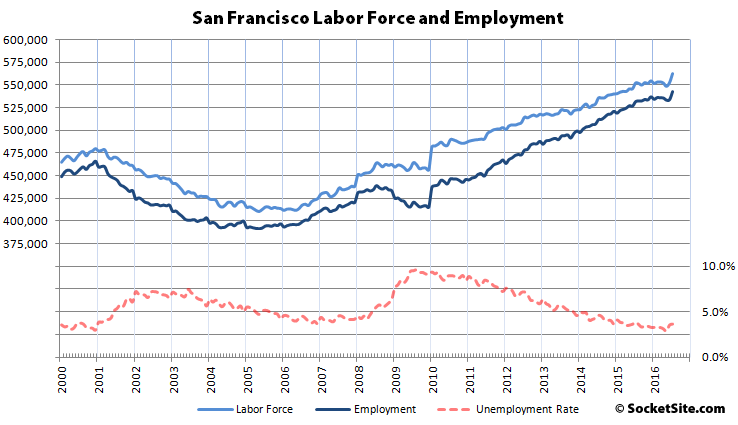

With school year seasonality and an influx of interns in play, both the labor force and number of people living in San Francisco with a job jumped like Kris Kross in July.

While the jumps were to be expected, the 9,900 person increase in the labor force was 65 percent above average for the past five years. And the 8,900 person jump in employment was 75 percent above the post-recession average for July.

As such, there were 76,600 more people living in San Francisco with paychecks last month than there were at the end of 2000, an increase of 105,400 since January 2010 and 11,100 more versus the same time last year.

And the number of people living in San Francisco with a job (542,100) has increased by 5,700 since the end of 2015, but that’s versus an increasing by 10,500 from the end of 2014 to the same time last year.

In Alameda County, which includes Oakland, the labor force jumped by an above-average 14,300 in July while the number of employed residents jumped by an above average 12,300.

In fact, the number of people living in Alameda County with a job last month was up by 113,300 since January of 2010, a greater increase than in San Francisco.

And employment across the greater East Bay jumped by 20,600 in July, the biggest jump in over 15 years, while employment jumped by 7,300 in San Mateo and by 7,800 in Santa Clara County.

“there were 76,600 more people living in San Francisco with paychecks last month than there were at the end of 2000, an increase of 105,400 since January 2010” and “increased by 5,700 since the end of 2015” — hence, the current state of SF rents and housing prices. That is the “demand” component for those who are skeptical about supply, demand, and prices.

Sorry, demand has two components, willing and ABLE. Since the affordability level in SF is well below 15%, and assuming the quality of these jobs is somewhat similar to the nationwide figures (heavily skewed towards very young and very old workers, low paying/seasonal jobs for the Top Ramen crowd) then this would have minimal influence on local real estate demand, which itself is skewed heavily towards foreign and VC funny money. Look at what happened to the Vancouver market since the recent foreign purchase tax, it absolutely fell off a cliff in terms of both volume and price.

Yes, the “able” component of demand is reflected in the demand curve, which intersects the supply curve at the . . . price. Thus, the high selling prices we see demonstrate that the demand is determining the high prices (along with the limited supply; only about 5000 units a year sell off the MLS, e.g.). If the 100,000+ newcomers were short order cooks and maids (as was seen in Las Vegas’ growth in the ’00s), rather than, say, tech professionals, then the demand curve would not produce the prices we’ve seen.* 100,000 new workers in 6 years and just a fraction of that number in new housing units, and the explanation for skyrocketing housing prices is quite clear. I agree that if SF imposed a new 15% sales tax on a significant number of buyers, that would likely lead to lower SF sale prices as that would shift the demand curve to the left, but that has not happened in SF.

* we could still see a demand curve supporting high prices if banks were handing NINJA, no-down loans to anyone with a pulse, as in 2003-06, because that would also move the demand curve to the right, but I haven’t seen any evidence that is driving anything as banks have very tight income and lending standards. And VC funny money is still real money in bay area workers’ pockets.

I agree it’s obviously been a factor over the past six years, but we’re talking about these new July jobs. You haven’t proven that they are well paid tech jobs nor that there is any correlation with real estate demand. All figures I’ve seen are showing a slowdown in tech, and I’ve read quite a few articles about a recent increase in investors buying homes.

Even if these are mostly non-tech lower paying jobs, there will be some RE impact. If nothing else on the rental market and specifically the “in-law” units springing up. More people in my neighborhood have started renting out their ground floor (garage level) bedroom/bath as they can get $1800/month give or take.

I was talking about the 105,400 additional SF employed persons since January 2010. I agree that I don’t know a whole lot about the new jobs in the month of July 2016 (although, very anecdotally, a relative just moved here in July, a new college grad, making well above the six figures threshold as a developer). Of course, if investors buying homes are increasing, as you’ve read, that would only shift the demand curve such that prices would head even higher.

