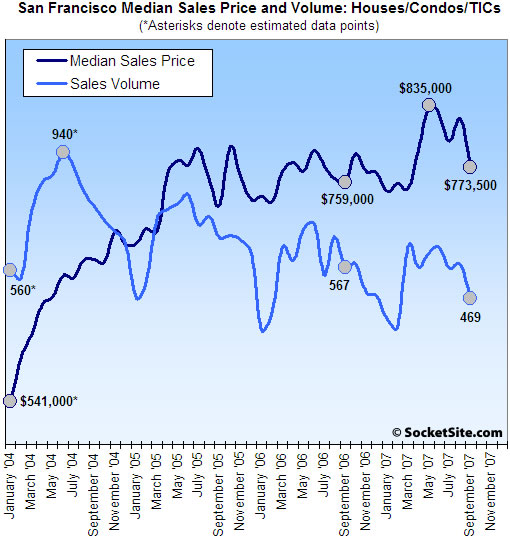

According to DataQuick, sales volume (i.e., demand) for existing homes in San Francisco fell 17.3% on a year-over-year basis last month (469 sales in September ’07 versus a revised 567 sales in September ’06) and fell 18.7% compared to the month prior (577 recorded sales in August ‘07). At the same time, the median sales price in September was $773,500, up 1.9% compared to a revised September ’06 ($759,000) but down 5.9% compared to the month prior. (And yes, we’re still thinking mix.)

For the greater Bay Area, sales volume in September was down 40.1% on a year-over-year basis (and no, that’s not a typo) and fell 31.3% from the month prior (5,014 recorded sales in September ’07 versus a revised 8,374 in September ’06 and 7,299 this past August). The recorded median sales price also fell from the month prior (4.6%), but was up a nominal 0.8% on a revised year-over-year basis.

The number of Bay Area homes purchased with jumbo mortgages dropped from 3,762 in August to 1,935 in September, a decline of 48.6 percent. A jumbo mortgage is a home loan for $417,000 or more. For loans below that threshold, the sales decline was 14.0 percent, from 2,675 in August to 2,301 in September. Historically, sales drop by about 10 percent from August to September.

Outside of San Francisco county, the smallest drop in year-over-year sales volume was recorded in Marin (down 32.5%) and the largest in Contra Costa (down 48.7%).

∙ Bay Area home sales plummet amid mortgage woes [DQNews]

There is something in these number for everyone, volume down based on access to jumbo financing but median price up… just!

Still picking March ’08 as the time when we will see clearest data of where the market is, but if you have to buy now, bargin hard!

March 08 is right around the corner. A few more 40% and 10% respective drops to go before you find the bottom IMO. Sellers don’t seem to be budging so as I’ve said before you probably aren’t going to see big price drops here in San Francisco, but demand is going to (continue to) plummet and certain sellers will fall into financial trouble if they can’t move a property to cover their shorts (literally and figuratively). Ok bad pun, but you get the idea.

How did this impact the CME’s futures for the bay area? I’m too lazy to look it up.

Personally, I’d buy now if you plan on being here for at least 10 years; or just wait until late 08, or sometime in 09 if you’re looking to get the most for your money and can continue renting.

E.

Hmm – I agree that mix might have impacted these numbers….but likely for the worse. With the lack of availability for jumbo financing and higher rates, the mix of mortgages likely shifted more heavily into conforming products last month. And before flaming me, look at the article posted today in the online version of the Contra Costa times. It says “if the jumbo-financed portion of the market had remained stable, last month’s median would have been $654,000”. That compares to last year’s median of $620K by the way. For the record, I think the drop in Jumbo availability should put some downward pressure on prices (even in SF), but it seems like this story is relatively positive news for the San Francisco market (compared to other places in California).

““if the jumbo-financed portion of the market had remained stable, last month’s median would have been $654,000”

It’s kind of a meaningless statement though. Stable from when, exactly? And what’s the betting that the percentage of jumbos actually _increased_ earlier this year due to the earlier collpase of sub-prime funding?

