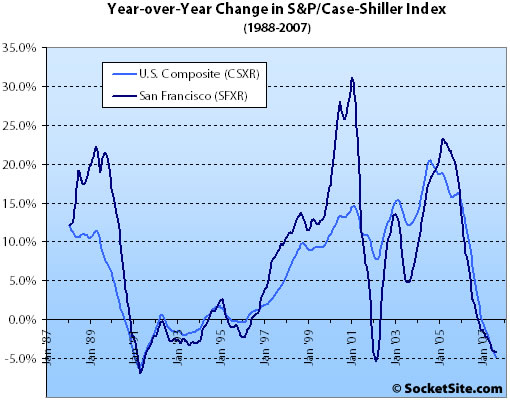

According to the September 2007 S&P/Case-Shiller Home Price Index (pdf), single-family home prices in the San Francisco MSA slipped 4.6% year-over-year and fell 0.8% from August ’07 to September ‘07. For the broader 10-City composite (CSXR), year-over-year price growth is down 5.5% (down 0.9% from August).

While Tampa remains the metro area with the largest annual decline, at -11.1%, Miami surpassed Detroit in September, reporting a decline of 10% over the past 12 months. Detroit and San Diego followed with -9.6% each.

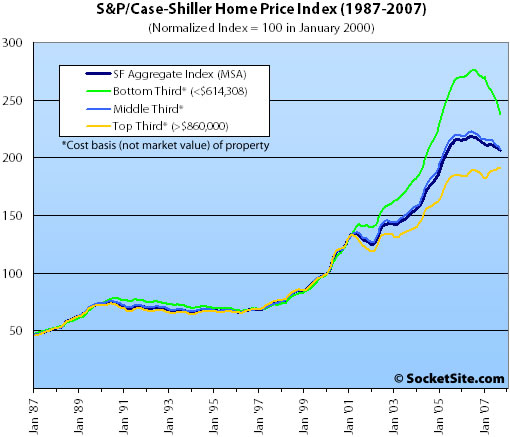

Prices also fell across all three price tiers for the San Francisco MSA.

The bottom third (under $614,308 at the time of acquisition) fell 2.4% from August to September (down 13.2% YOY); the middle third fell 0.9% from August to September (down 5.6% YOY); and the top third (over $860,000 at the time of acquisition) fell 0.3% from August to September (up 1.4% YOY).

The standard SocketSite S&P/Case-Shiller footnote: The HPI only tracks single-family homes (not condominiums which represent half the transactions in San Francisco), is imperfect in factoring out changes in property values due to improvements versus actual market appreciation (although they try their best), and includes San Francisco, San Mateo, Marin, Contra Costa, and Alameda in the “San Francisco” index (i.e., the greater MSA).

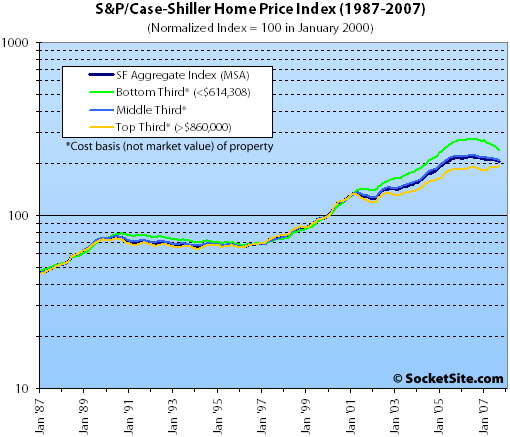

UPDATE: And by request (or at least an appropriate amount of taunting), the San Francisco Home Price Index (HPI) tiers plotted logarithmically:

∙ U.S. National Home Price Index Posts a Record Annual Decline (pdf) [S&P]

∙ August S&P/Case-Shiller HPI: San Francisco MSA Falls (But Less) [SocketSite]

∙ S&P/Case-Shiller Home Price Index For San Francisco By Price Tier [SocketSite]

I can’t figure out why anyone is buying right now. Its very easy to see that we are at the beginning of a downturn that will be at least as bad as the one that occurred in the early nineties. Rent now, buy in 3 – 5 years. Buy low, sell high as they say.

Are you missing the left hand scale on the second picture. Otherwise it’s just a bunch of random colored lines peaking and valleying.