I’ve opined for quite a while here that SF housing prices appear to be at a level that wouldn’t be sustainable in the event of a number of events. My only point above was to show that the reasons prices have shot up for the last four years is largely explainable by the big jump in population (which, as Jake points out, has been accompanied by higher – not lower- incomes).

Isn’t it pretty amazing though, that 37% of those “newcomers” with their “well paid jobs” somehow have ALL CASH to purchase a property in a city with median home price of $1.3M? This doesn’t even count the many people who are taking out only small loans with massive down payments.

I wouldn’t find that so amazing. SF only sees something like 7000 or 8000 home sales a year, give or take (new and re-sales). With the unreal amounts of tech money flowing into this city, that a couple hundred a month are able to pay cash for a home doesn’t seem that astonishing to me. I agree that if/when this boom runs its course, that will change. But it is presently still going very strong. It is not only the newcomers buying homes, but the newcomers have just added to the demand.

About 5 out of 6 of the new arrivals to SF are renters not buyers. And the people that move to SF and buy a home instead of rent are about 30-40% of the buyers in a typical year.

Sorry but I think you’re in denial about where a major portion of the demand for SF real estate is really coming from. And almost everyone on this site is in denial in thinking that building more housing will have any effect whatsoever on local housing prices, as long as that particular type of demand continues. With the exception of massive apartment high rises, which do relieve some pressure on rents. These false assumptions are based on archaic and irrelevant real estate market folklore.

Anecdotal data guy here! For the last several weeks I’ve dealt with three rental turnovers in the mission. I got loads of inquiries from the 22yo-just-graduated-first-job crowd. Salaries ranged from $65-110k. Many were in tech of course, but surprisingly also diversified in medical, bio, finance, consulting too. Probably 60-65% tech, rest other. They’re still comin in folks!

I predict no or little compression in rent prices, except for luxury condos. I predict a continued steady influx (seasonally adjusted) of new hires. Steady as she goes for the next year or two, wrt rentals. Or for my real barometer, burritos ain’t replacing sushi/gourmet lunches for this rentier any time soon!

But that’s me.

At a salary of $65-110k do you know what you can buy in SF? An old camper van to park under the freeway, that’s what. These people are NOT the ones driving up SF real estate, folks.

Interesting anecdotes, Rentier. Keep it coming. BTW, don’t you also have units in the Bayview? Interested in any anecdotes from there as well!

Sabbie, not sure who you are addressing, but my data comes from the US Census ACS not RE folklore. Thousands of heads of households move to SF every month. Average year-to-year, roughly 8% of SF households weren’t living in SF a year earlier. In boom times that can go as high as 10% and in bust times as low as 6%, been around this range for a very long time, decades. BTW, most of the people that move to SF move from within the Bay Area.

In the current boom, VC investment in SF has been on the same dollar scale as the entire value of all home sales. And that is a spigot that can double or halve in a matter of months, and then do it again in the next few months, and so on. If Twitter had become a profit monster like Facebook did, then SF would be in IPO-insanity to rival the late 1990s.

Jake, I am not questioning SF population or jobs count. Again, demand = willing AND able. So what’s relevant is how many residents *with the necessary level of income and savings to actually afford property at these prices*.

“And almost everyone on this site is in denial in thinking that building more housing will have any effect whatsoever on local housing prices”

Yeah, gee, I wonder why all these people on this site, and all those professional economists with their fancy ‘degrees’ and ‘studies’ feel that increasing supply will have an effect on prices.

(Note that we are finally increasing supply here in San Francisco and prices are not increasing.)

The same way that the experts thought building more and wider freeways would result in less traffic congestion.

Sabbie, the Census data clearly shows that over the past 5 years less than 16% of new arrivals bought a residence in SF. That is less than half of your 37% all cash. You may not doubt the stats, but they put doubt on your statement, unless you were just kidding or being facetious.

And there is nothing at all unusual about these patterns. When gobs of VC and wall street money pour into SF/SV many (thousands to tens of thousands of) people get rich who were already in the bay area and many of them then buy where they live, especially in the areas with good commute access to the job centers of SF and SV.

Individuals converting startup stock into investor cash into SF/SV RE has been going on since the early VC days of Fairchild and Intel.

Jake, thank you, now we’re finally getting somewhere!

Since less than 16% of new arrivals were able to buy a place in SF, and 37% of sales were all cash. what does this tell us? That the mainstream narrative is false, it’s not all these new arrivals with their well paid new jobs driving up prices for many SF properties, it’s a smaller group of people with excess cash.

The demand in SF is split in nature: there’s the average resident who wants to buy a place but is priced out, then there’s the foreign funny money and IPO lotto winners who can actually afford it. Sure there are techies stretching their limits for TICs in the Mission and Outer Sunset 2BRs, but in huge swathes of the City we are dealing with a different sort of demand, and this demand will never be met by tearing down a few gas stations and putting up six unit luxury condo buildings.

Sabbie, I was talking strictly about rentals. And the $65-110k crowd can rent here all day long at $1500-2000 per person per room.

