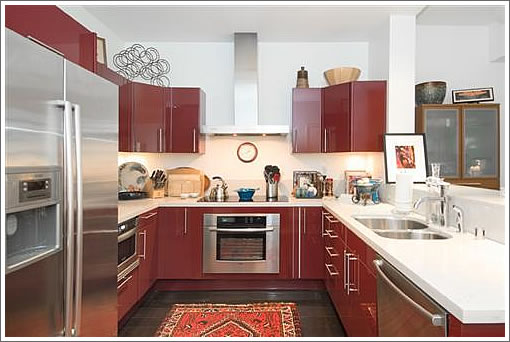

Plugged-in people knew the short sale had been approved and the list price reduced to $480,000, a sale at which would have been a 34 percent drop in value for the Jackson Square condo at 733 Front Street over the past three years.

This past Friday the sale of 733 Front Street #407 closed escrow with a reported contract of $450,000, 38 percent below its September 2007 purchase price of $730,000.

Don’t forget those invitations to the house warming, paying attention to those “bitter” bears three years ago just saved you $280,000 (and buys an awful lot of champagne).

Hmmm, time to adjust my 20-35% off peak comments. Looks like 20-40% is more like it, with some homes and areas down a little more and some a little less.

At 38% off for a pretty desirable area, we’re getting to the point where the risk of further declines is not huge, but it’s still 50-50 with interest rates poised to tick up. And it is remarkable that even after a 38% decline it still makes more sense to rent. Shows again how absurd the 2005-2008 pricing was as was all the spin attempting to justify it.

They overpaid!

Listening to bears won’t get you the house you want.

ok ed.,

i think i get it; everyone who was bearish on sfre was right. it does not matter if they were calling for 40-50%off or 5-10%, if they were calling for this to happen in ’07 or ’08 or ’09 or ’10 or if it was an arm reset tsunami…close enough..

They were all varying degrees of correct, anonee. By contrast, those who postulated that prices in SF would never fall, or would always outperform other investments, were all varying degrees of wrong. Before scoffing at those old tsunami predictions, imagine how bad things would be had the government not nationlized the mortgage market.

And listening to bulls won’t get you the price you want.

That’s $576 psft for a top of the line build in what had been a top of the line location, for those keeping track of where prices are headed.

I had to double check my math to make sure I had that right.

HOA dues are reasonable at $650.

One more note: this went pending at the low point in interest rates, you’d have to pay about $525 psft to hit the same total payment today.

@legacydude,

“They were all varying degrees of correct, anonee. By contrast, those who postulated that prices in SF would never fall, or would always outperform other investments, were all varying degrees of wrong. ”

ok aside from one poster making that statement (sort of)i do not think anyone else on this site ever made such claims. ever. the bulls tended to say that the bears were too pessimistic.

i bet the cumulative predictions of the few contrarian voices here are far more accurate than the tide of bear tipsters.

“You got to know when to hold ’em, know when to fold ’em

Know when to walk away and know when to run

You never count your money when you’re sittin’ at the table

There’ll be time enough for countin’ when the dealing’s done

Every gambler knows that the secret to survivin’

Is knowin’ what to throw away and knowing what to keep

‘Cause every hand’s a winner and every hand’s a loser

And the best that you can hope for is to die in your sleep”

yeah, ninnee, sfre bears are all wrong. No arms reset tsunami happened just as you predicted! we are “surprised” es ef is holding up so well. everybody knows “good seats” are doing fine in es ef. and sub-par units in sub-par locations deserve to take it in the shorts.

I am surprised you’re not gonna dismiss this “singular” apple or explain it away in terms of “short hold”, “interchangeable luxury condo” or lack of “actively adding value”.

Stalker Dude

Perhaps I’m old fashioned, but I think buying a home for you and your family to live in should not be like playing poker.

Hopefully now that the credit bubble has popped and is deflating, all those flippers, “short-term-hol”-ders, speculators and “real estate investors” hoping to “Buy, Sell, repeat, retire” will find something more productive and less harmful to honest, hard working people to do with their time. Like get a real job that makes a contribution to, rather than extracting value from, society.

“No arms reset tsunami happened”, did it happen?

“No arms reset tsunami happened”, did it happen?

nationally, without question. all one needs to do is look at the foreclosure/delinquency/short sale stats across the country.

did it affect the so called “real SF”? that is a matter of debate.