@eddy: where’s the valley? All I see is a big green peak that’d headed nowhere but straight down.

I’m doubtful that that green peak represents much of SF itself. For that, I would look more to the yellow line.

Considering that the chart includes areas other than SF and excludes condos, the top tier (surely the vast majority of SF is in this tier) increasing 1.4% YOY is mighty impressive, considering the gloomy media reports. Any method you use to draw a trendline for the top tier would show an undeniably upwardly sloping line.

It just goes to show that if 5,000 people think a property is overpriced and one person buys it at list price, the people who don’t buy it are totally irrelevant.

Great point, anon. Guess it also goes to show that if there are 1,500 bloated properties out there for the 5,000 potential buyers, and one person buys at list, there are still 1,499 overpriced properties out there waiting to be reduced to incite the remaining 4,999 buyers to look.

Regarding the line colors, I just checked the MLS. Of the 1,441 residential properties listed in the city, 956 (or 66%) are priced below $860K (blue and green lines). 400 (or 28%) are listed below $615K. Yes, I realize the colors represent time of acquisition, but according to today’s MLS the proportions have not shifted significantly. Each line represents roughly 1/3 of the city’s inventory – the yellow line is not a vast majority.

From a relative newcomer to the SF scene, why do the 4 lines track so closely until 2001 and then show such stratification since? Is that a result of the tech bust in the early part of the decade, or is that representative of a fundamentals shift?

Any ideas?

06 – real estate will never fall, it always goes up

Q1’07 – Its all about location, location, location. Bay area is immune. Everyone has jobs, and they want to live in bay area.

Q3’07 – Again location, location, location. SF is immune. No more space in SF to build.

Q4′ 07 – SF top tier is immune.

Q1′ 08 – ?

Do these charts take inflation into account?

If not, wouldn’t the “valley” some people are predicting be minimized by inflation? Gas in 1987 was under $1.00 after all…

Alex, adjusting for inflation would actually make the graph look worse. While inflation might keep nominal prices higher it would eat into real, or inflation adjusted prices.

here are graphs of the national case shiller index using nominal and inflation adjusted prices

Re “It just goes to show that if 5,000 people think a property is overpriced and one person buys it at list price, the people who don’t buy it are totally irrelevant.”

That’s true only until the one person who buys it at list price tries to sell….

One possible explanation for the reason they separate in 2001 is the beginning of the availability of exceedingly cheap money and the increasing laxness of underwriting standards in subprime, and other financing vehicles as well as the increasing prevalence of interest only loans starting at that time. If your money is cheap, you’re going to be able to pay more and therefore you bid up the price.

“That’s true only until the one person who buys it at list price tries to sell….”

Timely case in point:

https://socketsite.com/archives/2007/11/is_it_possible_that_priced_right_is_now_priced_below_wh.html

This one person paid $3.5M in 2006. Now on the market for $3.4M.

Just for fun, here are two additional Case Shiller graphs that were originally published in the New York Times. The first tracks home values, adjusted for inflation from 1890 to 2005. The second tracks the Case Shiller index from 1987 to June 30th 2007.

While some on here will take issue with the fact that these represent national trends and are not Bay Area or San Francisco specific, because “it’s different here”, it has been repeatedly discussed that the San Francisco data, overall, follows the national trends so this should give you an idea of where housing has been and from that an indication of where it might go here in the Bay Area.

Irrational Exuberance, the lines diverge in 2001 because that’s when the suicide loans first hit the market. Rich people were too smart to fall for teaser rates so they show a natural drop in 2001, along with the economy. Poor people, for some reason, gobbled them up ravenously.

@irrational

That’s a result of the graphing scale. Notice that 1 unit of y axis covers a 100% increase from 50 to 100 but then it takes 2 units to cover 100-200 and 3 units to cover 150-300? On a log scale the price tiers wouldn’t wander so far from each other

The way it’s indexed also increases the apparent volatility in the upper end of the graph. The increase from ’87-90 only traces halfway from one y axis grid line to the next but a comparable percentage increase in later years traces through multiple grid lines.