As for homes sales, we have seen the volume continue to go down as prices increase. But besides (what you consider) mystical all cash, foreign buyers and tech IPO crowd you have locals here that already own, have equity, basically your step up buyers. As for the supply/demand balance, a lot of sellers don’t have to sell. Which is why sales volume continues to go down as greed/price increases don’t match buyers willingness. But many of these market testing sellers just take their props off the market. We’re seeing that too.

This is basically a sticky market. You need an external event (like 2008) to upset the apple cart, and that ain’t happening yet. And personally I don’t think it will happen.

My prediction: détente in the market, flat appreciation, lower sales volume, for the next year or two. Just hang back and relax if you won here! And then next upturn…kaboom! Business as usual. And in the meantime our board of [Supervisors] will have helped setting up the next market growth by increasing affordability component of future developments, nymbism, etc. You’ve lived here long enough; you should know the song and dance here. Just refer to your 70’s rockers….and the song remains the same.

My prediction fwiw — if nothing happens sooner, a .25bps rate hike in December (of course they will wait until after the election) will result in a 20%+ long overdue correction in equities, and given that a large number of economic indicators are already in historical recession territory, this will put us firmly into the next downturn cycle, at which time many techies will head to parents basement (after pissing away severance in SE Asia) and the massive oversupply of new apartments will show that ‘the emperor has no clothes’ and give us a much needed major respite in rental prices.

Home prices will only see a modest decrease however as per the TINA market (There Is No Alternative) given that we have so much cash out there that is desperate for safe haven and yield.

The huge wild card however is that the Fed can no longer lower rates in response, so will the new administration admit Keynes was wrong and move quickly to enact fiscal stimulus, or will they flounder and take us somewhere much darker? Good luck out there everybody!

“Since less than 16% of new arrivals were able to buy a place in SF, and 37% of sales were all cash. what does this tell us? That the mainstream narrative is false, it’s not all these new arrivals with their well paid new jobs driving up prices for many SF properties, it’s a smaller group of people with excess cash.”

16% of new arrivals is a much larger number than 37% of sales. Like an order of magnitude higher.

“will the new administration admit Keynes was wrong and move quickly to enact fiscal stimulus”

Sabbie, that is precisely what Keynes said one should do to counter a slowdown. So the question is whether the post-2016 congress and president will admit that Keynes was right and move quickly to enact fiscal stimulus. You and I appear to be in agreement that would be the best move. I think there remains enough slack in the labor market to continue to justify a keynesian stimulus, and, as you know, I’m all about slack.

Bob-

Sabbie’s very savvy – that has to be a typo.

Sabbie can you point to anything that supports your foreign buyers take? anything at all?

I posted a few links about foreign buyers a while back and the moderator deleted them. If you are truly interested and not just up for an argument then I can recommend Google.com to search for articles about foreign buyers in California and the Bay Area.

Ah…the ‘ol moderator deleted them excuse, followed by a “you can find them yourself” jab. Classic tactic.

In the time you spent writing that comment you could have actually performed the search and read about it. The old “head in the sand” tactic.

Um, I’ve searched and found nothing that supports your argument. That’s perhaps why we asked you to provide links? Continually claiming “they’re there!” does not make it so.

If you’re not adept at online search, the other option would be for you to contact any local, experienced real estate professional and ask for their opinion regarding this trend.

I have, and all of them dispute your claims…which is why we’re asking you for some proof. Weird, I know.

“Individuals converting startup stock into investor cash into SF/SV RE has been going on since the early VC days of Fairchild and Intel.”

Indeed. One might argue that this is one of the foundational aspects of SF real estate values and had been for 40+ years

And again, it’s not the sheer numbers, but the nature of the demand. While the majority of home buyers rely on the principle of substitution, a small number of atypically motivated buyers have no problem with bidding 30% above asking to ensure that they can find a home for their cash. That’s the demand that drives prices to insane levels, not the everyday demand from Joe and Suzy Homebuyer.

I Google this every now and then. I just did. Most articles state “California,” and if they mention San Francisco there are no numbers whatsoever. Often they don’t even talk to someone working in the market. Sorry, but I don’t think you have anything despite your repetition of this theme. Don’t get me wrong, I don’t dispute that Chinese investors in particular have been active in the SF marketplace. What I question is that it has really moved the needle much. I think it’s practically a nonfactor in comparison to the proliferation of well compensated local American workers.

Well if I am wrong about foreign buyers (which I’m not) that just means the local market will tank that much harder when (not if) the tech bust comes.

Can’t disagree with you there, I don’t expect us to be bailed out by foreign buyers. That said, I think that any local market tanking in SF proper will be pretty minor (similar to 2007-9).

Here’s just one article. It says 1. Chinese buyers make up 6-10% of SF buyers per Trulia (note that this does not include other nationalities) 2. these figures are under reported because many use US intermediaries 3. they have pulled back recently due to frothy prices but could be ready to step back in and BTFD especially if the yuan continues to devalue.

