The Board of Supervisors postponed a vote on Supervisor Avalos’ amended “just cause” eviction protection legislation yesterday as the Mayoral veto of the original supervisor approved legislation survived.

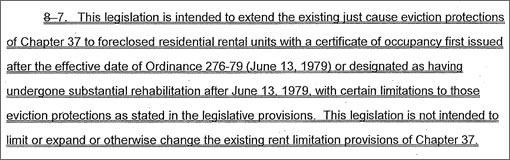

The amended legislation now intends to extend just cause eviction rights only to non-rent controlled residential rental buildings which have been foreclosed upon, because then nobody gets penalized except the big bad banks.

And hey, what are they going to do, raise their rates to offset the added risk?

∙ Amended Just Cause Eviction Protection Amendment [sfbos.org]

∙ Just Cause Or Rather Not: Mayor Newsom Vetoes Legislation [SocketSite]

∙ Just Cause Eviction Extension Approved, But With Four Key No Votes [SocketSite]

I doubt this law will cause enough of an impact to raise rental rates city-wide. I mean . . . the big bad bank owners will still be getting rental income on the property and it would have been rent-controlled anyway. Plus, we are going through a historic period of declining rents. This law will not have a big effect.

Plus, there are a good number of renters that are getting screwed while some homedebtors come out of foreclosure better off than before.

In fact, I think the law should be expanded to include single family homes because that is where the fraud is occurring and where some renters are being screwed over by deadbeat homedebtors and their banking and government enablers. As President Hopey Changey has said–the federal government policy is to make home prices go up and to bail out the deadbeat losers that overpaid for housing. Renters have gotten no protection. If we really wanted to help deadbeat homedebtors we would let foreclosure happen quickly and let house prices fall and then give the ex deadbeat homedebtors a voucher to use for rent if they were in dire need.

Deadbeat homedebtors bought houses they couldn’t afford with little money down and now are trying to rent out. They have been underwater so they stop paying their mortgage and take a renter in. And hey, some of them might be honest and rent first and then simply are unable to keep up with the mortgage and have to stop payment. Maybe some of them inform their renters they are in financial turmoil and are taking a renter in for life support. After all, renters are providing the main income for some deadbeat homedebtors now. But I bet the majority of deadbeat “owners” simply pocket the money and don’t inform the renters.

The poor renter currently has no recourse against the deadbeat home “owner” who has been pocketing the rent money and saving up a bundle on the house he “owns” while he fails to pay his mortgage obligations. The renter can get kicked out on short notice when he still has property rights under the lease and he’s the only one that’s been paying on the house! Meanwhile, both homedeboter and bank have been getting welfare and mucho government protection. In fact, us taxpayers have bought many of these mortgages and bailed both the loser homedebtor and the banks..

I want a law that really puts the screws to the banks and deadbeat owners. They should require a landlord to inform a renter when he has missed a payment to the bank. A renter should not be forced to pay rent when a deadbeat homedebtor hasn’t paid his mortgage.

I’ve seen numerous instances of deadbeat homedebtors engaging in these shenanigans in the Bay Area. If you are a renting a home in San Francisco make sure to get a credit report on you potential landlord!

“If you are a renting a home in San Francisco make sure to get a credit report on you potential landlord!”

yeah, sure. good luck with that. everytime i show one of my units i’m still getting lots of turnout. the rents are still quite a bit higher than 2-3 years ago. as usual, the landlord has the upper hand.

kid char,

You’re probably right landlords still have the upper hand in general–as evidenced by the government going out of it’s way to give welfare to “owners” and very few protections or welfare going to renters. San Francisco might be one governmental entity where slightly more attention is paid to renters.

And landlords, even deadbeat homedebtor landlords, might fool themselves into thinking they’re something special because they “own” a home and therefore get to call the shots when entering into a lease agreement.

But you’re absolutely wrong about rents. Rents are falling in San Francisco. Your anecdote may be correct that you are still getting good turnouts and getting more in rent than 2 or 3 years ago–but that flies in the face of the statistics I’ve seen and the anecdotal evidence I’ve seen. The statistics show rents DECREASING. I think you are engaging in wishful thinking.