Bad economist! No mean regression for you!

vox, whatever graph you use, the price for the lower tier doubled from 2001 to 2007, and increased only 50% for the top tier during the same period.

irrational, the buyers for the lower tier is totally different from higher tier. The higher tier buyers are normally well educated, with high income and manage their finance well. The understand oppotunity costs and do not buy something (whether stocks or RE) just because the rest of the population is doing that.

One can easily argue that the good houses are under priced and will continue to appreciate from the chart.

And I will even argue that when the three tiers meet, that’s when the market (as a whole) bottoms.

” is imperfect in factoring out changes in property values due to improvements”

I want to comment on this.

People seem to only consider the changes in property value due to improvements, but forget that the structure itself depreciates as it ages.

A property really has two components – the lot, which stays the same unless we have some natural disaster like earthquake, mudslide or flooding, and the structure.

When a structure is build, it has a value. Without maintainance, the structure will age and eventually (over 40 or 50 years) become unlivable, and has zero value.

Some owners will do regular maintainance. However, most likely, you remodel every 10 to 15 years to bring the property back to its prime.

So, even though a portion of the properties increase in value when they get remodeled, most of them lose value gradually when they age. In a normal market, they cancel out each other.

If remodeling activities are higher than normal, it will push the curve up. I can see that was the case in 2005 when home improvement was a national passtime.

However, if remodeling activities are low, then the aging depreciation will drag down the price too. I am sure that’s happening to some extend right now.

With enough data, over years, one can even pinpoint how much of the price change is caused by remodeling vs aging, and how much is real appreciation/depreciation.

“…the people who don’t buy it are totally irrelevant.”

Not neccessarily. They may not be irrelevant because if some of the people that don’t buy are people that tried to buy it, they would cause the price to get bidded up. If all of them were completely uninterested then that would be relevant as well because there would not be anyone competing for the property and putting upward pressure on the price.

Editor,

What service! I’ll be back to taunt more often.

“It just goes to show that if 5,000 people think a property is overpriced and one person buys it at list price, the people who don’t buy it are totally irrelevant.”

wow, you couldn’t be more wrong. if the 5k people who don’t buy think the price is too high, they won’t buy another comparably priced house in the neighborhood either. That will drive down the prices (as we are seeing today). So now the one moron that did buy will lose a great deal of money if he ever sells. Thus, these people are totally relevant.

My guess is that you’re a realtor… These 5k are even more relevant to you ’cause that’s commission you won’t be getting.

Looks like the Bay Area’s de facto “affordable housing” program of sending folks to the outer reaches of Contra Costa, Alameda, and wherever else BART goes may be blowing up in our proverbial faces … stay tuned for more socioeconomic stratification.

Just a few eyeball patterns that I think I see… (that probably have no real value except that they’re pretty!)

1. I find it interesting that in the first chart, YOY changes for the SF metro area seem to oscillate much more dramatically than the US Composite changes… (higher highs, lower lows) will this relationship hold?

2. thus far an argument can be made that the top third is still outperforming the middle and lower thirds… and is still going up YOY. I don’t like extrapolating one month’s worth of data to call this a “down” market for the top third yet.

regardless… interesting…

but as we’ve said before, housing downturns take YEARS to play out. I doubt we’ll know how SF will turn out for another 3 years or so… it’s similar to the downturn of the late 80’s early 90’s if memory serves…

besides, the credit crunch has just begun… each day brings more “news”. Today it was Citibank dealing with Arabs presumably to stay afloat (not a good thing), Freddie Mac axing its dividend (again not good) and Wells Fargo getting ready to tighten their lending and sell 11 billion of loans as well as probalby writing off a billion…

thus, if you are purchasing soon get your financial house in order… loans will be available in the future, but you MAY need to pay more for them, and you will FOR SURE need to have a rock solid financial status!

The three tranches seem to be converging. I wonder whether they will go back into lockstep at that point?

Buyers who try and time the market often get left behind. People who are buying now put a great value on owning their home.(PS these graphs are boring).

odd. I find them riveting.

Is it perhaps that they are saying things that you don’t want to hear?

I agree, when these 3 tiers converge, which seem like in 2 years time, I think the market resumes it’s upward bias.

One can indeed argue that the upper end is undervalued, and has plenty of room for catch up based on these charts as well.

In fact, if you’re an upper end buyer moving here from NYC, London, HK, Paris, Singapore etc.. you’ll be so shocked by how cheap SF is.