Well at least we have a timeframe for this bust. if it doesn’t happen by the first quarter of next year, will you admit a mistake? We’ve been hearing about the impending collapse of our housing for a long, long time.

Sabbie,

from the Trulia article you posted: “”We’ve seen a sharp drop over the last three years in search activity on Trulia, about 50 percent” by Chinese buyers, Ralph McLaughlin, chief economist for the San Francisco-based real estate search engine, told China Daily.

A drop over the last 3 years? That doesn’t even sync up in any way.

Sabbie, more than 10% of the current population of SF was born in the PRC and while most are naturalized, many are not. Do any or all of them count as “Chinese buyers”? Overall, ~14% of SF population are not US citizens and ~35% were born foreign nationals.

FWIW, the growth of the Chinese population in SF since the immigration laws were de-racialized in the 1960s is greater than the entire population growth of SF in the same period. People move from China to SF every month. No doubt some buy a home here when they do.

More generally, for the Bay Area, half of all population growth of the past ~50 years has been (foreign) immigrants.

We basically import talent (domestic and foreign) and investor cash (worldwide) to create companies and traffic congestion and inflated RE. I suspect the foreign investor cash fueling our corporations and jobs is a much bigger driver of the price of RE than the foreign investor cash going into direct purchases of residential RE.

As Jake mentions, we have to parse out Chinese (and Asians in general) living here vs those from abroad. In my mind, any of these people who are either US citizens or have green cards should be considered “American” vs. a true foreign buyer that resides abroad and either rents, leaves empty, or saves for their kids a property here. The latter is a much smaller size. Anecdotally there have always been lots of Asian buyers in the SF market, especially in D10- I’d venture to say that about 50% of the transactions in D10 are Asian. Also don’t forget, what about families pooling money from family from abroad? That is another legit foreign element that influences our market.

Jake- “I suspect the foreign investor cash fueling our corporations and jobs is a much bigger driver of the price of RE than the foreign investor cash going into direct purchases of residential RE.”

Care to elaborate on that? Given that most tech investments are usually VC or large tech Corp based, not sure how private foreign money is having an outsized financial influence. Of course foreigners working in tech, and contributing to the economy is significant, but that a different influence. As for foreigners setting up shop here, if they are citizens or have PR or work permits, they tend to stay here, so I see them more as Americans in the long run anyways. This is different than a foreign entity buying tech firms, or putting money straight in- usually they go through funds, etc., and don’t have direct control over the inevestments themselves.

I didn’t claim anything was “outsized”, but there sure is a lot of foreign investment money that pours through the Bay Area. Just today an SF tech company (druggies) was sold for $14 billion to a NYC company that outbid a French company that only offered $9 billion. The other day a Chinese company bought a 42 acre chunk of Oyster Point to build an office park that will compete with the grand plans for Bayview. They plan to spend one billion USD. That will be money coming back from Shanghai to the shores of San Francisco Bay.

Japan’s richest man is a VC with deep roots in the Bay Area. Masayoshi Son graduated from UCB and founded a company in Oakland. Softbank, his Japanese investment company, has been a major player in the US tech market for 20+ years. They even owned COMDEX through the entire dotcom era. They had a deal with Yahoo back in the good old yahooian days. BTW, he is of Korean ancestry and his last big score was a Chinese company you may have heard of, Alibaba. Among Softbank’s most recent investments is $76 million in an SF based company. Money really doesn’t care much about nationalities, just ask DJ Trump(et).

Panasonic is Tesla most important business partner. And Tesla builds their cars at a plant that used to be joint operated by Toyota and GM. Cannon was the largest investor in Steve Jobs computer company (Next) during his Apple hiatus. ….

Overall, foreigners have ~$3 trillion invested in the USA.

The idea that these huge flows of money aren’t more impactful than gaggles of foreigners looking to stash a few million privately in SF RE is just silly.

Well sure, but they are entirely different things. I though you were talking about private individual foreign money going into tech vs buying RE. Corp money is Corp money (even if it’s owned by a rich individual like Masayoshi.)

Here’s another great article if you want to see what sort of foreign demand we are looking at: China’s capital controls fail to curb outbound investment.

Sabbie, funny stuff – you say things to folks like “you haven’t proven……” – and then you go off and make 47 assertions that aren’t proven.

I think you’re basically wrong, ‘safe haven’ money is a factor but a minor one, not the driving one (where’s your evidence?), and quite arrogant in that you evince zero doubt.

Again, there’s no way to prove OR disprove it, because nobody is keeping track, although they should be. And again, we do have at least two hard numbers to work from: 37% of SF purchases are all cash, at median price of $1.3M. It is just ridiculous to say that this crazy amount of cold hard cash originates from salaries.

Doesn’t matter to me if you believe it. Go ahead with your blind devotion to building as many luxury condos as possible and see if it ever makes a significant dent in affordability. My guess is no way.