I’ll also note that Dataquick chose not to do a similar “if the sub-prime financed portion of the market had remained stable, last month’s median would have been xxx” analysis earlier in the year. I wonder why?

The chart indicates a peak in July and a trough in March. Based on where we are at in this trough in the making I’d say the March 08 stats aren’t going to look to pretty from the current trend.

The DQ counts, according to the article, are for “new and resale homes and condos” and for San Francisco were 469 for Sep07, 567 for Sep06, and 577 for Aug07. The listed sales volume for these periods were 345 for Sep07, 486 for Sep06, and 483 for Aug07. So this implies that the non-listed sales counts are 124 for Sep07, 81 for Sep06, and 94 for Aug07. So DQ would have reported a larger decline for September if not for this big increase in non-listed sales.

Where does DQ obtain these non-listed sales figures? Are these recorded sales? Are they subject to revision?

Good question…I often see pocket listings on CL and other sites. Enough of these may help explain why inventory seems higher than the MLS numbers convey. But I guess if DQ pulls County recorder data, everything shows up there when the deed is recorded?…just a guess.

“It’s kind of a meaningless statement though. Stable from when, exactly? And what’s the betting that the percentage of jumbos actually _increased_ earlier this year due to the earlier collpase of sub-prime funding?”

Amen Corner – I understand your point, but I disagree. The percentage of jumbos is being compared to September of last year just like the median price. If you were to adjust for this change in mix (out of jumbos), then prices would have been $654K this month. This is effectively the same type of mix analysis that a lot of folks on this board have been using to explain the increase in prices over the last several months. It’s just that this time it suggests that prices would have actually been higher. I certainly don’t have a crystal ball or profess to know what this market is really doing, and things certainly aren’t very rosy. Mix shifts however can and do work both ways, and there still aren’t any really non-anecdotal signs of a serious downturn in SF real estate prices.

Lance, you may be right, but I see nothing in DQ release to back your assertion. The relevant comment is

“The median price paid for a Bay Area home was $625,000 last month, down 4.6 percent from $655,000 in August, and up 0.8 percent from $620,000 for September last year. If the jumbo-financed portion of the market had remained stable, last month’s median would have been $654,000.”

One could just as easily interpret this as “stability” from August as opposed to September last year.

A couple comments from looking at the graph…

It’s clear the moving average for sales volume is trending down. Since 2004, every successive September has had decreasing sales volume.

Meanwhile, the median is still moving up, but unlike the steadily decreasing seasonal fluctuations we see in sales volume, the median seems to be encountering greater volatility.

Again, I will propose that this can only further depress sales volume. Who wants to buy a house and discover waiting another week or two would have saved them $100k? While not all sellers have to sell, some do, and when their backs are against the wall they will use the only option available to them to move, and that’s price reductions. There’s no doubt that price reductions are on the way, even in SF, the only questions, is how much, and for how long.

“Sales Volume” is demand? Doesn’t sales volume just mean the number of properties sold?

I always thought that the quantity sold and the sale price were found by the interaction of demand AND supply. But what do I know, I’m just an economist.

I know that many of you have said that prices in the prime areas won’t drop, but what will happen if inventory increases significantly? For instance, I drove by 29th ave. between Lake and California yesterday in the Sea Cliff and I swear I saw at least four or five homes for sale all on the same block.

Here’s an idea for what drives demand: availability of credit coupled with historical increases in asset prices.

Those are the fundamentals we should be looking at.

Who really cares about sales volumes or the number of properties for sale? If they aren’t going up in value, demand is going to be weak. If they are going up in value, demand is going to be strong, provided credit is available for speculation.

That, in a nutshell, is the supply and demand equation as it pertains to housing.

