Carolyn Said takes a stab a calculating the Bay Area’s “shadow inventory” of foreclosure homes – propeties that have already been foreclosed upon but have not yet been registered in county records as having been resold.

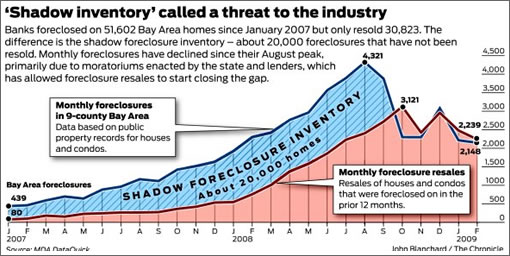

For the 26 months from January 2007 through February 2009, banks repossessed 51,602 homes and condos in the nine-county Bay Area, according to DataQuick. Yet in the same period, only 30,823 foreclosures were resold, leaving about 20,000 bank repos unaccounted for.

The county with the highest percentage of unaccounted for foreclosures? According to the Chronicle that would be San Francisco with 50.2% unsold versus an average of 34.5% for the Bay Area as a whole.

UPDATE: As noted, according to the Chronicle’s analysis 50.2% of properties that have been foreclosed upon in San Francisco from January of 2007 through February of 2009 remain unsold and constitute “shadow inventory.”

Based on our back of the envelope calculations, roughly 750 properties in San Francisco County became bank owned during that 26 month stretch. And as such, the Chronicle’s methodology would suggest around 375 bank owned units are unaccounted for.

At least 69 of those bank owned properties, however, are accounted for and currently listed for sale in San Francisco. And while 69 is not 375, it is a swing of roughly nine percentage points in terms of the percentage San Francisco foreclosure inventory that’s out in the open versus possibly lurking behind. No update for the Bay Area as a whole.

∙ Banks aren’t reselling many foreclosed homes [SocketSite]

worse yet there are many homes out there that should have been foreclosed upon, but weren’t. either because the bank is overwhelmed and doesn’t have thee staff/willpower to foreclose on any more homes, or due to the various moratoriums. this is mentioned in the article.

it’s also a possibility that the banks can’t foreclose and sell or they’ll have to realize an actual loss on their balance sheet that they can’t afford.

there are reports of people who are in homes for months without making any payments who haven’t received NOD’s.

The county with the highest percentage of unaccounted for foreclosures? According to the Chronicle that would be San Francisco with 50.2% unsold versus an average of 34.5% unsold for the Bay Area as a whole.

it would be nice to see the actual numbers on this. Is it a small number of properties in SF proper or potentially huge?

[Editor’s Note: Our back of the envelope calculation for San Francisco proper suggests roughly 750 recorded foreclosures since January 2007, so perhaps roughly 375 unsold.]

That seems like a factor over and above the focus of the story. Homes not yet foreclosed add even more to the shadow stock, and might be even more numerous. Wasn’t there a report that the process of foreclosing had slowed at some banks? Notices of default seem to be a noisy and inaccurate metric, possibly because so many pay late either out of sloth or as a way of getting an extension.

Some people are not paying intentionally for three months or more. They’re not doing so to get an extention. They’re doing it as a way to get a super cheap rate from the lender from numerous programs both subsidized and private.

anonn:

that might be true. however, as you’ve probably noted a high percentage of people who go through that process end up in foreclosure anyway.

of those loans “successfully” modified, over half redefault.

thus, while there are undoubtedly some people who are purposefully not paying so that they can get sweeter loan terms, the future for their particular outcome is poor anyway.

FWIW: many people are forced to do this, otherwise they can’t get the lender’s attention. If you have a loan that is resetting to MORE money than you take in each month you’d think the lender might consider renegotiating. however they won’t. unless you have 3 missed months.

so it’s hard to weed out those who just want sweeter deals from those who really “need” a loan mod (at least to stay in the home). but again, regardless, a high % of those in that situation default anyway.