I would propose that it likely did. This could be a PARTIAL (not full) explanation of all the homes we see up here that are sold 2-3 years after purchase.

2-3 yrs. after purchase is ahead of lots of resets. The tsunami being a ton reset at once (or nearly) and the new price bring them all to market together, I don’t think we ever saw that. I think we have seen a lot more gradual selling before the reset. Plus at this point the ’04-’05 purchases have already reset, plus the shorter reset 06-’07 purchases.

As always I was talking SF, not nationally.

“Scare tactics are dead. San Francisco never really took a price hit and it won’t , either.”

Posted by: fluj/anonn/anon.ed/? at June 23, 2008

@tipster, since when is $650/mo HOA fees reasonable? Especially on something that sells for $450k. That’s a huge percentage of the monthly payment. For that kind of monthly, I’d expect something in the $300/mo range for HOA fee.

Interests rates are still fairly low, so I don’t think a reset tsunami has really happened yet.

But some people confuse the terms “reset” and “recast”. Here’s a good blog post on the topic:

http://www.calculatedriskblog.com/2008/08/reset-vs-recast-or-why-charts-dont.html

For Resets, it is worth noting that the fed is going to extreme lengths to hold down interest rates. I don’t think that anyone thinks that this can last forever.

For Recasts, consider that for this to have an effect you must first hit your recast limit (time or money), then go delinquent, and then finally have the bank take action against you. Given that people are going a year plus without making payments, it seems reasonable that this process could be quite drawn out.

The short sale/foreclosure tsunami is just beginning for this building; most of these units were sold at the height of the craziness.

I guess if they hold long enough, say 15-20 years they should break even.

ok aside from one poster making that statement (sort of)i do not think anyone else on this site ever made such claims. ever. the bulls tended to say that the bears were too pessimistic

maybe. however when I first started posting the Credit Suisse reset charts (this was well before the recession began, and when many areas were still in full bull mode) I remember many posters telling me that SF was “different” and “special” and that it wouldn’t be affected like other places due to its specialness.

they would then characterize me as a bitter person who just couldn’t hack it in SF and thus was trying to bring everybody down.

(remember Esther? or Gdog?)

here’s a typical quote:

Good luck waiting for prices to fall 10% in SF!

Posted by: anonymous at May 1, 2007 12:01 PM

or here’s another:

I actually do believe prime location 600-700sqft studios will be over $1 million by 2015. That’s simply $1,500-1,600/sqft, which is the norm in many other cities such as London, HK, Tokyo, etc.

It always seems expensive now, and then you wait a year and realize, you made the right choice.

I actually the Fed will start cutting rates next year, allowing many to refi to longer term mortgages at the same rate or lower. Nobody is talking about lower rates. The Fed will save middle America, and coastal America is going to go hog wild for more cheap money. It’s a great system.

Anybody want to talk about the 13 out of 14 sales at big bucks at 3208 Pierce St. in The Marina?

Posted by: Prime at May 1, 2007 9:19 PM

when the garbage started hitting the fan I agree that many bulls changed their position to “it won’t be as bad as elsewhere”.

and clearly there were some bulls whose only point was that the bears were over-reaching. I agreed with those bulls at times depending on macroeconomic fundamentals…

scurvy, it seems that the practical “floor” for HOA fees is $300/month. This is probably due to the fixed costs of running an HOA and the irreducible expenses that an HOA would incur.

The only place I’ve seen that’s lower than $300/month is the Book Concern Lofts which are freakin’ tiny (under 270 sq. ft.) and the HOAs there are $288/month for places that are now asking $268k (were asking $273k for another unit when socketsite last posted on that building), which has to be rock bottom when you’re in The City, ’cause of the district.

Regarding resets & recasts. Wells, who inherited the Wachovia portfolio, has been doing its best to avoid the tsunami (or at least pace it out over a longer period of time) as they have been doing aggressive loan modifications.

In other cases, simply getting more reasonable terms may help a family stay in their home: The loan modification Lisa negotiated for the Capristos sets their interest rate at 2 percent for five years, followed by 1 percent increases until it hits the ceiling of 5 percent. How do I get that deal?

“How do I get that deal?”

Agree to keep paying on a mortgage balance that is far underwater, thereby allowing the bank to keep the balance on the books at full value, thereby hiding the loss, until you walk away in year 8.