And if it doesn’t? What’s the harm? We have additional tax generated from the sales, we have additional money paid into the affordable housing fund and/or additional affordable units built on-site, and we have additional units that will be cheaper when “the crash” comes.

Also, no one here has said that the 37% of all cash purchases originates from salaries. Everyone has said that it’s related to stock grants, options, etc. I’m 15 years into an engineering career (now at one of the big companies, manage a team of 8), never worked at a startup, but have received stock grants that cumulatively exceed $2M in value (either when I sold or now for those still owned). Bull markets are pretty nice to companies that dole out bonuses in stock.

$1.3M in cash is just not that big of a number for the ridiculously tiny number of properties that change hand each year in SF, considering the stock increases of the last decade for big, boring, and old companies like Google and Apple, let alone newer companies.

The harm is that it’s already way too crowded. It lowers the quality of life for existing residents. The traffic is beyond nuts lately. I’m moving next year, so whatever. My main point is people fail to look past the obvious, if we want to reduce all of this social disruption and friction then we need to address the boom and bust FIRE economy.

“Way too crowded” is simply your opinion. More density increases my quality of life, period. I bought in a place where I can walk to work, and the increased services provided by more people are far more important to me than having slightly less traffic for the times that I need to drive.

It doesn’t sound your concern is around increasing prices, but rather that you’d simply prefer that we lift the drawbridge and prevent further growth and/or newcomers. That’s not the city I want.

Your assumption that more density will attract needed services has not played out much in terms of city infrastructure. And your tax revenues from higher RE values have also not been reflected in improved city services, as far as I can tell. I don’t want zero growth, I want growth at a slower pace, one that’s closer to the ability of government to keep up, and also closer to the general pace of salaries and inflation so that it doesn’t cause mass social upheaval. Financially this boom has been dandy for me since I own rental property, but everything else about it sucks.

Anyways, this article was about jobs, and Bob DID indeed say these jobs make up the demand side of the local real estate equation. And my response is no these jobs do NOT constitute the greater part of demand that is driving up SF real estate prices. Like you said, it’s a lot of people cashing in company stock, and it’s foreign buyers too (even though for some strange reason everyone wants to deny it).

When I said services, I was more talking about restaurants and the like.

I don’t have any confidence in the SF government to keep up at a slower pace any more than they can at the current pace. As far as keeping real estate prices more in line with salaries and inflation, I don’t have a lot of confidence there either, since the Fed seems to want to keep inflation below their target (really the only way to explain below target inflation for years on end from any central bank). Monetary policy has been too tight this entire recovery period, and I expect that to remain the case, especially if the Fed prematurely raises rates again.

The reasons inflation is below target are 1. measurement error (real inflation is actually quite high) 2. failed theory (lower rates have failed to promote real economic growth but rather financial engineering of bubbles) 3. Fed keeps moving the target (we’re way behind the curve per the Taylor Rule). They should have raised a long, long time ago actually.

Ah, the ‘ol Trump conspiracy theory. Ok then. Good luck with your goldbuggery.

The reason there’s a boom/bust cycle is due to prices feeding back onto prices.

The newly minted $100k engineer can lever up and buy a home and will do great if prices go up. But if prices stagnate or go down will just end up spending a huge amount of what should have been savings on housing costs.

Combine that with the fact that tech goes in waves, when times are good big company stocks go up and many startups are formed. When times turn, big companies do layoffs and startups fold.

When things go well, they go really well. And when they turn, they really turn.

Low rates and looser lending just makes the cycle more extreme. Lower rates allow people to lever up to a higher price to income multiple and lower down payments open up the gate to people earlier in their careers. Lower rates also drive investors to seek yield and drive money into established tech stocks, VC funds and profitless “growth” companies.

Right, a conspiracy shared today by billionaire fund managers like Soros, Icahn, Dalio, Gross, Gundlach, Druckenmiller, Jim Rogers, Spitznagel, etc etc. But I guess you’re smarter than them. Bourgeois coastal bubble dwellers with blind faith in ivory tower bureaucrats and White House press conferences peddling fiction are in for a surprise soon, economically and politically. And I don’t have much sympathy. Because in 2009, “nobody saw it coming” was a reasonable excuse. But this time, all the problems I mention can be seen almost daily on mainstream outlets like WSJ and Bloomberg or even CNBC. Heck even the current and former Fed members themselves are expressing these concerns.

“2. failed theory (lower rates have failed to promote real economic growth but rather financial engineering of bubbles)” “Ah, the ‘ol Trump conspiracy theory. Ok then. Good luck with your goldbuggery.”

Why is this conspiratorial?

You can borrow money and do something useful with it or you can borrow money and do something useless with it.

If an economy crashes due to fear and under-investment, then lower rates can help the recovery. If you have great investment opportunities and profitable companies sitting there waiting to be built for lack of capital, then increasing the availability of capital can stimulate real economic growth.

But if you have an economic bubble of unproductive activity (i.e. the 2007 housing bubble and much of the 2000 dot com) collapse, then trying to stimulate the economy back up to bubbly levels may not produce real economic growth.