I’m personally interested how the yellow/blue lines hold up in a recession — a real one that scares rich people and puts the light blue line (high income, minimal assets) out of work.

These latter folks keep threatening to pounce on any housing weakness with their nest eggs (perfectly timed, of course, when calculations work out just right), but if their job is uncertain, I bet they don’t pull the trigger…

We’ll see!

“I bet they don’t pull the trigger…”

Very valid insight. When the time comes it’s going to take courage to trade the security of having years of living expenses in liquid assets for a dwelling and a mortgage.

“Today it was Citibank dealing with Arabs presumably to stay afloat (not a good thing)”

Saudi Prince Alwaleed bin Talal is the largest holder of Citi stock so it makes complete sense that he would reach out to his friends in Abu Dhabi.

“Buyers who try and time the market often get left behind.”

I doubt anyone will be left behind in this market. If you had the same theory in 1895 you would have had to wait until 2005 to get your inflation adjusted dollars back (according to the graphs linked from badlydrawbear).

“Saudi Prince Alwaleed bin Talal is the largest holder of Citi stock so it makes complete sense that he would reach out to his friends in Abu Dhabi.”

Peter: no doubt. My issue isn’t that they chose non-Americans as buyers… it’s that they had to do this at all.

Clearly, Citibank is running into trouble either with liquidity or more likely reserve ratio requirements. Not good…

Do you think it was a good thing that Citibank needed to raise cash so badly that they had to sell 4.9% of the company? Or that they didn’t do it by simply offering common stock?

reminds me of another “great deal” that we recently saw between BofA and Countrywide…

Analyzing the terms of the deal would take 10 years of high level business accounting experience… so I’m not up to the task of who got the better deal here, citi or Abu Dhabi. At first glance a convertible stock yielding 11% annually seems a steep price… but then it has forced conversion at a set price in 2010-2011… thus a lot will depend on what Citi’s stock does in the meantime.

@ex-SFer

“I find it interesting that in the first chart, YOY changes for the SF metro area seem to oscillate much more dramatically than the US Composite changes… (higher highs, lower lows) will this relationship hold?”

The smaller sample is likely to be noisier.

The other interesting consideration is in the methodology. This index tries to massage away price changes attributed to neglect or major renovation (as is ‘suspected’ in the methodology by comparatively large price swings). However, by trying to index only indentical paired sales, it’s going to throw out a lot of activity, shrink the sample, and add some noise.

interesting article from WSJ opinion

“san Francsico has lost population since 2000”

“There is a basic truth about the geography of young, educated people. They may first migrate to cities like New York, Los Angeles, Boston or San Francisco. But they tend to flee when they enter their child-rearing years. Family-friendly metropolitan regions have seen the biggest net gains of professionals, largely because they not only attract workers, but they also retain them through their 30s and 40s.”

http://www.opinionjournal.com/editorial/feature.html?id=110010911&ref=patrick.net

Economics and statistics put some people to sleep and turns others into Jimmy The Greek.

1895? or even 1985. I do not comprehend the message. Or the reference. If you bought in 1985 or 1895, held real estate in San Francisco and sold in 22 or 112 years later, that is a a bad investment? I’ll unplug my time machine now. No wonder I never took an economics class.

I can not hear a message from the graphs – like silent Bob, they don’t speak, they illustrate.

The graphs are boring. There are better ways to illustrate a point. No difference to me if anyone buys or sells now or not.

Those who buy in face of a recession, or with an ear towards talking illustations, are pehaps using additional criteria that is not exclusive to speculative economic gain. And does not appear on the graph. Does that make sense?

Sincerely, Miss West Carolina of the Graphs

P.S. Anyone have a map?

Population might be down since 2000’s peak. I thought we already talked about how it is up in the last few years, tho?

It doesn’t makes sense. Who lived in South Beach in 2000? Nowadays thousands live in South Beach.

Fluj the Census Skeptic.

I wouldn’t be surprised if the population is down. One of my pervious landlords raised 3 kids in this 1000 sqft 2/1 house. Would anyone raise a family today in that house? Maybe 1 kid, but definitely not more.

Since majority of the housing units in the city are small, I am not surprised if new parents move to the suburbs.