Does anyone else find it funny that kid char/paco/anonee doesn’t make predictions but constantly repeats the more extreme predictions (without picking any mainstream ones)?

I’m with EBGuy on the Option ARMs. Some of those loans have been more heavily modified, generally without principal reduced, but ridiculously low interest rates for a longer period. Nonetheless, Option ARM loans have a higher foreclosure rate than subprime: http://www.calculatedriskblog.com/2011/01/what-about-those-option-arms.html

tc_sf makes an important point about resets and recasts. Resets are completely unimportant because interest rates are low, as subsidized by Uncle Sam and its comrades. No one should care about resets until interest rates go up.

Recasts, which is reamortization, is far more important until interest rates go up. Some of the modifications have pushed off recasts as well, I believe. For the time-based recasting (e.g. 5 years, but sometimes up to 10 years), some of the analyst charts suggested a peak of either 2011 (link below) or 2012 (link above):

http://www.calculatedriskblog.com/2010/01/option-arm-recast-update.html

However, some loans also have alternate recast schedules based on LTV, and may not recast until 2014/2015 or later because interest rates are so low, as Wells Fargo is predicting — they project very few recasts before 2012:

http://healdsburgbubble.blogspot.com/2009/05/reset-chart-from-credit-suisse-has.html

paco has been at this tactic for quite some time. here’s a sample from Nov 2008.

“i’m surprised that the bears cannot come up with more stories about people over reaching and then having to punt. ok, maybe in daly city or d10 or wherever (those outer burbs the above poster cites so often?)

c’mon bears! thousands of units have traded in real sf in the last few years so where’s this 30-40%

drop happening?

now i know this is an easy one for you bears so i’ll sit back and wait to hear about all those rotten apples…”

Posted by: paco at November 11, 2008 7:33 AM

https://socketsite.com/archives/2008/11/where_the_wild_things_arent_179_delmar.html

EBGUy,

I agree with you on the recast vs. reset, it should be called the “OptionARM recast tsumani” but it’s not.

And I think what you posted goes to what I was saying. The ’04-’05 have already gone past the 5 years. Sales of the ’06+ have been ongoing to so the wave of a bunch at once is diminished.

the reset has some importance because over the years it moved the minimum payment up and then when the rates went way down the payment stayed up and people were forced to pay closer to the full amount. As rates have gone even lower people have been paying down mortgages with an amount that used to be the minimum and so they aren’t forced to sell anymore; minimum payment has become full amortized.

Here’s one of the wildest loan mods that I’ve heard of — courtesy of Wells Fargo. A huge chunk of the loan (the underwater portion) is deferred at 0% interest and due as a balloon payment at the end of the 30 year term. Glub, glub, glub…. something about cement shoes.

SS’s most recent inventory post noted that 27% of all listings are either REOs or short sales. The percentage of listings of post-2004 resales that are distressed is certainly far higher (no, I do not have hard numbers, but I do have common sense). It is not unreasonable to assume that a big chunk of those are re-casts where the teaser payment multiplied so the buyer just gave up. It certainly may be that all of these are just underwater and distressed for other reasons but that is highly unlikely — and even if true, it bodes far worse for the SF market going forward as at least the re-cast issue will go away in a number of years whereas structural unaffordability problems will linger.

“A huge chunk of the loan (the underwater portion) is deferred at 0% interest and due as a balloon payment at the end of the 30 year term. Glub, glub, glub…. something about cement shoes.”

The balloon payment method is not uncommon for a modification. A common method is amortizing the loan for 40 years and having a balloon due at the end of the 30th year. If you look at an amortization table, that would mean the balloon is 45.5% of the principal, which is hardly a bargain.

That way, if there is significant appreciation, the bank/investors reaps a benefit from that appreication, but otherwise it’s a write-off in 25 years or so.

@sparky-b: I’m not sure the 04-05 wave is done yet. As pointed out above a number of the Wells Fargo (was Wachovia) loans were 10 year time based recasts. But even for the 5 years, this puts re-cast in 09-10.

Some people may try making payments for a while, but even if you immediately default the average number of days between default and losing the property in CA was 415 days as of last June. ( http://www.nytimes.com/2010/06/01/business/01nopay.html?_r=1&scp=1&sq=not%20paying%20mortgage&st=cse )

This has you losing the property in the ’10-’12 range. Then it may sit on the banks books for a bit before it hits the market.

