen again? There is always a possibility but probability is not high.

Peak 30yr fixed mortgage rate was around 18.5% in 1981.

Wouldnt want one of those 7 year arms…

Any metrics on what percent of mortgages in last 5 years or so were ARMs?

Every TIC loan is ARM. Since 2012, there have been 1,500 TIC units sold in SF. I’m sure a small portion were all cash or group loan though. And these loans were made at rock bottom interest rates.

If I’m not mistaken, every half point rate increase adds about $300 to the monthly nut on our run-of-the-mill 1 million dollar median property. So let’s say rates go up a point, $600/mo. For most SF buyers these days, that is probably chump change, but I imagine it would have a big effect on the market for smaller condo/TICs, which would be compounded by the fact that we’re building new ones at a rapid pace.

That’s going to hurt – the other option to guard against interest rate hikes (more to come in 2017) is to pay off ARMs sooner, rather than later. Stocks have their run ups in several months and I would be surprised if some buyers or prospective buyers did not use their gains to either pay off part of their loans or use it for a bigger down payment.

We could see another big push to ease condo conversion rules too. Not hard to figure out who the lobbyists are behind that.

That would be refreshing — saw a friend in a SF four-unit TIC building go through the entire painful decade long lottery process, code work upgrades, bickering/unhelpful co-owners, various lawyering-ups stints, and constant fear of co-owner defaults, etc. By the time it was converted into a condo., one of the co-owners (not the problem one) sold and cashed out.

When you deflate one bubble, another one elsewhere will form.

There’s no reason it shouldn’t be eased for existing longterm TIC owners.

I think that generally ARM share has dropped significant since the 2007 bust. SF though is probably not a normal market. And also, many stats you find may only be reporting loans made via banks and non-bank lenders have become an increasingly large part of the mortgage market.

Finally, it’s as much an issue of having payments go up for prospective buyers of a house as it is for sellers who happen to have ARM’s.

10-year bonds are now a full 10 bps lower since the Fed’s rate announcement on Wednesday. Anyone wagering on significantly higher mortgage rates anytime soon is going to be sorely disappointed.

San Francisco RE is an all cash purchasing market. Not much will change

Not as much as it would seem:

“It’s called delayed financing, in which buyers pay cash for a home and then take out a mortgage soon after closing. Rarely used even two years ago, experts say it has picked up over the past 12 months.

“It was an extremely unusual phenomenon, but it’s going on quite a bit now,” says Jack McCabe, an independent housing analyst in Deerfield Beach, Fla.

The practice is growing mostly in affluent coastal housing markets, including New York and San Francisco.”

Bond yields down again. NASDAQ just hit a new record high. Not the stuff of which imminent bay area housing crashes are made.