If you come into the ER with abnormally low blood pressure, the doctor might give you medication to bring it to normal levels. But it doesn’t follow that increasing the blood pressure of a healthy individual will make them even healthier.

Do you want me to name the billionaire fund managers that do not believe in your conspiracy theory? Or the economists that do not? Naming a dozen names doesn’t make something obviously true, and just because a billionaire says it doesn’t make it respectable. A lot more billionaires got 2008 wrong than got it right, and there are plenty of super rich people who’ve been claiming for a decade now that inflation was right around the corner.

@incog – I’m not at all saying that we should be trying to stimulate the economy. I’m saying that the Fed should uphold their mandates, like any other time – full employment and 2% inflation. They’ve utterly failed the latter for 7-8 years.

The Fed just keep moving the targets in a pathetic dance of lost credibility. The only way to “uphold their mandate” is to force them to be data dependent. Ben Bernanke in 2015 on the target employment rate: “Nobody really knows that number with any precision,” adding, “and the Fed will continue to grope to find out what the right number is.” And just last week John Williams suggesting raising the inflation target from 2%. The only number the Fed is honestly targeting is the S&P 500.

anona-

There you go again bizarrely equating all criticism of neo-liberal monetary policy with goldbuggery.

I’ve elaborated for your benefit a post-Keynesian critique of you beloved monetarism (if you think post-Keyesians are goldbugs, you really need to get an education). You persist in your delusions, and worse, accuse all critics of loose monetarism of being Trumpers, revealing a sloppy and disingenuous ignorance of political economy.

All critics of of the Fed are goldbugs and Trumpers — it must be comforting to have such a simplistic understanding of politics and economics.

I submitted a couple links yesterday regarding Chinese investment in RE, but they didn’t make it past mod. Whatever you do, anona, please don’t use google to try to find anything that doesn’t fit with your confirmation bias.

Unless the links to which you are referring were disguised as “viagra without a doctor prescription from canada, cialis without a doctors prescription canada, viagra online pharmacy no pres needed, cialis online canada pharmacy,” we don’t see any pending or moderated comments from yesterday with respect to Chinese investment.

thanks for keeping two beers and Sabbie honest, editor.

two beers – I only claim goldbuggery when I see it. It’s quite evident here, with Sabbie claiming a massive conspiracy to rig data that’s been measured the same way for decades ad you claiming that some of the tightest monetary conditions in history are “loose money” because the fed funds rate is at or close to zero (meaningless to the actual stance of policy unless you believe that policy was super tight in the 70s and super loose in the depression).

Saying that CPI is understated is far from conspiracy, it’s actually quite widely accepted among many economists, it was even studied by Congress. The reason they do this however is not to keep interest rates low (since the Fed answers to nobody they can come up with a billion lame excuses for that) but to keep payments like Social Security low. Also it has not been calculated the same way for decades, it’s constantly being tweaked to substitute cheaper items for ones that have inflated (chicken for steak, for example).

Referring to the last fifteen, let alone eight, years as “some of the tightest monetary conditions in history,” is breathtaking and audacious revisionism. I guess if you’re going to be wrong, you might as well go large. Your flat earth zealotry is endearing, or maybe there’s just some really, really bad acid going around.

If the most accommodating and extended monetary expansion in history isn’t “loose,” then what is? You believe loose money must stimulate the economy, and because the economy hasn’t been stimulated, therefore we don’t have loose money, despite all the empirical and consensus evidence to the contrary. See the logical fallacy there? Are you puling my leg, or are you just a crackpot?

Value of international purchases of American homes and Location of Chinese home buyers.

“[…] we’re seeing a large influx of foreign capital — particularly coming from China.”

two beers – what is your definition of “loose”?

sabbie – of course the elements within the CPI change, that’s part of the methodology. The methodology hasn’t changed in decades, which is the conspiracy that you’re claiming. It would also mean that all other inflation measures – including those conducted in other similar countries by other governments – would have to be in on the fix.

and two beers, again, I absolutely do not believe that loose money “stimulates the economy” or that the Fed should even attempt to stimulate the economy. The Fed should focus on its mandate and nothing else. If the economy needs “stimulating” then fiscal policy should take over. However, in current times the Fed has systematically kept inflation too low, and in times of fiscal stimulus has nullified that stimulus by monetary contraction.

If we can’t get the Fed to focus on its mandate, it doesn’t matter how much fiscal stimulus you try.

The Fed “mandate” is anodyne, and so broad, vague, and contradictory that it can always be used as a justification for whatever policy it takes. Stable prices, “maximal” employment, “moderate” interest rates? Who can argue with those?

Who cares if policy that “stabilizes” the prices that benefit one class happen to immiserate another class? If one happens to think that endless years of ZIRP aren’t moderate, but are actually extreme and work against the “long run potential to increase production,” than you must be against stability! You don’t like negative interest rates? Then you must be anti-growth! You don’t like asset bubbles caused by ZIRP and QE1/2/3? You must want to throw people out of work! You think old people old be able to get the rate of inflation on their savings? That’s not “moderate” interest!