Here’s a snapshot of rents in Noe Valley which show a significant decrease over the last year or so. http://noevalleyvoice.com/2009/December-January/Cost.htm If rents are higher than they were 2 to 3 years ago, as you claim, they would be higher in Noe Valley. Rents are DOWN in Noe Valley and throughout all of San Francisco.

Which gives renters more power.

As far as investigating a landlord’s financial situation . . . smart renters will do it. I would either ask for a credit report or do some sort of investigation to ensure the landlord is not a landlord because he’s underwater on his home and needs to make money off of the next sucker. I don’t want to rent a house I plan on being in with my family for 3 to 5 years only to get evicted because of a deadbeat landlord. I would tread carefully if I see a new landlord that is desperate to rent or has just moved out of their primary residence and is now letting it out.

I would probably insist on a clause in the lease that says I get notice if the landlord doesn’t pay the mortgage and I don’t have to pay rent in that case. I bet many landlords would agree to that clause because most honest ones don’t want to collect rent and then not pay the mortgage.

Of course, there are also laws that currently prevent an “owner” from stopping payment on the mortgage and receiving rent if this occurs within the first few months after the purchase of the house.

SFHawkGuy – good ideas on paper but good luck finding a landlord that doesn’t laugh in your face and refuse to deal with you once you start asking for information so you can check into their finances.

That kind of due diligence is standard in commercial real estate but I’ve never seen it in the residential market and I doubt many residential landlords would tolerate it.

“I would probably insist on a clause in the lease that says I get notice if the landlord doesn’t pay the mortgage and I don’t have to pay rent in that case.”

Good luck with that, SFHawkguy. I’ll see you in Xanadu with the Purple People Eater riding my unicorn.

Eric,

You’re probably right it’s too much change from current practices and most landlords would not want to negotiate beyond the standard terms. I guess one has to be willing to walk away with one’s rental money until one finds a landlord under the right terms. Although, on higher priced single family homes it may be prudent to shop around and negotiate to screen and investigate landlords. It’s what I plan on doing in the near future.

I will probably only go as far as asking for a credit report if I se a number of red flags.

For instance:

Say I want to rent a SFH for ~ $2500-$3500 in the East Bay. If I see a home in Berkeley for rent, for e.g., and the home was purchased in 2004 for $650,000, and now the owner/prospective landlord tells me he’s moving into a smaller place because he’s downsizing and had to let go of his other “investment” property so he’s only going to be renting out this place . . . I would be worried. Then I would want to know what his job is . . . . and if I found out he worked in an “average” job then I would be even more worried. Of course I would also look for court records to see if the landlord has been sued on any debt, etc.

I may only inquire further if I see some red flags. If the landlord has owned the place for 25 years then I will be less compelled to investigate. Asking for a credit report would only happen if a number of warning signs were present.

And frankly, there might be a situation that renting from a deadbeat homedebtor that is on the brink of default might be a good thing. There will presumably be cheaper rent because the landlord needs the money and he’s not paying the mortgage anyway so he needs to get any sort of rent as soon as possible. I would also expect a few months of free rent once I found out the deadbeat owner has stopped payment on his mortgage (at least when the notice of default is filed) and before I get evicted. A deadbeat landlord is not likely to sue for a couple of months of rent when he himself isn’t paying the mortgage. And, I may get the money for the keys that usually goes to the “owner”.

Anyway, there are lots of deadbeat landlords or potential landlords out there and it’s prudent to make sure one’s rental home isn’t going to be ripped out from under them because of these deadbeat speculators.

Wonder if this will lead to banks adding no-leasing clauses to their mortgage contracts.

It’s not rental rates that would go up because of this, but mortgage rates in San Francisco. Either banks will raise their rates due to higher risk, or some banks will pull out of loaning in SF completely, thereby reducing competition, which would result in higher mortgage rates.

It makes little sense to me why a lease can be broken merely because the form of a change in ownership is a foreclosure instead of a purchase.

Banks should step into the shoes of the landlord during a foreclosure. If you are renting and are half-way through a year lease, the bank should be held to that year lease and nothing more.

Of course, a bank can break the lease and the renter can take it to small claims court.