Jimbob, I think your point is perfectly valid and explains the high demand of recent years — a perception of rising values coupled with ample credit available to anyone with a pulse. Now we have the near-universal agreement that values in SF will be lower or flat at best in the next couple of years, and credit has dried up substantially. All that will certainly lower demand — indeed, to the extent these factors influence demand it has probably completely flattened the demand curve.

This, of course, does not tell the whole story with respect to housing (compared to, say, stocks or commodities — pure investments). Demand is also driven by people who simply want to buy a home to live in and are able to do so. That aspect of the demand curve remains, although it will be less steep than in the recent past as even those who can and want to buy increasingly realize that it is probably smart to hold off given that the market is softening.

I’ve said it before and I think these numbers support it: what we have currently is a stand-off between buyers and sellers. Who will blink first?

Well, a lot of the buyers who were in active in the market for the last few years are gone. Flippers are gone. Those who do not have substantial down payments, documented high incomes, and high credit scores are gone. It’s true that some would-be sellers will hold off because they think the market might turn back up at some point (which it will, of course, but that took about six years last time we saw this in the 90s). But many sellers have no choice — they’re moving, can’t afford their place for 100 different reasons, etc. Others will jump in now simply because they can see that even though we’re off of the highs they’ll still sell for more now than they would if they wait two years. I don’t think you’d see these numbers plummeting if buyers were blinking. They’re not going to.

I think missionite nailed it. The SF market, for now, is still whistling past the graveyard. But last I checked, the laws of physics still applied here, regardless of how “special” we might think we are….which means the laws of economics do as well.

It seems that part of the editorial mission of many on this site is precisly to persuade would-be buyers not to blink . . . not yet (maybe in March 08 or some later date). And that’s fine, that’s fair. Some people think they can time the market, and maybe they can. I have no argument with that. But IMOH what often gets overlooked here is the seller/supply side of the market equation. No evidence in these numbers that would-be sellers are blinking . . . yet (maybe March 08 or some later date).

Are there sellers who will have to sell because their financial circumstances change, they are moving (or they died)? Of course. Will we see must-sales in high enough numbers to tip the pricing subtantially? Don’t know. Not there yet.

One reason SF had higher sales volumes in recent years is that homeowners looked around at what their neighbors were being paid for their homes and said to themselves: Why not me? The market, in effect, made them want to move. However, the opportunistic SF seller may be largely absent from the market now, contributing to low sales volume and lower-than-expected inventories.

sanfrantim – I think the argument you make may go against your point. If the opportunistic sellers are gone, that means most current owners bought in the last 2-3 years. Which means they paid inflated prices and most likely used toxic loans they can’t afford over the long-term (the highest mortgage default frequencies are currently the ’06 and ’07 vintages, with the ’05s not too far behind).

The only way for the SF market to hold steady is the opposite – if most current owners bought before ’04 using more traditional loans. Then they would have enough equity cushion to ride out a cycle, even if prices dropped 20%, and would not have to worry about payment or rate adjustments.

Good point, sanfrantim. But as a buyer who’s been “on the sidelines” for the last 6 months, I’m not sure it really matters all that much to me what sellers do. I’ve already moved on, putting my 20% downpayment to work in other investment vehicles, and I’m expecting it’ll be at least 6-12 months before that cash becomes available again.

Any bets on whether inventory will be higher this winter than last year? I feel like that will be the true test of whether SF is starting to tip or not. If the majority of current sellers can afford to pull their listings in December and try again in the spring, then I think we’re in for another year of standoff.

I always wonder how many sellers can afford to lower the price. If you bought in 2005 with 5% down on an IO loan, or perhaps you bought earlier and HELOC’d out your appreciation, then after commission you could be writing a big check to sell at even a 5% discount.

Dude, i don’t think you really meant to suggest that most SF owners bought in the past 2-3 years. think about it.

For those that did, and paid top dollar, they are not likely to sell anytime soon – unless they have to.

Anon, I have no reason to doubt you that you have made a prudent decision by taking yourself out of the market. But those who are still currently looking to buy obviously do care what owners/sellers choose to do.

