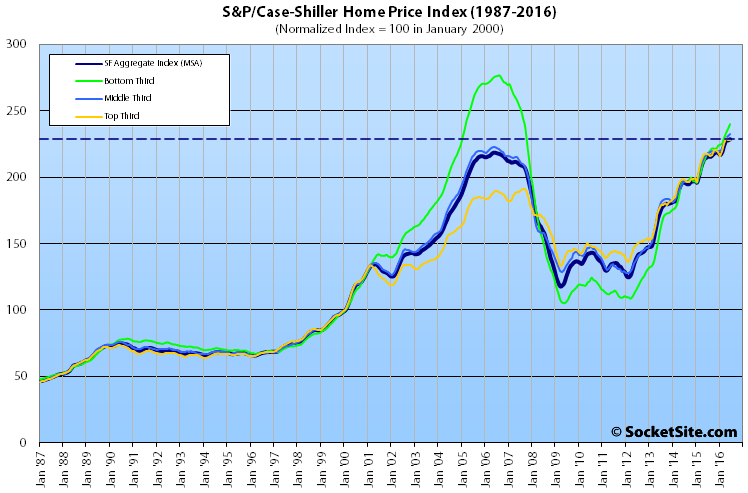

Having effectively stalled in May, the Case-Shiller Index for single-family home values within the San Francisco Metropolitan Area ticked up 0.4 percent in June to a record high, surpassing the previous cycle peak recorded in May of 2006 by 4.6 percent.

At the same time, the year-over-year gain for the index, the pace of which has been on the decline since the third quarter of 2015, measured 6.4 percent in June, the lowest year-over-year gain since the third quarter of 2012. And for the first time since early 2012, the index for Bay Area condo values dropped over a percent as compared to the month before.

The aggregate index bump for San Francisco single-family home values in June was driven by a 1.3 percent month-over-month gain at the bottom third of the market which is now running 10.7 percent higher versus the same time last year and has more than doubled since bottoming in 2009, but it remains 13.0 percent below its 2006 peak.

The middle third of the market gained 0.6 percent in June, is running 7.3 percent higher versus the same time last year, has gained 82 percent since 2009 and is now 4.4 percent above its 2006-era peak.

And while the index for the top-third of the Bay Area market remains 19.3 percent above its previous cycle peak recorded in August 2007, it was unchanged June having slipped in May and its year-over-year gain of 4.9 percent remains the lowest on record since the third quarter of 2012.

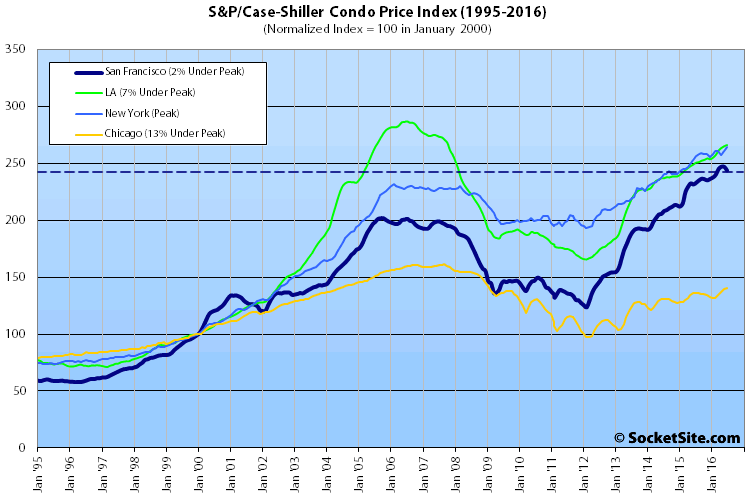

The index for San Francisco condo values dropped 1.3 percent in June, the first month-over-month drop of over a percent since the first quarter of 2012. The index remains 20.7 percent higher than its previous cycle peak in October of 2005, but the year-over-year in June slipped to 5.4 percent, the smallest year-over-year gain since the second quarter of 2012.

The index for home prices across the nation ticked up 1.0 percent from May to June and is now within 1.2 percent of its July 2006 peak and the index’s year-over-year gain ticked up to 5.1 percent.

And for the fourth month in a row, Portland, Seattle and Denver reported the highest year-over-year gains, up 12.6 percent, 11.0 percent and 9.2 percent respectively.