SFHawkguy — definitely makes sense to do your due diligence. I definitely ran across rentals in recent years where it was pretty clear the owners were distressed, and some of them ended up as short sales/foreclosure.

Most everyone should check SFR rentals on Redfin at least, if nothing else. You can also check tax records to see if there are delinquencies.

What’s most suspicious is when the deposit seems to be what a mortgage payment would be based on the last sale, but the actual monthly rent is $2000 less. I saw that a lot — even if the house isn’t foreclosed upon, good luck getting your deposit back.

Anyway, if the landlord gets NODs, you may see them on the house itself. If you have reason to know the landlord isn’t paying the mortgage, most people would recommend not paying the rent — what are they going to do, evict you?

The best story was a friend of mine who found a nice place on Craigslist and was asked to use the key in the mailbox to open the side door to check the place out (key only works for side door, not front door). Turns out the house had already been foreclosed on, and it was just some dude down the street trying to defraud people.

“It makes little sense to me why a lease can be broken merely because the form of a change in ownership is a foreclosure instead of a purchase.

Banks should step into the shoes of the landlord during a foreclosure. If you are renting and are half-way through a year lease, the bank should be held to that year lease and nothing more.”

That’s not how the law works. The policy difference with respect to foreclosure is partly because a foreclosure sale doesn’t allow as much due diligence for the new buyer, but historically banks weren’t typically the principal buyers of foreclosed houses.

This provision will lower the price of all foreclosed properties in SF, producing great comps. And you may see higher mortgage rates in SF County too due to the extra risk, which would put further pressure on housing prices.

Economic forces will often influence the behavior of individuals or groups.

During the height of the dotcom boom, potential tenants were put through absurd selection processes that would have been considered intolerable or fantastical just a few years previous (and after). Why? Because demand overwhelmed supply and landlords had a heavy upper hand in negotiations.

If supply overwhelms demand (don’t think we’re there yet, but it’s trending that way), and potential tenants have a heavy upper hand in negotiations, why wouldn’t we expect landlords to submit to practices that they would have scoffed at previously? They do need to rent the place out, after all.

I’m not saying that the idea above will become standard practice, but to dismiss it as intolerable or fantastical misses the behavioral point.

“This provision will lower the price of all foreclosed properties” –> should say “all foreclosed rentals, not properties

First they came for the foreclosures then they came for me.

A toe in the door for rent control on all property in SF. Be afraid be…very afraid…but then what the heck when rents turn around…and they will…you will have no one to blame but the man in the mirror for the high cost of living in SF if you allow this to pass.

U keep screwing landlords, we keep raising rents to justify risk. There are always going to be consequences to takings…pay me now…or pay me later…but you will pay for my risk.

A state law terminates leases upon foreclosure.

A state law overrules any city law.

So this city law would have no effect once it winds through the courts. I’d give it all of about a year before it goes poof.

I think the tenant gets 60 days notice (up from 30!) until 2012.

http://www.ktvu.com/download/2008/1017/17737405.pdf

@anon at February 10, 2010 11:51 AM

I agree, that’s how the law works. I don’t agree that’s how the law should work.

Currently, the tenant is treated as an unsecured creditor in the quasi-bankruptcy that is a foreclosure. The tenant’s contract is terminated and they have absolutely no recourse. That’s ridiculous. As many people point out in this thread, there is absolutely no practical way for a tenant to protect themself.

While a potential buyer may have limited time for due diligence, they are in a far better position than potential tenants to do the same. It is unfair to burden the tenant with the loss of a lease breach when they are the least able to account for the risk.

“g” wrote:

It doesn’t matter if it does, because barring the banks or mortgage servicers employing an army of private investigators to verify that the mortgaged property isn’t being leased, there is no way to enforce such a clause, and therefore it’ll be useless in practice.

Huge numbers of amateur, “bootleg” landlords in The City have mortgages that presume the property will be owner-occupied, because the interest rate on such a loan is lower than it would be for a commerical property. The prospect of being criminally prosecuted for mortgage fraud doesn’t stop them, and neither would a flimsy clause in a mortgage contract.

Sure glad I’m not a tenant in one of the Lembi-related units.