No, I was definitely not suggesting that – I thought that’s what you meant when you said the opportunistic sellers were gone?

Regardless, the foreclosures/defaults are starting to seep into San Francisco proper now. V-Valley and Excelsior are hardest hit so far, but NODs are increasing across the board, even in the Marina. So even those currently looking to buy may be well served to wait just a few more months, to see if it’s a fluke or if national trends affect us, too.

dude, that may not be too far off the advice I have been giving my friends who are in the market for a SF home: “now is a good time to be looking and gathering information. there may be a further shake-out coming, so don’t bid high on something you really don’t love. if you see something you do love, and can afford, and plan to live there at least 5 years, make an offer.”

Who will blink first?

They guy who converted the 10 unit building to TICs and gave it the pergranteel treatment. He wants out and there is no going back…

Anecdotally, we are seeing more TICs on this side of the Bay. Dude, do you post on the HBB?

Sanfrantim–I offered my example to point out that, for the next 6-12 months, I (and perhaps other “highly qualified” buyers) are essentially “locked out” of buying real estate. If you are a student of game theory, you’ll know that this is an important move in a game of chicken.

For those who could buy but are choosing to sit on the sidelines, I am curious what date they have in their head for when they will begin to look to get back in the market. Spring 08 or 2009? At least in my circle, there are many people who could afford to buy, even at today’s bubbly prices, but are choosing to rent and wait. These “waiters” could keep prices from going off the cliff that some would hope for, though I think the outer neighborhoods are going to suffer more than areas such as 94123.

“Dude, do you post on the HBB?”

I used to, but not much anymore, and never on Patrick (although I’ve seen your posts there). SocketSite is more fun because there are still a ton of bulls here…less fun at the other places, where everybody thinks the same way!

ahem…sorry…forgot to add that SocketSite is a MUCH better site in general since it’s specific to San Francisco and features a diverse forum of topics, from economics to architechture to local politics.

gfw is right. Sales volume is definitely not demand… I think it is hard for many to believe but volume is down because inventory is down, inventory is down because it is selling quickly. Equilibrium will set in, but it hasn’t as yet. Ripley’s ……. “SF remains a Seller’s market”.

we are special. remember that little company called google? what about vmware? new millionaires by the day at each with each new 10 point increase in stock.

@anon94123: I’m in this same position. But regarding waiting, I don’t think it’s so much of a timing issue, but more of a price/value issue. Not sure about your friends, but I know the areas I like and know what I want to pay. What I’ve calculated as an “equilibrium price” for the market, if you will, based on incomes and pre-bubble appreciation.

As one example, when I can buy in 94122 for around $350-$400/sq. ft. for a mild fixer, count me in. This is basically 2001/2002 pricing – I don’t think I’m insane thinking prices in Sunset may fall that far. But agreed that we won’t see that type of drop in 94123…

James perhaps you missed the post just two days ago, but inventory is not down, at least nowhere near as down as sales volume is. Listed inventory is off 1.3% from last year, and if we factor in what appears to be a surge of pocket listings then I suspect inventory is actually up YOY, while sales volume is continuing to decrease.

If inventory and prices are relatively flat compared to years past, and volume is down, what does that tell you about demand? Anything?

Granted, I’m not an economist, but as a small business owner with a degree in common sense, if sales are down industry wide and everything else is equal (quality, supply, marketing, competition) then I’m probably going to start cutting prices. I don’t need a degree to figure that one out.

but we are dealing with the most emotional asset their ever was or will be, home.

all rules are off until they cannot be ignored, and the fact that we are in a 7×7 piece of land that literally 1000’s of people would love to own in, now extract all the undesirable neighborhoods to live in, and you have the making of a sustained bubble no matter what happens in the rest of the world.

“If inventory and prices are relatively flat compared to years past, and volume is down, what does that tell you about demand? Anything?”