So, it makes sense to me, that the # households increased, average residents/household decreased, and the overall population decreased.

Judging simply by my anecdotal experience, I wouldn’t be surprised if the population is still below what it was in 2000. Rental occupancy rate in ’99-’00 was over 98%, and now I think it’s somewhere around 95% (can’t find current data anywhere) and rising.

Since more than 60% of housing is rental property, and there really hasn’t been much new rental property development to speak of in the past 5 years, that 3-4% drop in occupancy rate means a lot of people.

Fluj, I could see your perspective being different because you spend so much time dealing with the purchasing market. I’d imagine the number of owners in the city has increased by a lot (esp with the increased amount of inventory in places like SOMA, South Beach, etc. as you mentioned). But since so much of the population is renters, a minor decline in rental population will probably mean more than a major increase in owners.

We’ve probably recovered, but it’s either just barely under or just barely over.

The picture of the graph in reference (linked by badlydrawbear) is very simple. If you bought a house (US in general, NOT SF) in 1895 you paid $125,000 in todays money (inflation adjusted).

According to the graph, that same general everyday home would not have sold for $125,000 (inflation adjusted dollars) again until roughly 2002.

So even though you actually paid $5000 in 1895 and sold it for $200,000 in 2002 you did not ‘make’ any money. You broke even, just as if you had taken the money and put it in a bank account with interest equal to inflation.

Peter,

You are cherry picking a point on the chart there by chosing 1895. If you had bought in 1890 when the chart starts (rather then the first peak which you picked) you would have made money if you sold any time after 1950.

The chart does a good job of throwing in the information that the real cost of building homes decreased in the first part of the century and that home prices didn’t really start to increase until the post-WWII boom.

It also shows that there was a huge spike in housing prices in the last decade.

Peter is cherry-picking, but I think he is making the broader point that buying at a market peak can have a huge impact on returns even on the very long term compared with buying just a few years earlier or later. Realtors often claim that if you think long-term, it doesn’t really matter if you’re timing the market a little bit wrong. That just is not true. The returns illustrated by the 1890-2005 chart support pretty solidly an argument that those who bought in 2004 to 2006, the recent peak, very well might take a huge financial hit — even if they hold on for decades — and this could be even more stark when compared to buyers of comparable places a few years earlier or later.

That’s right, Trip. Rillion, I think most people would be shocked that there was ever a period of time where one could own a house and it would not appreciate one bit in over 100 years. The last ten years have fooled people into believing that owning a house is the key to wealth. It’s just not the case.

All over the world, the value of residential real estate has merely tracked inflation for centuries.

The reason why people have made money in real estate is leverage and interest rate deductions, not because of 10% annual gains. When you add leverage to an investment, you greatly increase the risk, but you also increase the returns.

Example, 100k down payment on a $1 mill house. House goes up 5%, you just netted a 50% return on your investment. If you can get a mortgage that pretty much matches your rent with the interest deduction, e.g. a $3100 mortgage or so when you’ve paid $2k in rent before, then it’s almost a no brainer to buy because even a 2% annual increase will be a great return on your down payment.

But if you’re doubling your monthly payment or more, as has been the case for some time, and your house is only going up 2% a year. You are throwing money down the toilet.

I have to disagree timkell. Owning a house was a way to benefit from the government’s policy of endless inflation.

If you bought a house with a 30-year fixed then it’s value was guaranteed to steadily increase with inflation. At the same time inflation would increase your salary making your fixed payment a smaller fraction of your take home with time. At the end of 30 years you had a paid for asset for an outlay that was not much more than what you would have paid in rent anyway.

Since the end of WWII a house has been an excellent investment for the middle class. And once the coming correction was removed the speculative premium from house prices it will be again.

Of course, without inflation, it’s just a depreciating asset and a cost. But that’s another discussion.

Diemos, I don’t think we disagree. I think we’re saying the same thing.

I said it a little differently, but yeah, if you can get yourself a mortgage+insurance+property tax that costs the same as your rent after tax deductions, you’re psyched and it’s a good move.

A house is an excellent investment if it doesn’t cost you much more on a monthly basis than rent and all you have to do is come up with the downpayment nut. But in the last ten years people thought a house was a great investment no matter how much it costs above and beyond rent.