How convenient that whatever policy the Fed takes, it always just happens to be the one that boosts asset prices at a pace that vastly outstrips the productive economy. The only part of the Fed mandate it pays any attention to is the very first part (“maintain long run growth of the monetary and credit aggregates”), although it is empirically only concerned with short term growth. The rest of it (“long run potential to increase production, so as to promote effectively the goals of maximum employment, stable prices and moderate long-term interest rates.”) has been a farce. Fed policies have been extraordinarily accommodating to the employment, prices, and rates that the upper classes enjoy. Those same policies have been devastating for the employment, prices, and rates of the vast majority of the populace.

The Fed did a wonderful job of upholding its “mandate” in maintaining employment of bankers by buying up trillions of dollars of toxic assets from Wall St. Workers on Main St are still waiting for the mandate to smile on them.

It’s like having as our foreign policy a mandate of “make America great again,” and “everywhere be a force for peace and stability.” “Sorry we had to bomb your little country, be we had unleash death and chaos on it to spread peace and spread democracy.”

“The Fed “mandate” is anodyne, and so broad, vague, and contradictory that it can always be used as a justification for whatever policy it takes. Stable prices, “maximal” employment, “moderate” interest rates? Who can argue with those?”

Agreed, that’s why the Fed should switch to hard rules that they can be audited on. I don’t disagree of most of the rest that you wrote too, I just have no idea why you want the Fed to tighten policy now, even though you freely admit that any fiscal policy used to offset the tightening will be quickly squashed by the Fed in support of everything else that you mention.

Why not switch them to a rules-based NGDP targeting (or another target) approach, hold them to it, then enact whatever fiscal policies that you’d like? What is so magical about the fed funds nominal rate being higher than it is now? How will that fix anything?

there is no evidence that there is a large contingent of foreign investors buying SF rela estate. thats a red herring

That is really an increase in incomes becoming an increase in the price of housing. SF real per capita income is up at least 20% since 2000, while housing units increased about the same as population (net increase of 11-12% residents between 2000 and 2015, per Census, and net increase of 10-12% housing units, low per SF gov and high per Census). Of course mortgage interest rates have been much lower than the ~8% in the late 1990s and 2000.

The real reason SF has higher RE prices now than in 2000, inflation adjusted, would seem to be more correlated with being richer and having a higher proportion of income available to spend on housing than these ratios of people with incomes to housing units.

Don’t all these nubie-incomed know they could crash on Brian Chesky’s couch for $50/night?

Maybe if Airbnb moved their HQ to Oakland it would help solve SF’s housing crises. And if Uber moved to Oakland it would help solve our traffic congestion.

If we just weren’t so financially successful, then we could afford to demand cheaper housing prices.

Perhaps it would be fun to revisit some history. Back in May 2006, Bloomberg ran a piece titled “Why The Housing Bubble Won’t Burst“.

The author’s main argument: housing won’t drop because of “the growth in employment and the growth in personal income.” Sound familiar? Not one year later, the Case Shiller plunged over 30%.

You’ve misrepresented the article you reference. The author of the article, Toddi Gutner, did not make what you claim was her main argument. It was made by an analyst interviewed the author. The interviewee was also quoted as saying “I don’t expect the housing prices to fall in 2006.” Well, guess what, the big drop happened in 2007, not in 2006. And who cares if there is a 10-year-old interview subtitled “analyst Michael Youngblood explains his unusually optimistic take on the real estate market”? Sheesh the first sentence of the article is “Type the words “falling housing prices” into Google and more than 8 million citations pop up.” Look if you can’t even represent your own references or the history correctly, why should any of us expect you can forecast the future?

FWIW, I had plenty of conversations in 2005 and 2006 with people about how the liar loans and prices were unsustainable. I knew people that sold before prices peaked to be in cash. That was an obvious bubble and not something that “no one could have predicted….” — many people did predict it. I also had similar conversations in 1998-9 wrt to the stock market. So what?

Real per capita income is up in SF. If it wasn’t then we couldn’t pay as much for housing. If real per capita income declines in SF, like it did in the three recessions since I’ve lived in this area, then housing prices will decline, like they have in the three recessions since I’ve lived in this area. Clear enough?

Correlation does not equal causation. Home prices may dip along with salaries but it will come from a deflationary shock to the system. These relatively minor changes in employment, wages, or new construction supply that we are always going on and on about will do practically nothing to bring down SF RE values. Rents yes, but not prices. Just as in 2006, the problem today is low interest rates, the loose money is just flowing in different channels today.

Saying “Correlation does not equal causation” is not an argument, it is just another avoidance.

There is definitely a risk of deflation in the US. It has been happening in other major economies and could bleed over here.