If inventory and prices are relatively flat compared to years past, and volume is down, what does that tell you about supply? Anything?”

@anon94123 & Dude: Much the same situation and evaluation happening here. I’m a renter, by choice, watching the market closely. I have the down payment and salary to purchase, but don’t see the -value- I’m looking for, which basically amounts to ~1300sqft 2/2 in a ‘desirable’ neighborhood w/ parking and some small outdoor space (patio, roof deck, something) for

“In the mean time, I’m more than happy sit and wait by renting, put another $6k+ a month into savings/retirement and have my nest egg outperform inflation+YOY housing appreciation on relatively low risk investments”

I agree totally and the money I have been able to set aside during renting has also performed better than housing. The taxes and association dues on the condo I am renting almost equal what I pay the owner of my unit in rent.

I heard a comment recently that pretty much points to how insane the last couple of years have been. “You know it is a bad time to buy, when the realtor is driving the $100,000 car instead of you.”

Again, this is not surprising. August contained all the bad news. September closings, therefore, were down. October will be up from September. Blah blah blah.

Fluj – I’m amazed at how quickly you dismiss a 40% drop in sales. Surprising or not, that’s a huge hit. October sales might be up from September, but how will they look compared to last few Octobers?

Comparing Septembers between an avowed peak year and a late summer ’07 rife with bad news? I’m surprised it was only 40 percent, to be honest with you. The market is cruising along. It simply is coarsing along at 70 mph these days. Maybe not 100 mph, but whatever. It’s still over the speed limit in most states.

Last October saw 294 sales for single family homes. As of today there are 94 October sales for SFRs. By Monday there will probably be another 30-40 slotted in … for whatever reason, weekends are when realtors often seem to update their listings. I’d say we’re not far off the pace, actually. We’ll see.

Gloom and doom!

October sales volumes and prices will bump back, no doubt.

And anyone who says that they made more money on stocks than real estate in the last few years is incredibly lucky in their stock picks. In general a no or extremely low money down highly leveraged mortgage over the last few years would have generated a multiple x bigger gain than investing in the markets. Better and easier to earn 25% on someone elses million than 100% on my $100k.

If you were lucky enough to have bought a house before 2004, and then sold between 2005/2006 at the height of the market, then yes, you will have made a lot more $$$ in real estate than other investments. (Unfortunately, thousands of people who bought within the last 2 years aren’t so lucky). In any case, stocks yield higher gains IN THE LONG RUN.

Stocks yield more in the long run than real estate? Why is that hard and fast? No. It isn’t. It’s case by case. Come on now.

Here is a common example. What about somebody who invested 80K on the South Slope of Bernal Heights five years ago, as 20% down on a 400K house? I think if they sell today that 80K is worth way more than most stock portfolios. That 80K nets 500K in five years.

Economists from around the world have analyzed this countless times: historically, real estate is not a good investment. Returns usually follow inflation, maybe you beat inflation by a little bit, but that’s about it. Even over hundreds of years and in the nicest areas:

http://www.nytimes.com/2006/03/05/magazine/305tulips_shorto.1.html

Old article, I know, but still relevant. Amsterdam is also a “world class city” where they’re not making any more land.

There are analysts in that very article who disagree with Shiller’s irrational exuberance thesis and posit contrary opinions.

What about my example? It happened. It is not a thesis, it is a fact.

fluj, that piece was written over a year ago, before the stuff hit the fan and prices nationwide started to fall. As Schiller accurately predicted they would (for the 2nd time in a decade). Wonder how many of those analysts still disagree? Definitely not the guy at the Fed….

But you’re missing the point, so let me rephrase my comment. Show me some comparisons OUTSIDE of the bubble of 2000-present where, on a consistent basis, real returns from real estate outperform a balanced equity portfolio. Got any examples not within the last 5 years?

naah. i don’t really feel like it. i’ll just stay observing all these people irrationally throwing their money away. OK?

j/k — I am out the door for a Friday wedding, of all things. No time.