When it’s two to three times rent, in a normal market it’s not a good investment, plain and simple.

I have to say that I found badlydrawnbear’s chart of inflation-adjusted housing prices for the past 115 years mesmerizing. The FACT that you could buy a house in 1895 and not make any “real” dollars until sometime in the 1980s — almost a CENTURY later is utterly astonishing! And to think that our current house price peak is about 80% higher than the 1895 peak … its just mind-boggling. It could conceivably take TWO centuries before the average homebuyer makes any “real” money (after adjusting for inflation).

We’re sure lucky to live in San Francisco, where prices are most definitely not inflated, speculation doesn’t exist and most importantly, everyone wants to live here, which provides limitless support for appreciation of housing prices far in excess of inflation from now until eternity.

timkell/deimos — I think you are both correct (you actually are saying two different things, both correct).

Back on point, the time frame (100 years!!) is ridiculously long, and assumes someone is so stupid as not to default if things get intolerable.

In real life, you would buy “at the high”, suffer a crash, default, wait awhile, and walk back up to the table again when the prices are better (I’m oversimplifying, of course). People are already walking away from their debt very successfully. They’ll be back in a few years no questions asked to start again. They won’t bear the brunt of the loss, the holders of the paper will (and are).

In fact, someone who buys at the high, and is “smart enough” to default, then come back later, might actually do quite well over the long run! It might not sound fair, but this isn’t the playground, after all.

Meanwhile, the “hyper-savers” get screwed (they always have, always will). In the depression (mentioned because it’s covered in that ridiculously long time frame), we had a currency devaluation in 1933/34. The market is currently devaluing the dollar right now, and of course inflation, etc.

Maybe in real life, you wouldn’t buy at the “high”, suffer a crash, default, go bankrupt, then rebound a few years later. You might just get out a piece of paper and a pencil and write down the following numbers as they apply to your situation:

My rent: $3000/mo.

My cost to buy the apartment: $840,000 (based on August sales price of the one next door), or roughly $6000/mo PITI (before tax deductions).

Hmmmmm………

“People are already walking away from their debt very successfully.”

Yup. Durn that integrity. If I wasn’t burdened with that I could be making a lot of money by screwing over the system.

@Jimmy: When things are as far out-of-whack as they are in your situation, and given what appears to be happening right now, I quite agree; my point is one shouldn’t assume an individual is going to suffer the same long-term losses as implied by an aggregate graph. But what if your situation was 5k to 3k? 4.3k to 3k? Are you waiting for 3k/3k? Hard to know when to ring the bell…

Like it or not, “rags to riches” is kind of a staple of the American Story ™. Defaulting (intelligently) can be part of that story. Excessive saving is never rewarded, and sometimes punished! I don’t make the rules 😉

Disclaimer: I’ve never defaulted on any loan 🙂

“The FACT that you could buy a house in 1895 and not make any ‘real’ dollars until sometime in the 1980s — almost a CENTURY later is utterly astonishing!”

Just because the inflation-adjusted graph shows no change doesn’t mean no money was made, or that there was no value in buying. The graph index is at 110 in 1907 and is at 110 in 1997. A neighbor family bought their San Francisco house for $700 in 1907 and sold it for $340,000 in (around) 1997. Now, perhaps if they had rented, and invested that $700 in AT&T stock in 1907, they may have made more than $340,000 in 1997. But if they had invested the $700 in a company that went bankrupt during the Depression, and they were still renting in 1997, they might be out the $340,000, as well as the experiences of three generations of a family in that house.

@diemos — Let’s say someday you buy a house (10-20% down), and despite your best projections, the economy continues to falter, you lose your job, get a new one 9 months later that pays 2/3 as much (with a lame health plan), and you or a family member has a minor medical problem requiring recurring treatment. Your projections now tell you your remaining savings will be gone in 5 years, but if you rented (or moved away from SF), things would be fine.

Are you telling me you wouldn’t consider walking away from this loan, depspite your “integrity”? C’mon, friend, we all have our default point. Nobody’s mother teresa, not even mother teresa…

Jimmy, I think your estimate of 6K/mo is off for a 840K property (unless you found the greater fool that is going to loan you 100% of the purchase price)…Good luck…

Well dub dub, if I put 20% down then I should be able to sell if I get into trouble. But you’re right, at some point I’d walk away and take advantage of that legal option in extremis.