Our standard SocketSite S&P/Case-Shiller footnote: The S&P/Case-Shiller home price indices include San Francisco, San Mateo, Marin, Contra Costa and Alameda in the “San Francisco” index (i.e., greater MSA) and are imperfect in factoring out changes in property values due to improvements versus appreciation (although they try their best).

So, consecutive new record highs from February to June of this year. Maybe one will be reflected in July data.

In the face of the tech pullback that has been widely-reported, fairly pretty impressive price stability in (Case Shiller index) housing prices.

Perhaps because there is no tech “pullback”. There’s a slowdown in venture funding, but Google, Facebook, and Salesforce are at near record highs. Apple is down a bit from a year ago but up over the last six months. The drivers of the bay area tech economy are doing fine.

Yeah, the tech pull back is just trimming some fat. People here love to talk about a tech pull back like it’s around the corner.

I work for a start up – we’re expanding still and seeing rising profits. We are making double this year than just 1-2 years ago. And, I’m not talking 100,000 to 200,000 dollars; I’m talking.. over $100 mill+.

I honestly think all you’re seeing is supply vs. demand happening. Some people can’t buy into the $1M barrier houses, (and people just have to save up 2-3 more years with their spouse to make that downpayment) and not to mention, more and more condos are coming online.

Curious, does your startup sell to consumers or other companies?

Consumers.

Also, I think soccermom hit it dead-on with the article below.

Startups are basically looking to trim fat, reduce excessive costs. ie. Dropbox got rid of the “unlimited friends and drinking” perk in order to save $20k/person a year. IMO, what the public is perceiving as a major down-turn because they see an embellished article (love that click-bait) of layoffs isn’t really so.

The goal right now is to survive and grow during the hard times. Those that do will become stronger and more desirable to future rounds of funding and going public. It will be easier to invest in these companies when you know they’ve survived just fine during a down turn. Their valuations will grow and be bigger as a result. There is a term already coined for those start ups: “water bears”.

“Evernote is not valued at $1 billion because our business is worth $1 billion today, but because it could be worth $100 billion in a few years.” —Phil Libin

Phil Libin being the former CEO of Evernote, the company referred to in soccermom’s article.

And similarly, many condo’s aren’t valued at $1M because people think their current worth is $1M, but because people believe they will be worth $1.6M in a few years.

I think it’s far fetched to think 1M condos will be worth 1.6M “in a few years”, same goes for ever note being 1B now and 100B in a “few years”.

I think the next “few years” will have 10-15% off condo prices, low building growth followed by stabilization…. then growth.

And when the general consensus becomes that valuations for $1B startups and $1M condo’s are far fetched, what level do you stabilize at?

A more common name for your “water bear” strategy is the cockroach strategy. And the kicker with that is that even if you succeed, you still end up as a cockroach.

People would pay top dollar to ride a unicorn. But can you support current valuations, salaries and high but declining condo prices with a jar of cockroaches?

startups shouldn’t have excess expenses to trim. Their flab was bought with their own equity in most cases. Very pricey lard.

That Dropbox and some other private pre-profit companies need ‘dieting’ is a sign of mismanagement that was indulged by the froth of a few years ago that inflicted some truly lame IPOs on the market. It’s well known that the IPO/exit windows tightened since then forcing many of these pre-profit companies to stretch their cash else take down rounds or guarantee returns or find buyers.

All good for herd health: “bulls make money, bears make money, pigs get slaughtered”

Acknowledging that both “tech” and “pullback” are terms cast a wide net, an article like this one from Sunday’s NYT speaks to the broad trend I had in mind. But then, if everyone thinks a “crash” (their word) is coming and adjusts, maybe there’s no crash.

Maybe house prices will keep ratcheting up gradually, too.

The 2007 housing bubble was the biggest this country has ever seen and there was still a 2+ year period of stability around the top before the decline began in earnest.

The key to look for now is a clear turn from growth to flatness and what happens to demand once flat growth becomes the norm.

And the same goes for startups, cutting back and laying people off is the easy part. Getting to a profit and particularly a profit sufficient to justify prior lofty valuations once you are no longer a “growth story” is the hard part.

And sometimes a slow down is just a slow down– flat growth followed by modest growth– no jolting recession, no schmession. I personally think some people are suffering from PRSD– Post Recession Stress Disorder. Sometimes a pipe is just a pipe folks.