But I think, off the top of my head, that you can probably find equal evidence of so-called “bubbles” throughout time. Run ups in price, so to speak. They are followed by cooling periods, but never complete reversals. So it stands to reason that such cycles, if one were to hold throughout, say three, would produce substantial gains.

These are places to live after all. Shoot. If you’re happy, then stay there. Stay there 20 years. I bet folks do all right.

And you know, the “bubble” didn’t really affect everywhere. It isn’t like Central Michigan, Indiana, or Ohio saw big runups in value. All that cheap money. All those hideous giant new homes you can see from highways and stuff. NOt a whole lot of change in price indices. Right?

Seems like you didn’t read the article to the end. The research showed exactly the volatility you speak of: prices went up dramatically, then also came down dramatically, for different reasons and in several waves. But with nearly 400 years of data, the real return on real estate was only 0.2% above inflation. And this is for Amsterdam’s version of 94123. Not exactly substantial gains (but definitely better than tulips). In fact, in real value terms, it took ~350 years for a property’s value to double.

Properties in San Francisco rose 400% in nominal terms in under a decade, and it’s supposed to be justified and sustainable? Pardon me for being suspect.

“And you know, the “bubble” didn’t really affect everywhere. It isn’t like Central Michigan, Indiana, or Ohio saw big runups in value.”

Lack of big price runups is not necessarily indicative of lack of a “bubble” (although, of course, it may be). For example, it certainly a plausible argument that those places would have seen significantly _lower_ prices without the easy credit of this decade. And now that that spigot has been turned off, we’re seeing prices get killed in many of those areas.

Any idea why Sept SF median prices still went up 1.9% YoY, even with the most violent credit crunch in history in August?

400 years. wow. How can you apply an Amsterdam dynamic to a country where you could own something by planting a flag there?

Fluj, you ARE joking I hope? You did take macro and micro econ in University did you not?

Yeah, it was a joke. But it was just another theory, OK? Who are you anyway? Are you the same guy even? Whatever.

I’m glad I didn’t take econ. I get all the econ instruction I could ever need from the esteemed panel of anonymous soothsayers on this particular neck of the Internet.

Now THAT is funny Fluj. I also get great entertainment from this “neck of the internet”. (I am not the person who originally posted about Amsterdam btw, and I hope we are not in for that type of correction).

Dude wrote: “Show me some comparisons OUTSIDE of the bubble of 2000-present where, on a consistent basis, real returns from real estate outperform a balanced equity portfolio. Got any examples not within the last 5 years?”

How about 1995-2000? According to SFAR data, the average price of a San Francisco single family home went up 113% from 1995 to 2000. However, from 2000-2006, the average price of a single family home only went up 54%.

http://www.sfpulseofthemarket.com/Pulse48.pdf

“Comparing Septembers between an avowed peak year and a late summer ’07 rife with bad news? I’m surprised it was only 40 percent, to be honest with you. The market is cruising along. It simply is coarsing along at 70 mph these days. Maybe not 100 mph, but whatever. It’s still over the speed limit in most states”

“Sales have decreased on a YoY basis for the last 32 months.”

How about ’89 to ’94? Prices fell for 5 years straight. Which illustrates my point about the market being cyclical, and large run-ups usually being followed by corrections.

In retrospect, it’s easy to look like a genius if you bought real estate immediately prior to the largest run up in US history. IMO, this is more a reflection of “right place, right time” than the merits of real estate as a fantastic investment.

But to be open-minded and fair, maybe it really is a “new paradigm,” and the next few years prove me wrong. We’ll see. The State of California has 163,707 square miles, most of which are currently falling in value. Maybe these sacred 49 of ours won’t suffer the same fate. Even if they don’t, I’ll still have 163,658 cheaper square miles to choose from.