They just filed for bankruptcy: http://www.jdsupra.com/post/documentViewer.aspx?fid=fbcbfdd4-9bc7-4970-ba04-c8f4a744c8bc

Interesting they do not list the tenants as creditors–maybe the management company takes the security deposit and is the creditor?

Tenants have to be careful about losing a security deposit or prepayment of rent in a bankruptcy.

“While a potential buyer may have limited time for due diligence, they are in a far better position than potential tenants to do the same. It is unfair to burden the tenant with the loss of a lease breach when they are the least able to account for the risk.”

That’s not really true. If you’re at the point of foreclosure, the renter has had at least 6 months (if not 9 or 12 or 15 or more) of notice that the property is being foreclosed upon. The renter should have done due diligence earlier and certainly has time to figure out what’s going on during the foreclosure process. The renter has *plenty* of time to find a new place and move, which is the only proper recourse here. What’s the rationale for allowing renters to stay, other than “moving sucks”?

There’s no way in hell these places should be rent-controlled just because they were foreclosed upon. The rationale behind foreclosure (and bankruptcy for that matter) is more efficient use of assets and to provide the former asset holder a clean slate. The renter has no claim on an asset here and shouldn’t be above a would-be secured creditor here. Allowing renters to stay makes it difficult to redeploy the asset.

I’m sorry, the tenant is the only one in the whole sorry cast of characters that isn’t gaming the system or getting welfare. The tenant is providing the best use–he’s living in a home he can afford and paying the rent! Unlike the deadbeat homedebtors and crony-capitalist bankers that have been gaming the system and are bleeding the taxpayers dry.

If the law favored the best use of the property then current tenants paying fair market rates would be allowed to live out their lease terms.

Um, how in the world, if a tenant is in a situation where the mortgagor is renting out the property to try to extract money from it in the face of an inevitable foreclosure, going to get “notice that the property is being foreclosed upon” unless they are a real estate agent or something like that? Is every renter in The City supposed to read and keep abreast of the legal notices printed in the paper to see if the address where they are currently living shows up? Underwater landlords tend to have the mail forwarded to another address, so the renter isn’t necessarily going to see the default notices that the mortgage lender or a trustee is sending. That’s the context of the legislation under discussion. The underwater landlord has every financial incentive to hide the fact that they are being foreclosed upon, and some do quite a good job at it.

That isn’t what the President said. Using the bubble bust as an excuse to get mean and political is super lame.

hey hawkie,

b/c rent control constrains the supply of available rental units you can bet that you will not find a large inventory of nice units at any one time. the good places (w/good nabe,light,views,amenities) are held onto while the crappy ones come up over and over. after you’ve toured lots of awful AND expensive units you’ll see how quick you are to jump when a good one comes around.

anyway, the scenario you fear (landlord collecting rent but not paying mortgage)is not very likely in sf.

On the Lembi bankruptcy, my guess is that the bankruptcy code will trump local rent control laws, and when these companies (and their buildings) emerge from Chapter 11 or during the bankruptcy process they will be able to evict even rent-controlled or “protected” tenants.

A.T.,

Since the Lembi case is a Chapter 11 the company probably wants to reorganize rather than liquidate.

Therefore, my guess is the leases will continue to be in force even when the company comes through bankruptcy. I imagine the company wants to come out of bankruptcy with the same management, the same buildings, and the same leases.

Theoretically, the court or trustee could decide to sell the buildings and then I don’t know what would happen to the leases.

Generally in bankruptcy the debtor gets to affirm whatever contracts (e.g. leases) it wants and reject all others, even in a Chapter 11, which means reorg not liquidation. That way the company emerges from bankruptcy w/o the unfavorable contracts/leases. I don’t see why the debtor here wouldn’t want to reject leases for rent-controlled tenants that have crummy terms.

So the debtor can pick and choose which leases it affirms and come through bk not subject to rent control and other eviction protections (or at least get a short exemption)?

Since bankruptcy law supersedes state and local law, does the debtor not then have to give 60 days notice to vacate either?

If a debtor does try to extinguish leases wouldn’t this act be a breach which resulting in damages and therefore wouldn’t these tenants become creditors? I’m assuming these people have security deposits as well.

So you’re saying a judge is going to approve a plan where the tenants get wiped out as creditors and the new management (probably same as the old management) is allowed to violate local and state housing laws to breach leases and evict tenants?

