With a typical influx of summertime residents and workers in play, the number of people living in San Francisco with a job increased by 5,000 in July to 546,600 while the number of unemployed increased by 1,500 to 19,300 which caused the unemployment rate to tick up from 3.2 to 3.4 percent.

There are now 81,100 more people living in San Francisco with paychecks than there were at the end of 2000, an increase of 109,900 since January of 2010 and 1,800 more than at the same time last year.

But the year-over-year gain in employment has been trending down since mid-2015 and is now at its lowest level in nearly eight years, with last month’s gain of 1,800 roughly an eighth of the year-over-year gain registered at the same time last year (13,800) and versus a year-over-year gain of 21,900 in July of 2015.

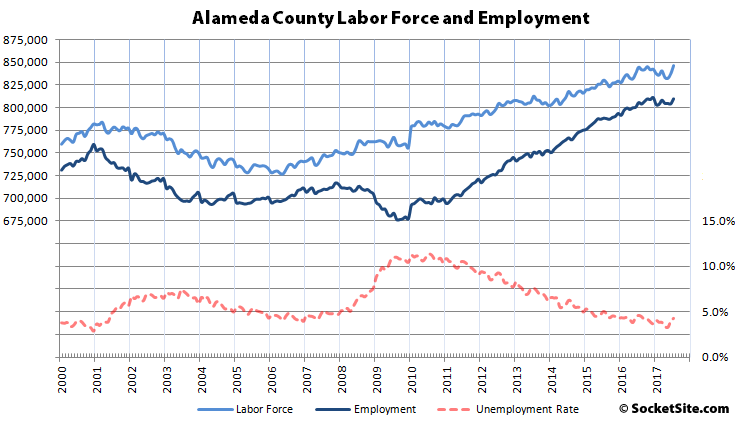

In Alameda County, which includes Oakland, employment increased by 5,700 to 809,500 in July, which is 4,300 higher than on a year-over-year basis and 117,500 more employed residents since the beginning of 2010. But the unemployment rate ticked up from 4.0 to 4.3 percent on account of the aforementioned seasonal influx of residents.

Across the greater East Bay, employment increased by 9,500 to 1,345,700 while the unemployment rate ticked up to 4.4 percent.

Up north, while the unemployment rate in Marin County ticked up from 3.1 to 3.4 percent, employment increased by 1,300 to 137,000.

And down in the valley, while the unemployment rate in San Mateo County ticked up to 3.2 percent, the number of employed residents increased by 4,000 to 438,900 while employment in Santa Clara County increased by 3,000 despite the unemployment rate ticking up from 3.5 to 3.8 percent.

End story: Employment is still gaining.

It might not be growing as fast as it did, starting after a large recession, but it is growing. Headline wants to focus in on a negative (as per usual SS), but this doesn’t mean housing is going to get any easier unfortunately

As usual, we focus on the bigger trends and turning points. Speaking of which, here are the year-over-year gains in San Francisco employment since July of 2015:

21,900

22,900

20,400

18,500

18,600

15,800

14,700

16,200

17,000

12,900

11,100

13,100

13,800

13,400

13,300

13,100

12,900

14,500

8,700

6,100

5,000

6,800

4,400

2,400

1,800

Can you spot trend that might be bigger and more meaningful than “employment is still gaining?”

And if so, do you understand the relationship between the pace of new construction and employment and the relationship’s effect on rents, returns and values? (Here’s a hint: employment alone is not the end of the story and the slope of a trend lines matter.)

Can you explain the relationship to those of us who are pretty sure we understand it but really have no idea what you mean when you mention the concept?

So “San Francisco Employment is topping out”?

That would actually be past tense for now as employment in San Francisco was higher at the end of last year.

A difference of 600 – what is the statistical margin of error on these figures?

Shouldn’t the headline be “SF Labor Force at Record High”?

Nahh, employment figures – no matter how good they are – need to be titled in some scary, alarmist language. “Nearing Negative Growth”! sound much sexier than “Labor Force at Record High”

touche.

Pet peeve rant: On top of that both the headline and Socketsite reporting on employment is and has always been somewhat misleading. The text is mostly accurate, but both headline and a couple places in the text it says “employment.” Most people would naturally think “employment” means “jobs.” It does not. What they are are reporting is the number of employed residents of SF – regardless of where they work (SF, SV, East Bay, etc), which is absolutely not the same thing as the number of jobs in SF. While undoubtedly they follow the same general trendlines across broad cycles, the numbers and micro-trends of jobs in SF vs employed residents in SF (or any other city) month-to-month or quarter to quarter could be quite different, and for many smaller cities they probably are not correlated at all. For instance, a trends in the number employed residents in Daly City probably has a lot more to do with the number of jobs in SF than it does with the number of jobs in Daly City. A story on “employment” in SF would typically be about jobs, not about employed residents who work anywhere in the Bay Area.