But I just can’t follow the example of my peers and treat these 100% neg-am loans as if they were monoply money. Blithely signing up for million dollar loans (cue Dr. Evil … one MILLION dollars) with the expectation that you’re rolling the dice with somebody else’s money and if it doesn’t work out, just walk away.

Through the magic of securitization the money for all these loans have been coming out of your defined benefit pension plan’s assets, your 401k bond fund, your money market fund. The middle class is going to be mighty upset when they finally realize that this bubble was created by spending their retirement money and when it collapses not only will their house value disappear but their retirement money will vanish with it.

“Jimmy, I think your estimate of 6K/mo is off for a 840K property (unless you found the greater fool that is going to loan you 100% of the purchase price)…Good luck…”

Craig, a 672k mortgage (20% down) with 7% interest would run about $4450 per month. Property tax would be $795 per month. If you only put 10% down the mortgage would be $5029 per month.

Remember HOA too because it’s probably not a detached home for $840k

$6k is not a stretch by any means when all costs are included.

Jimmy, $6000 before tax deduction sounds about right. What’s your tax bracket? I am guessing your after-tax cost is about $4000.

$4000 vs $3000 rent….I would rent.

If the after-tax cost is about $3500, I would consider.

Dan – Let me preface this with the fact that owning a home provides a sense of security and stability. I would have loved for my family to have owned a home in SF for such a long time and I would probably never want to sell it regardless.

BUT as far as pure financials go:

The DOW Jones Industrial average has returned an average of 7.4% from 1901 to 1999.

The average inflation rate from 1901 to 1999 was 3.2%.

$700 invested in 1901 in the DOW would now be worth $882,116.97.

(sources:http://www.moneychimp.com/articles/econ/inflation_calculator.htm and BLS statistics)

Sorry – in the above post I should have said $700 invested in 1901 in the DOW would be worth $882,116.97 in 1999. NOT today as I indicated.

It would NOW be worth $1,312,973.76.

“Rillion, I think most people would be shocked that there was ever a period of time where one could own a house and it would not appreciate one bit in over 100 years.”

I think the people that would be shocked by that fact would most likely be the same people that would consider a house to have appreciated if they bought it for $100,000 and a year later it was worth $103,000 while there was 3% inflation. In my experience most people don’t calculate their finances and their wealth in real dollars but in nominal dollars.

I didn’t include HOAs in the $6000/mo number. I assumed a hypothetical 100% 30-year fixed at 6.5% which is $5300/mo. Your results may vary.

HOAs are about $380/mo, and I also didn’t factor in any insurance costs– I have no idea what that would be for a condo.

And to factor in the tax deduction properly, you have to consider the amount of principal repaid every year (and then consider that your after-tax payment is necessarily going to rise every year).

In the end, I don’t particularly like my view of a back alley although the pigeons nesting there are friendly enough, so I guess I’ll have to content myself with not signing up to pay double for what I live in now….

And since I moved here in late 2006, there’s no reasonable way I could have taken advantage of all that appreciation on the way up to $840k. Although I’m sure the owner must be delighted with their good fortune! (But you wouldn’t know it from their crappy attitude — what is it with landlords anyway? Seems that business makes you cranky all the time.)

peter,

It is simply not possible to buy DOW stocks in 1900 and hold it for XX years. There was no index fund then, and if you buy seperate stocks, do you know how many times they have changed the stocks in DOW?

The stock market return is based on winners, because if you really bought the original DOW 12 in 1900 and hold for 100 years, you probably will lose your shirts.

Second, never use “average return”. That number is fake. For example, if your first year return is 100%, but second year is -50%, what’s your average return? 25%. However, your have exactly the same money as you put in. Your annualized return is 0%.

To get a real sense of return on investment, you need to use annualized return.

DOW was 51 in 1900. Now it is about 13000. $700 in 1900 invested in DOW index (just to remember to sell and buy whenever DOW changes the stocks) is worth $180,000 today.

http://stockcharts.com/charts/historical/djia1900.html

John,

You are incorrect. This thread is worn out though so I will not explain. Do additional research if you are truly interested though.

Peter,

I call your bluff.