I’ve seen reports that a substantial percentage still default after adjustment, yes. What was it, like 52% or something? I don’t recall. So multiply that percentage by the other percentage to get an understanding of what MIGHT be the actual “shadow inventory.” But remember, there are probably a lot of other folks living in a “shadow” house who will manage to stave off foreclosure too. You’ll say, sure, and there are a lot of people who think they’re still fine who will be facing difficulties down the line. That’s true as well. I would hesitate to call something “shadow inventory” if there is no intention whatsoever to sell. And I’d like to see an SF map too.

750 recorded foreclosures since January 2007, so perhaps roughly 375 unsold

Probably mostly D10. They went higher (percentage-wise) and are crashing harder. Tough to sell a SFH fixer with 500K due when some short sales are sitting unsold in the 300s. These areas still have ways to go.

SFS, the CW is that D10 went higher and is crashing (or will crash) harder, but I’m not so sure these assumptions are true. Gumby did some nice charts on a post a couple weeks ago using long-term average sales data by district (and Case Shiller):

http://chartmechanic.com/chart.jsp?c=demo/SF%20Case%20Shiller%20District%20Mashup.chart

I agree that foreclosures have been centered in D10. But that does not necessarily mean the crash will be restricted to D10. It’s all an integrated market. Regardless, FSBO also did a nice analysis recently of all the shadow inventory out there. Between that, the growing MLS inventory, the dwindling sales, and the foreclosures-in-waiting, the bottom-line is that we are many years away from seeing a bottom in SF.

I’m a bit confused over the use of the term “shadow” in this context. It isn’t like this inventory is hidden or not showing up in the MLS. As the way I understand it the figure present here (20k shadow foreclosure inventory) is just the homes that have been foreclosed on and not yet closed on re-sale. So for those 20k homes, I’d expect a certain percentage of them are on the MLS and being counted in the standard inventory of unsold homes.

[Editor’s Note: Excellent point (and we’re working on a follow-up post).]

As the way I understand it the figure present here (20k shadow foreclosure inventory) is just the homes that have been foreclosed on and not yet closed on re-sale.

Rillion: that is not the way the article worded it. the shadow inventory is the # of homes foreclosed upon that have not been relisted for sale. They word it thusly:

In a recent study, RealtyTrac compared its database of bank-repossessed homes to MLS listings of for-sale homes in four states, including California. It found a significant disparity – only 30 percent of the foreclosures were listed for sale in the Multiple Listing Service. The remainder is known in the industry as “shadow inventory.”

That’s true as well. I would hesitate to call something “shadow inventory” if there is no intention whatsoever to sell.

I agree. it’s hard to parse out.

Clearly, homes that are post-foreclosure but not listed are shadow inventory. Banks are not allowed by law to continue holding the property for too long. (not like laws matter to our current Fed/administration).

but I agree with you, it’s hard to know how many people intend to refinance and stay, versus simply walk away. but the 50% redefault number gives us a guess that at least half of those hitting NOD status will eventually redefault and go into foreclosure. it’s simply that they can’t afford the house. period.

this could change if the govt starts forcing cram downs or other principal modifications, which they’ve been reluctant to do.

Ok to bailout Goldman Sach’s bad bets… but not Joe 6 pack.

Banks are generally smart enough to know that flooding foreclosures on the market is not a smart strategy. The fact that there is even a minor flood suggests that there is still an even larger backlog in the waiting.

oops… later in the article they do seem to jumble the idea of REO’s that aren’t listed, and REO’s that simply haven’t sold.

For the 26 months from January 2007 through February 2009, banks repossessed 51,602 homes and condos in the nine-county Bay Area, according to DataQuick. Yet in the same period, only 30,823 foreclosures were resold, leaving about 20,000 bank repos unaccounted for.

I think they do this because traditionally REO’s are sold within 30 days. obviously this downturn isn’t typical. Thus, they’re calling REO’s that haven’t sold within 30 days “shadow inventory”. I agree that I’m not sure I’d use that term. I’d use “excess inventory” or “inventory overhang” or similar

Even so, it appears that only 1/5th of REOs are listed per the article.

Discovery Bay’s ForeclosureRadar.com compared its database of Bay Area foreclosures to MLS listings for the past 120 days and found that fewer than one-fifth of the foreclosures showed up as for-sale listings.

so it makes you wonder:

is the 20,000 the overall number, or is the “shadow inventory” 4/5ths x 20,000, or 16,000.