Or as we obviously bury in our first sentence above, “the number of people living in San Francisco with a job.” (Which, when it comes to local real estate, is more important than the number of jobs in the city to which others commute but demand housing elsewhere.)

Given that this pet peeve comes up over and over…and over again, perhaps the Control Voice @SS can explain – or explain again for those who might have missed it – why this type of info ISN’T provided, as either an addendum to these monthly posts or (even) its own thread (as opposed to, say, threads on random retail spaces or suburban houses…charming though they may be).

And yes, the explanation “because it isn’t readily available” is perfectly acceptable…however idol dashing it may be.

Mainly, as the editor points out, if you live elsewhere then by definition you are not a factor in the local RE market even if you happen to have a job in SF. And if you count jobs via payroll data, as would be typical, what’s to say that a person on the payroll of a SF based company isn’t working remotely some or all of the time? Or what of someone on the payroll of a company outside SF who is physically working here in SF either in a satellite office or co-working space?

Also, a fairly typical definition of “employment” bins every working age person as either “employed”, “unemployed” or “out of labor force”. But a person can have no job, one job or multiple jobs. An increase in part time and/or gig work can increase the number of jobs without changing employment and/or #hours worked.

What do you think that the jobs data would tell you that the employment data does not?

I’m thinking it would be useful in tracking:

(1) office lease rates – as opposed to residential rentals – since it seem reasonable to assume the former is related to how many people actually work there …reasonable to me, at least; and

(2) how great is this “housing crisis” we hear about from time to time – as in daily – which is impacted by where people live vs. where they work (or more to the point, if they’re living in, say, Sonora and working in SF it must have a different impact on the market than living in SF and working there).

As for the data being aggregated by location of HQ vs. job-site, that was what I was getting at by “maybe not being feasible”: it’s my impression that the EDD tracks by the latter – or at least they have it available – but if that’s not the case, then you’re right, it wouldn’t be helpful. And the usefulness of the “employed” data is largely predicated on the assumption that you have to be employed to live somewhere..which of course is untrue for the retired or profitably idle.

Hence the request for comment from the editor: the request was legiitimate, only 5% snark (by weight).

No, that’s absolute nonsense. The number of jobs in SF absolutely is a driving factor (if not THE driving factor) of the RE market for housing in SF. The fact that many of those folks live outside the city is as much or more a function of the shortage of housing in SF as it is that those workers just want to live somewhere else. The housing shortage elsewhere in region to house their workers (eg Mtn View, Palo Alto) also contributes to the SF housing market (at least more than it used to), but job growth or contraction in SF is absolutely the driving factor of the housing market in SF.

The value of any good, asset or service is dependent on the incremental unit of demand once a market reaches full capacity. Therefore, while still positive, slowing employment growth implies less incremental demand. You already see that manifesting in rents.

When the incremental unit of demand turns negative, as it appears likely to do soon, the pace of price declines accelerates in a non-linear way – owning to aforementioned full capacity – until equilibrium is reached.

Axiom: markets overshoot in both directions.

The West Coast cities, gold rush, are Seattle and LA for the next decade at least. Population growth, projected,, job growth and other measures.. LA is building a world class public transportation system. SF is nowhere to be found. BA folks are, IMO, in denial.

Dave, you first called the peak in what, 2014?

No. I said/felt 2014 was close to a peak for SF RE and exchanged my rental properties to the NW. I think the recent record jobs number is a peak and going forward there could be a significant drop in the SF labor force. No one can time the “market” and call peaks – whether in RE or stocks.

Ok, I guess this is a different Dave?

September 2014: “SF seems to have peaked out and the risk is getting caught in a bubble and bidding homes up unrealistically.”

That was me and I said “seems” to have peaked. The observation was in reference to RE prices and not the labor force.which this thread is about. I’d say today, summer 2017, that SF’s labor force “seems to have peaked”.

This is pure gold. Depending on where your property in SF is, 2015-2017 saw major appreciation in some parts of the city (e.g. Bayview)

[Editor’s Note: Or not.]

The point is there were signs of a coming peak in 2014. Early signs which seem to be more obvious now with the slowing of SF home price appreciation relative to many other metros, the stalling of labor force growth, negative office space absorption for the previous two quarters and more. The market can’t be timed but one can read trends and react accordingly. As an investor I reacted in late 2014 and shifted my rental investments. I did not see the huge surge in prices in the Seattle area coming so soon – it was a nice surprise to see Seattle RE appreciate at close to double the rate SF. In 2016 and more or less so far this year. That should continue for a number of years to come.

Labor force is the key and job growth is slowing here and projected job growth here is not expected to match Seattle or LA or Austin or Dallas or …ad a few other metros. Prices will react accordingly. The unfortunate thing was that SF was not equipped to handle, based on infrastructure and already sky high rents and home prices, the job growth of the past 7 or so years. A time out is long overdue – these labor force numbers and trends indicate that timeout may be upon us.