“Um, how in the world, if a tenant is in a situation where the mortgagor is renting out the property to try to extract money from it in the face of an inevitable foreclosure, going to get ‘notice that the property is being foreclosed upon’ unless they are a real estate agent or something like that?”

In California, just file a Request for Copy of Notice of Default with the recorder under Civil Code 2924b:

http://law.onecle.com/california/civil/2924b.html

In California *anyone* can request notice of default.

SFHawkguy, bankruptcy lets you do many, many things that would subject you to big damages claims outside of bankruptcy. Yes, the general rule is that the debtor in bankruptcy can simply cancel any leases or contracts it wants to, and not cancel those it does not. Retailers do this all the time. They enter bankruptcy, cancel the bad leases they signed with shopping center owners (but keep the good ones) and then re-emerge operating only in the good locations. The counter-parties to the leases do not then become creditors; they are out of luck. The judge does not have to approve, and cannot disallow, these decisions. It is a statutory right under the bankruptcy code.

I do not know if there is some specific provision dealing with real property leases that is different, nor do I know how rent control figures in. But, as you mention, the general rule is that the bankruptcy code trumps any state or local laws. I’m curious whether this is a component of the Lembis’ strategy.

Thanks for the input A.T.

I guess I’m still confused. I see that 11 U.S.C. section 365 pretty much covers this situation; unexpired leases. It’s a little too complicated for me to figure out on a first reading though.

But in general, I guess Lembi will be the debtor in possession which will give them the same rights as a trustee when it comes to administering the estate. Specifically, the debtor will be able to use, sale, or lease the property, per section 363. And as you point out A.T., the debtor in possession can assume or reject unexpired leases pursuant to section 365 (notice the special rule for shopping centers).

However, I don’t see how the trustee/DIP has the power to violate local housing laws when managing the estate. I knew state and local proceedings would be stayed . . . say a tenant wanted to protest an eviction by the debtor in possession . . . he wouldn’t be able to stop it in his local court but would have to go into bankruptcy court. But I didn’t know the trustee was basically lawless. Say the trustee/DIP thinks the most economical use for these properties are as slaughterhouses and tanneries. Can he violate the local zoning and animal cruelty laws because he’s in bankruptcy court?

And the judge would have to approve a plan. Also, right in the first sentence of section 365(a), it states that the trustee (and DIP) can only assume or reject contracts “subject to the court’s approval . . . .”

Plus, other interested parties could file a motion and seek judicial review.

Anyway, probably sucks for the tenants. I’m interested in getting a fuller picture and hope to see some reporting on this. This has to effect a lot of people I would think.

Thanks for your input and let me know what I’m missing and how the trustee can violate rent control and other laws . . . I’m interested.

SFHawkguy, hey, I’m just a forensic accountant. I’ve worked on a lot of bankruptcy matters but I do not know the ins and outs of the law, although I work with lawyers a lot. As a general matter, a debtor in bankruptcy can reject ANY lease to which it is a party. The judge’s review of assumed or rejected leases under the code is almost nil. With no lease, the tenant has no right to be in the place, and one would think the U.S. Code would trump some local ordinance that says “no, the tenant gets to stay anyway.” But maybe I’m wrong. I have a hunch the Lembis, knowing what they are like, might test these issues as “they” (the post-bankruptcy owners) will have MUCH more valuable properties if the rent-controlled tenants are out.

anon, thanks for setting me straight about getting a notice of default.

I wish I would have known about Civil Code 2924b when I was younger, it’s too late to help me now since my current lease is going to expire and I don’t plan on renting again for the rest of my life, but I’ll pass that information on to my friends who have sketchy landlords. Good info to have.

And A.T. and SFHawkguy, conflict of laws cases are always lots of fun; I expect that if the Lembis try to use bankruptcy court to get large numbers of rent-controlled tenants evicted that some young attorney associated with The Tenants Union or somesuch will take up the case just to be in a position to “make law”.

Supervisor Avalos’ amended legislation that grants “just cause” eviction protection to buildings which have been foreclosed upon was approved by the Board of Supervisors on Tuesday (3/9/10).