You are arguing against a straw man. I never said prices never go down. You asked for a period of time besides 2000-2006 in which SF real estate may have been a better investment than a balanced equity portfolio. The last half of the Nineties was another time in which investors in SF real estate did well.

I’m a grown-up and am willing to admit when I’m wrong. There have indeed been 2 five year periods when San Francisco real estate was a great investment.

I ran the numbers Dan linked to.

Average return over the 5 year periods starting with 1987-1992 ending with 2001-2006 was 47.5%.

Worst case was buy in 89 sell in 94: -9.3%

Best case was buy in 95 sell in 2000: 112.8%

Complete cycle peak-to-peak (buy 89, hold on, sell 06): 210.6%

Masters of the game (buy 94, sell 06): 242.4%

I certainly wasn’t expecting numbers that high. Buy and hold!

[Editor’s Note: Do keep in mind that a gross gain of 47.5% over five years is equal to a compound annual growth rate of 8.1%. And 210% over 17 years? 6.9%.]

“There have indeed been 2 five year periods when San Francisco real estate was a great investment.”

More than that. From 1985-1990, the median price of a home in SF increased 98%.

From 1985 to 2005, there has only been one 5 year period in which prices went down: from 1990-1995. The other three 5 year periods, prices rose rapidly. It is false to view the price run-up of the last few years as without precedent.

There have been other periods in SF history in which prices went down, including in the early ’80’s, when interest rates went sky-high. These price declines have usually been due to recessions and/or high interest rates. So there is always the risk of buying at the top of the market, and losing money if one has to sell shortly after buying.

Leverage on the way up is a beautiful thing. 10% down, and take that return and multiply it by 10X the same period.

Obviously, not good on the way down. But, that is the frustration, how the nation seems to be weak, and yet SF and NYC continues to hold strong.

Hey guys, I’m new to all of this, and most people on this site (seem to at least) have a little more knowledge than me when it comes to sf real estate. But this is what I see from the outside looking in:

The median household income in sf is around 60k. The median home price is about is about 775. @ 60k you qualify for about 300k in financing, which means average dude in sf is running around with about 400k in the bank(for a down payment)? Or if you have a couple, they both have about 90k (to meet the difference between the amount they can finance and the price)? Just looking at the general numbers, and a little common sense, it would lead you to believe that the average person in sf where financing with exotic mortgages.

Judging by all the problems with SIV’s on wallstreet, it doesn’t look like people are going to be jumping up and down for exotic loans on the secondary market any time soon. The long and the short is this, if people simply cannot get financing, doesn’t that bring demand down? (regardless of how awesome sf is!) Not to mention all the new construction in formally uninhabited places of the city (soma, mission bay). And lastly, more ARMs came up than in any time in recorded history in September (I believe), until January, which is expected to beat sept out. Which theoretically means more people having to find a way out of loans they cannot afford.

You guys know better than me (I’m trying to decide if I’m going to buy my first condo soon, or wait). So with all this going on in the market, how can prices continue to climb? Are they not destined to fall a little?

“The median household income in sf is around 60k. The median home price is about is about 775.”

The median income households in San Francisco are renters. Households making 60k are not buying 775k houses, generally.

@Vic – as you mention, the price/earnings ratio in the city is totally out of whack. Many of us, myself included, believe a noteworthy correction is coming. Regardless of your view, prices are definitely no longer shooting up, so you lose nothing by waiting another year to see which theory is right.

Coincidentally, even though 2/3 of the city rents, as Dan mentions, a vast majority of those that own are financed with adjustable mortgages.

I forgot to add, if you held any 7 year period from 1987 to 2006, the worst return was +1%. That was buy 1989 sell 1996. Of course, 1% doesn’t cover the sales commission or other transaction costs.

Here is a quick painless comparison between stocks and real estate. For 1978 to 2004, Stocks returned 13.4% vs Residential RE returning 8.6%.

http://money.cnn.com/galleries/2007/real_estate/0704/gallery.stocks_v_realestate.moneymag/index.html