I’d use the latter number as “shadow inventory”. (unlisted REO’s).

Looking back to Jan 2007, where the chart starts, there has always been “shadow” inventory. As a %age, this “shadow” inventory doesn’t seem to have changed. So I, too, am having a hard time seeing the story there.

I think the interesting part of the chart is in August 2008 where bay area foreclosures drop and how the monthly foreclosure sales become more than the monthly forclosures, and thereby, seemingly, eating into the “shadow” inventory. But I think the explanation for this phenomenon is that the banks are not moving to foreclose on many properties that are in default.

chuckie:

even if the percentage is the same, it’s still a big issue due to absolute numbers.

at one time there were only 439 or so foreclosures, and 80 sold… leaving 360 extra properties out there.

recently (august) there were 4300 foreclosures, with only 2500 selling. that leaves 1800 extra properties.

and it’s been cumulative.

I WOULD say that 16,000 extra properties is a big deal. (remember, these are FORECLOSED so they must be sold at some point)

that said: we must not forget what happened in August: foreclosure moratoriums.

how long can govt keep this up? your guess = as good as mine.

I went with a friend to check out a condo that her agent said is REO but not on the MLS. She kinda like it and she checked the MLS and indeed saw no listing of said condo. My friend decided to pass and the condo was sold last month. Recently her agent contacted her with news that the buyer couldn’t get financing and the condo is back on the market, but still not on MLS.

I wonder how many REOs is not on MLS but are indeed on the market.

“I WOULD say that 16,000 extra properties is a big deal. (remember, these are FORECLOSED so they must be sold at some point)”

It’s taken a while for that number to build up, and it will continue to build for a long while. And it will take even longer to eventually work through this backlog. Certainly not a recipe for a bottoming out in the near future 🙂

UPDATE: As noted above, according to the Chronicle’s analysis 50.2% of properties that have been foreclosed upon in San Francisco from January of 2007 through February of 2009 remain unsold and constitute “shadow inventory.”

Based on our back of the envelope calculations, roughly 750 properties in San Francisco County became bank owned during that 26 month stretch. And as such, the Chronicle’s methodology would suggest around 375 bank owned units are unaccounted for.

At least 69 of those bank owned properties, however, are accounted for and currently listed for sale in San Francisco. And while 69 is not 375, it is a swing of roughly nine percentage points in terms of the percentage San Francisco foreclosure inventory that’s out in the open versus possibly lurking behind.

Just one case but friend at work was foreclosed on but allowed to “rent” for 6 months by the bank. They were just tossed out a couple of weeks ago. There must be many of these places that are in-between.

That was an excellent chart, but now I have some questions about the districts.

1) What districts have gone down the most and why? Are these districts “worse” areas living-wise? (As you can tell I’m not an SF native, but I will soon be)

2) Also, what do the changes in these districts mean to the rest of the city? Are these districts closer to the bottom waiting for the rest of SF to catch up? Or will they be the only big drops in the city?

I read the whole article at lunch and it cleared it up somewhat but I do notice that gives several different figures and percentages (% of homes not listed, % foreclosed but not sold, etc) while using the term shadow inventory multiple times, sometimes while referring to one or other of the different percentages. Really sloppy imo. That last update by the editor shows the gap in what the article presents as shadow inventory (foreclosed and not listed for sale) with the precentage they quote, foreclosed and not sold. The two are different but the article flips back and forth between the two making seem like they are both shadow inventory.

I just wish articles about a subject could help clarify the subject, not muddle it. Overall the subject of the article shouldn’t come as to big a surprise to anyone, there is still a lot of foreclosed inventory out there, not all of it listed on the MLS yet.

[Editor’s Note: Unfortunately the Chronicle article presents foreclosed and not sold as “shadow inventory” as well (note their graphic).]

Trip,

Great chart. I find it interesting how close the districts correlate to the CS chart when selected individually (except for D8).

Does this disprove the theories that “Real SF” doesn’t track with CS because CS contains East-Bay cities?

Why does D8 seem to have such a low correlation? I’m guessing it’s the low volume leading to patchier data.