Aside from potential global impacts, the SF Bay Area takes in as much VC money as New England, the NYC metro, and SoCal combined, year after year after year. It is far out-of-proportion to our economy as a whole. That’s the spigot that gooses our local employment and RE market on a scale unlike other areas. And the VCs can turn it on and off very quickly. That is what we are most sensitive to and what caused our booms (and subsequent busts) of the late 1980s and late 1990s. The tightening of the IPO window ~2 years ago somewhat dampened SF job growth and RE price growth over the past year plus.

“The real reason SF has higher RE prices now than in 2000, inflation adjusted, would seem to be more correlated with being richer and having a higher proportion of income available to spend on housing”

Again, correlation…. Again, this could only be true if the incomes were high enough to actually afford the homes here, which most aren’t. Again, only around 15% of SF residents can afford the median home, while 37% of homes are bought with all cash. The larger driving force is not salaries sorry. Want to make homes more affordable? The best bang for your buck is probably to pass a tax on foreign buyers. Nobody REALLY wants to make homes more affordable though.

Sabbie, you’re mixing up denominators in your numbers. Even accepting for the sake of argument your “37% all cash” number, 37% of the ~8000 SF homes sold in a year is about 3000 “all cash” sales a year. But 15% of the 837,000 SF residents is about 125,000 residents who can afford the median-priced home at today’s prices. I.e. those 125,000 are from households with high enough salaries to be able to afford SF homes even at today’s prices. It is not all that astonishing to me that a few thousand a year can, and do, pay all cash, especially with the influx of additional residents (100,000 more in the last 6 years), the huge infusion of VC and other money in the local economy, and rising SF incomes. And, sure, some number of those cash buys were from investors and foreigners and second home buyers, making that 37% figure even less remarkable. No real news there.

Anecdotally, I know 3 people who have bought a home in SF in the last year – a partner of mine bought a house for his daughter (a schoolteacher); a friend who runs a mutual fund bought a new place; and a college friend who made a ton of money on Facebook bought a home. Anecdotes do not establish broader trends, but this just illustrates the types of people who can an are paying cash in SF – it doesn’t have to come from shadowy foreigners.

JR

Add me to the list of those who bought all cash, albeit several years ago. For those of a certain age, all cash makes sense if one has been successful (or lucky) and don’t need the deduction. I’ve not seen any statistics on this, but empty-nesters downsizing or returning to the city from the suburbs may also play a part in the all cash phenomenon.

JR, I was not saying the cash sales are all shadowy foreigners, most of it does come by way of VC and finance. But there’s nothing we can do about that, that will only stop when (sorry if) the Fed ever raises interest rates. The foreign bit is something that we can control however. Also, of the 125,000 who can actually afford to buy a home in SF, don’t you think the vast majority of them have already bought homes? They are a much smaller part of the demand equation in that sense.

Yes, I suspect that most of the 125,000 in SF who can afford to buy a home have already bought one. But the number of homes sold each year in SF is so small that it only takes about 6% of the 125,000 to soak up every sale — far less if you consider the number bought by newcomers, investors, foreign buyers, and second home buyers. The supply is very small, and the demand is not so small – hence, high prices.

Where you and I agree is that this could change pretty quickly – tech market crash, political event like some hypothetical disastrous presidential election, etc. But I don’t see anything like that being a definite, or even likely, event in the near term. But the risk is not insignificant, which is why I’ve been warning would-be buyers to think hard about whether they could absorb a 10-15% loss.

The market of people to buy a home in SF is much larger than just the current residents of SF. About 5,000 people a month on average move into SF. About half of them from within the Bay Area. Something like a third of all home buyers are among these people that move into SF from somewhere else.

And the VC funding of tech companies is based on expected ROI with the emphasis on the multiples in the Returns. This isn’t just money looking for something better than bank interest rates. FWIW, the dotcom boom happened when there were much higher interest rates than now.

And Kriss Kross? Liked that (showing my age . . . and yours)

I’ve been seeing technical indicators for another leg up of the bull market beginning, nice to see that reflected in hiring and real action on the ground. It has been a good and refreshing pause.

Bull market in what? This is the only indicator that matters right now. Central banks propping up their equity bubble until after the election.

no links back to the several prior months’ socketsite “sky is falling” updates?

[Editor’s Note: If by “sky is falling” you mean an accurate accounting of what’s actually going on in the market, try the link we obviously buried in the second sentence above.]

I love how the Socketsite editor(s) call people out like this in the comments, always puts me in a good mood.

socketside has a perfect 1000-0 record for shooting down commenters. that’s because socketside just deletes comments for which they don’t have a snappy comeback.

Ugh… High school flashback. It’s horrifying to think Jump came out almost 25 years ago… Hell, even one of the Kriss Kross kids is dead… I made myself sad.

The miggidah-miggidah-MACK is my everyday uniform.

Since they – interns, that is – were called out by name, do UNpaid interns count in the “having a job” category?

Maybe many new graduates are starting new jobs in July?

Is the bay area economy suddenly heating up from the slowdown? Or is there any change in statistics methodology?