Regarding loan modifications, the data I’ve seen on the government modification programs has been abysmal as far as affecting any significant portion of the market. Information on internal modification programs seems more hazy. Hard to say if doing a modification for the family of someone serving in Iraq with TV news involved is typical or just a PR move. Note that in the linked article, the bank did initially start foreclosure proceedings.

In general, as tipster pointed out, for someone with an Option ARM a modification may be a hard sell. Not sure what the average payment rate is, but during the boom I seem to recall seeing quite a few loans with ~2% payment rates.

Although typically not true with a fully amortizing loan, with a 2% payment rate you very well may be paying less on the mortgage then comparable rent. Not sure if the neg-am part is legally non-recourse, but it is probably practically non-recourse. So why not just make the minimum payment for as long as you can, do a year of non-payment and then just walk? Especially if you have one of the Wachovia 10-years, seems hard to offer you a mod that beats that.

OptionARMs are at like 2.7%, but the minimum payment or full payment actually covers a lot more than that.

Maybe someone got one at 2% and paid the minimum, but that went up the next year and the next, then it came way down. The minimum payment is now at or over the full amortized. Maybe they owe more than the house is worth but it’s still affordable, and for the same payment they are paying down the house.

“i bet the cumulative predictions of the few contrarian voices here are far more accurate than the tide of bear tipsters.”

those bears of us who were posting here in 07-08 were the contrarians. in 07, 85% of posters were permabulls

@sparky-b: I haven’t seen any good hard data on average payment rates for option ARM’s. Just recalling what I saw. Some loans had yearly payment changes, some only at recast. Do you have a source for the 2.7% number?

Not sure how the minimum payment could be over the full amortized payment.

For info on how these loans worked see this from Countrywide’s last 10-Q (p80-81)

“While new originations of these products have virtually ceased by June 30, 2008, Banking Operations holds a substantial investment in pay option ARM and payment advantage ARM loans (collectively “pay option loans”).

•

Pay-option ARM loans—have interest rates that adjust monthly and minimum required payments that adjust annually (subject to recast of the loan if minimum payments are made and deferred interest limits are reached). Annual payment adjustments are subject to a 71/2% maximum change. To ensure that contractual loan payments are adequate to repay a loan, the fully amortizing loan payment amount is re-established after either five or ten years and again every five years thereafter. These payment adjustments are not subject to the 71/2% payment limit and may be substantial due to changes in interest rates and the addition of unpaid interest to the loans’ balances.

•

Payment advantage ARM loans—have interest rates that are fixed for an initial period of five years. Payments are subject to recast of the loan if minimum payments are made and deferred interest limits are reached. If interest deferrals cause the loan’s principal balance to reach a certain maximum level within the first ten years of these loans, the payment is reset to the interest-only payment; then at the 10-year point, the fully amortizing payment is required.

”

http://www.sec.gov/Archives/edgar/data/25191/000104746908009150/a2187147z10-q.htm

On the table right below this you’ll see that far from “maybe a few people made the minimum payment” as of June 2008 72% of people who made a payment paid less then the full interest rate.

(83% had low or no doc of income!)

This was in ’08. With prices down I don’t see much incentive for someone who is underwater to make more then the minimum payment and just run out the 5-10 year clock.

“Do you have a source for the 2.7% number?”. My bank, that’s what my rate is.

“Not sure how the minimum payment could be over the full amortized payment.”

My minimum when I got the loan was $600 more than my full amortized is now. Maybe my minimum wasn’t good compared to other peoples, maybe they got crazy in ’07-’08. Also, my original full amortized vs. my minimum payment option was only an $800/mo difference. If I had only paid the minimum they would have kept adding the 7.5% each year as well.

“Scare tactics are dead. San Francisco never really took a price hit and it won’t , either.”

Posted by: fluj/anonn/anon.ed/? at June 23, 2008

I must admit surprise at the absence of a convoluted attempt at rationalizing the above statement. Is Kenny losing his edge?

Seems like even Fluj has given up. Could this be the next leg down?

Despite the fools being bailed out / extended to eternity by the government and their banks, prices are still taking a big hit.

Over the pond, prices in Paris have climbed another 20% in 2010. As a consequence, the government decided to respond to high prices by giving out 40,000 Euro 0% mortgages that can be used as a downpayment. Regular rates have been under 4% for a while there.

In short, 0 down, rock-bottom rates subsidized by the government. I have seen this one before.