Yeah, D8 has so few SFR sales (just a couple a month) that the numbers aren’t too useful. This was originally put together to test the hypothesis that the Case Shiller MSA (SF and a few neighboring counties) was disconnected from SF in terms of price trends. This result is not perfect (CS uses a repeat sale methodology and the SF district data from Blackstone uses monthly averages). Regardless, it does show a very close correlation over a long period — among SF districts and with CS. Note that there is a disconnect beginning about two years ago (my bet — averages were skewed up in SF by changes in mix), but in any event that is narrowing now toward the long-term correlation, as one would expect. Others will continue to shout “SF is different from the MSA” but unless they provide something other than “because I say so” to support it, such views should be discounted IMHO.

By the way, gumby put together these great charts, not me.

Great chart. I find it interesting how close the districts correlate to the CS chart when selected individually (except for D8).

They sort of correlate. If you look closely, you will see that D4 used to have the same median price as D5 in 1989, now it is 1/3 less. It is only a percent or two a year, but it adds up to a pretty big difference. During the 2000 run-up, SF prices jumped up first. But generally they seem to correlate.

Others will continue to shout “SF is different from the MSA” but unless they provide something other than “because I say so” to support it, such views should be discounted IMHO.

There have been four or five reasons put forward on Socketsite, you have just chosen to ignore or discount them. It is fine to say that you find the arguments presented unconvincing, but to claim that they have never been put forward is disingenuous.

In fact, NVJ,

Trip says, “Regardless, it does show a very close correlation over a long period — among SF districts and with CS.”

and then, “Note that there is a disconnect beginning about two years ago (my bet — averages were skewed up in SF by changes in mix),”

Translation: Never mind about that incongruous period! I’ll tell you what’s what!

But concludes, “but in any event that is narrowing now toward the long-term correlation,”

Hypocritical? You bet.

In essence it’s precisely what he says others are saying (but didn’t, because actual arguments were continually presented), which is “It’s this way because I say it is.”

And yeah, the shape of some of the graphs look the same. Three districts are breaking northward still. But the actual numbers can differ wildly over time for most districts versus CS.

Seriously, anonn, all you ever do on this site is mock others. Why are you so pathetic? That’s not a rhetorical question. I’m really curious where it comes from.

NVJ, the SF data are averages not medians. Medians would be better as averages tend to be more volatile and can skew high (and CS SF-only data would be better yet).

You write: “There have been four or five reasons put forward on Socketsite, you have just chosen to ignore or discount them.”

What are those? I recall fluj positing that “the internet” made the SF market different from its neighboring counties, and that was quickly shown to be nonsense. But what are the others you have in mind?

I remember the following:

1) San Francisco is unique and deserves a premium because of this.

2) There are more high paying jobs and opportunities here and these opportunities will be relatively worth more during a downturn.

3) Foreign buyers, particularly Chinese, will be unaffected by the economy in the United States and will continue to want to own property here.

4) As urban areas grow in population and particularly in density, land in the core is worth more.

5) The total cost of living in a place should include housing and transportation costs. Transportation has gotten relatively more expensive in suburban areas and this will probably only get worse, especially when you consider that California seems determined to underfund infrastructure, thereby making housing near jobs more valuable.

6) The top decile (in income) has disproportionately done well during the last decade, so markets that cater to them, including most of San Francisco, should outperform.

7) Credit was made too widely available in the last few years, creating a housing bubble. This credit was most excessively distributed to poorer exurban areas, which led to increased speculation there. San Francisco was less effected by this.

8) Wealthier buyers with better credit scores are more likely to attempt to hold on to their mortgages, even when underwater. They also have more financial resources, both formal and informal, to allow them to do so.

I have listed them in what I think is their plausibility. I am not sure anyone has made argument #1 except as a straw man, but I see people making it all the time, so I have included it for completeness.

Did I miss any of them?

Just to be clear, I think #1 is the least plausible and #8 the most. I should have said “increasing plausibility.”

Those are all possibilities. But the only ones that are SF-specific (rather than applying equally to the neighboring counties) are ## 1, 4, and 5. And I’ve never seen any evidence to support these hypotheses — they are really just speculation. Regardless, we’ll see how it all plays out — no settling this debate until then.

“Seriously, anonn, all you ever do on this site is mock others. Why are you so pathetic? That’s not a rhetorical question. I’m really curious where it comes from.”

You don’t even know the difference between mockery and debate, “anon.” I used his own language to show he argued against his own point, and you called it mockery. You’re plainly stupid, “anon.” Want to talk about pathetic? You’ve said the same thing 20 times in a row now.

“I recall fluj positing that “the internet” made the SF market different from its neighboring counties, and that was quickly shown to be nonsense”

Oh, you mean the point that Noe Valley and a few otehr southern neighborhoods have shown a very strong gentrification thrust over the last five or six years? And their proximity to southbound freeways noted? Internet, Web 2.0, and tech jobs prevalence in the SF workforce correlated?

Is that what you meant? Was it truly so quickly shown as “nonsense” ?

Really Trip. Out of everybody on here you are probably the least fair. I think you’re playing some sort of part, actually. Don’t quite get it. But always the big dismissive language that overreaches the argument, and you tell us you’re a lawyer. It doesn’t add up.

anonn, look up the definitions of debate and mockery (it’s obvious you don’t know them). Then come back and explain your point. By the way, the southern districts have seen the biggest crash. So much for your latest “debate” point.

“Look up the definitions ….”

Childish. Using someone else’s language is debate tactics 101. You wouldn’t know that.

“By the way, the southern districts have seen the biggest crash.”

Wrong. The southeastern quadrant D 10 has, sure. That’s not what I was referring to with “Noe Valley,” and gentrification ..

Thanks for saying something other than your tired refrain. It shed some light on yourself. You really are just a knee jerk anonymous hater and not one of these other haters in disguise who at least attempt to pick up some knowledge here and there.

I agree, all the wealthy neighborhoods in the Bay Area (and throughout the country) have held up better so far. In fact, they are going the route of the more typical real estate cycle — which in the past has been a moderate decline, followed by at least five years of below inflationary (usually stagnant) home price gains.

Where’s a banker when you need one?

Or better yet, a banking analyst?

I’ve seen the apparent “shadow inventory” discussed here & there for several months. I’m instinctively cynical with two thoughts.

If you look at the first comment after the story, it reads:

So the very banks that issued the toxic loans are now going to create a housing shortage in order to drive up the value of their inventory.

The idea that banks are strategically withholding inventory so as not to overwhelm the market is ludicrous to me. It might make sense if a single bank owned all the REOs in a specific region, and thereby could unilaterally impact the market for foreclosures. But there are plenty of bagholding creditors in each neighborhood & region to dilute any one creditor this pricing power.

Each of these individual creditors (e.g., among the owners of the foreclosures I have reviewed on line are Countrywide, Deutsche Bank, HSBC, Wells, etc…) have every incentive to beat its competition to market with distress sales. I don’t believe banks are engaged in a coordinated “controlled release” of foreclosure inventory in an effort to prop the market, mainly because the incentives to do otherwise are too great.

So, let’s dismiss this idea.

The reason I am curious about the presence here of a banking analyst is that the rules governing the pricing of bank assets on the balance sheet are particular & esoteric. We all (err, or at least the pathetic among us who take interest in such things…) just witnessed the hulabaloo about FASB reiterating its recommendations for the “mark to market” of securities for which normal transaction markets have gone temporarily (“*cough* *cough*”) illiquid. (“Build a convenient pricing model, fellas! Congress wants it so!”)

What I am wondering from this is whether there is some ability for banks to carry a foreclosure at a historic value until it is subsequently resold?

For example, let’s say Joe & Judy Bubbletoppers of Vallejo, CA “bought” a $1,000,000 house with a 100% 2/28 IO ARM loan in June 2006. Recast comes in June 2008, and they can no longer make payment, so, eventually, it gets resold back to the bank on the busy courthouse steps for the balance of the loan for $1 million.

Now, bank has a “$1 million” property on their books, right? And it is the other side of the ledger to the $1 million loan outstanding.

In the absence of a resale, what should that bank carry that property for on its books? Without any specific schooling in the regulated esoterica of bank balance sheets, I could imagine there may be sufficient leeway to scribble “$1 million” in the ledger.

If so, there is no immediate recognition of a loss for the bank from the foreclosure.

Now, at some point, along comes Nick Knifecatcher who thinks that $750,000 is a swell price for this place, and he plonks down cash for it, and the banks turns over the keys. At that point, it would seem to me, the bank would be obligated to recognize the $250,000 loss on the property. But not necessarily before then.

If this is the case – that is, if banks can suspend recognition of losses on foreclosures until the property has moved permanently off its balance sheet in a sale – then one might expect banks to exhibit a predilection for retaining properties on their books above a certain value threshold.

Is this the case? I don’t know. Just thinking out loud, and trying to understand the incentives that I assume must be in place that encourage creditors to slow-walk sales and certain losses.

Oh brother….

Nothing like offering long-winded discourse in a likely-stale thread from yesterday that is consequently unlikely to be read or noticed by anyone….

Outside our faithful editor(s), of course…..

Problem is finding somebody to authoritatively answer the question. Many of us are still reading (catching up) but can’t really even guess what the accounting practice works.

I’ll ask one of my friends at KPMG, she works with High Tech companies buut might know somebody in banking.

Debtpocalypse – Not a bank analyst but it seems your scenario isn’t that likely. First, just scribbling $1 million on the ledger isn’t really a model for justifying the price. The banks still have auditors that will ask how they came up with that $1 million value and what the rational for it is. Also the bankers realize that if the house isn’t really worth $1 million but only $750,000 that they will eventually take a $250,000 loss. I mean if they are just going to make up a price I think that right now they would be just as likely to split the difference by writing it down a little each quarter so that they can offset their losses with the revenue from mortgages that are still paying.

I suspect that the banks with use the new relaxed rules to revalue the CMO bonds that actually owned some of these bad mortgages rather then using it directly on REO. It is easier to come up with some crazy model that tries to predict how much money that bond will ultimately collect. Remember mark to market is only difficult when there is an illiquid or frozen market, that is not the case for actual home sales, it might be a weak and declining market but transactions are still taking place and it is still possible to figure out what houses are selling for in different neighborhoods.

I call BS on Trip’s chart until it can be explained. WHAT do the numbers represent? I traced it back to the “source” which is http://blackstone-sanfrancisco.com/198.html and the only thing it says is “this table was developed from statistics compiled by the San Francisco Association or Realtors.”

“compiled by”???? OK, let’s see that raw data. Isn’t it posted somewhere for us to see? Who compiled it at SFAR, etc?

And what is it? Single Family homes? Condos? All residential? All anything? What is it????

And is January of each year really the best month to do year over year comparisons? How about a 3 month period each year. After all the CS numbers are every single month of every year.

By the way – I love the “all rights reserved” nonsense on the bottom of Blackstone’s site. If you got the data from the SFAR, what the F*** are your rights?

Also – how is it that commenters above noted that only D8 didn’t match CS? I see D7 and D6 are also no where near CS during the last 2 years. That is 3 of 10 districts not tracking, plus D9 and D2 falling, but no where near CS… so really half of the Districts are light years from CS.

Looks like shoddy work to me.

Finally – I love how everyone shat on Plank’s CBS report. This equally bad reporting is a virtual love fest.

Hangemhi, you need to go back to the original thread where these data and this chart were discussed before you get all indignant. I noted precisely the problems in the data and methodology that you now point out. And I added that this was an apples-and-oranges exercise as the Blackstone and CSI data are derived two very different ways. There was full disclosure. And I noted that I just haven’t seen anything better or more robust so we need to work with what we have. And then gumby posted the results for all too see. I invite anyone with better data (someone with full MLS access, e.g., like you) to give us something more robust to work with.

FWIW, I notice that over on thefronsteps, there is a somewhat similar analysis showing that — using medians — D3 and D10 have performed right in line with the “core” SF districts (all but D3 and D10). Again, anyone is free to provide better data or a different analysis. And I guess anyone is free to simply say “wrong” with nothing more. That is a lot easier.