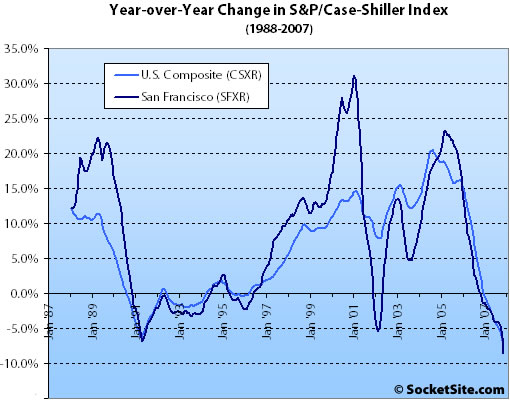

According to the November 2007 S&P/Case-Shiller Home Price Index (pdf), single-family home prices in the San Francisco MSA fell 3.2% from October ’07 to November ’07 and are down 8.6% year-over-year. For the broader 10-City composite (CSXR), year-over-year price growth is down 8.4% (having fallen 2.2% from October).

Miami remains the weakest market, reporting a double-digit annual decline of 15.1%. San Diego followed with -13.4%, Las Vegas with -13.2% and Detroit with –13.0%. Seven of the metro areas are now posting double digit declines in their annual growth rates. Charlotte, Portland and Seattle are the only three MSAs still experiencing positive annual growth rates.

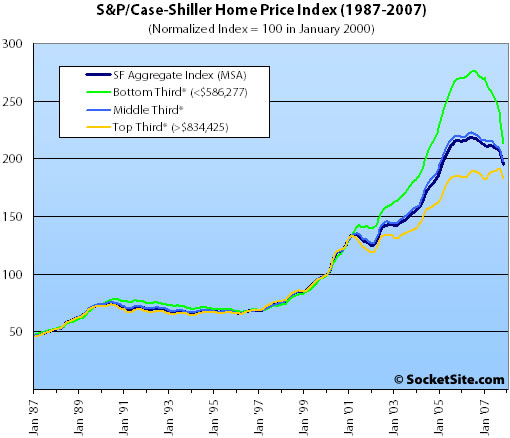

Prices fell across all three price tiers for the San Francisco MSA with the rate of decline leveling off for the lower two-thirds of homes but accelerating at the top.

The bottom third (under $586,277 at the time of acquisition) fell 5.3% from September to October (down 21.3% YOY); the middle third fell 2.5% from September to October (down 8.5% YOY); and the top third (over $834,425 at the time of acquisition) fell 3.1% from September to October (down 1.6% YOY).

The standard SocketSite S&P/Case-Shiller footnote: The HPI only tracks single-family homes (not condominiums which represent half the transactions in San Francisco), is imperfect in factoring out changes in property values due to improvements versus actual market appreciation (although they try their best), and includes San Francisco, San Mateo, Marin, Contra Costa, and Alameda in the “San Francisco” index (i.e., the greater MSA).

∙ Record Declines in Home Prices Continue in November (pdf) [Standard&Poor’s]

∙ October S&P/Case-Shiller: San Francisco MSA And Price Tiers Fall [SocketSite]

Everyone who believes prices are still rising in SF, please raise your hands…!

We can grow to the sky!

raise both hands

Something is going on here. We just don’t know what yet.

I think in some districts and neighborhoods in San Francisco, prices are indeed declining. But in others prices are still rising and I honestly don’t think we’ll see a significant change in that trend at all. Especially when you factor in the point that these figures are also pulling in numbers from San Mateo, Contra Costa, and Alameda Counties. So I guess I will raise just one hand for now.

Tell me, oh ghost of flujs past. Are these visions of things which will be or only of what might be? Tell me there is still time to turn aside from the dark fate which has been revealed!

All I can do is show you guys what the MLS says. If you choose to dismiss the numbers for SFR sales so far this year versus SFR sales for the equivalent time period last year, that’s entirely up to you. But 50 billionth time, the SF MSA is not equivalent to San Francisco proper.

Here, and this time I included District 10:

1/1/8 – 1/29/8 SFRs:

78 sales, DOM 61, avg price $1,208,526, $psqft 645

1/1/7 1/29/7

128 sales, 59DOM, $1,028,526 , $psqft 576

Here are the numbers YoY for that fabled whipping boy neighborhood of S.S. infamy, the Sunset District. You know, the part of town that has “already seen change.”

’07 — 18 sales, 53 DOM, 859,753, 501 psqft

’08 — 17 sales, 54 DOM, 849,552, 550 psqft

Looks kinda samey, don’t it?

Don’t worry. They’re battening down the hatches in CoCo.

The YOY January decline in sales volume fluj posts is quite astounding. I suspect these price declines will only further accelerate given the incredible slowdown in demand, particularly noteworthy given that inventories are up over early 2007.

Of course, CSI controls for differences in the mix and compares apples to apples, whereas MLS average price information does none of that.

Yeah well District 10 ’07 outsold District 10 ’08 43 to 12 YoY for this year so far to last.

That basically goes along with what some of us have been saying, ad nauseum, for quite some time. Do factor that number, 31, into your “astounding” appreciation of sales volume decrease. You know, whilst seizing upon one aspect of the numbers I provide and dismissing all other aspects of the numbers I provide.

Did I miss something? Why are there so many flujs now?

Movin’ on up to the East Bay.

Just saw a REO listed at $400K, 4 BR, 2.5 BA in a decent neighborhood, with a decent school. Oaktown is in da house.

Oh yeah, last sold in 2006 for…drum roll…

$800,000!

heh.

The number of REOs in parts of Oakland is astounding. Prices are going to fall a lot further there imo.

@David: address please so the rest of us may take a look?

Not trying to threadjack, but speaking of REOs, you guys might want to check out http://www.foreclosureradar.com. A similar slant to PropertyShark, but it tracks properties in all stages of default, provides lenders and payoffs, and covers all of California. It was mentioned in the recent 60 Minutes piece “House of Cards.” Even I was surprised at how many distressed properties there were in the city and bay area (including “prime” areas of SF, Orinda and Lafayette, Marin, etc.).

Quick question:

Let’s say a 20% price decline emerges, on average, for the city of San Francisco in the next 18 months.

Would any of the (frequent, repetitive) doomsday cheerleaders actually DO anything in that event?

… or is it a bit safer to stay behind the keyboard, where you’re the smartest person in the whole universe?

(for those with fearless predictions of an average of 50% declines across the city, please jump in despite your detachment from reality)

I’m waiting for the marginal cost of renting (i.e. the free-market rent for the unit today as opposed to what I actually pay which is less) to equal the cost of buying (with 100% financing) when all expenses and tax deductions are exactly factored in. That way I’m sure to get a fair rate of return on my 20% cash downpayment.

Either a sharp rise in rents (doubling, in my case) or a fall in prices or a combination of both will push me to buy.

To answer your question, amused, you can definitely count me in when buying makes more sense than renting on a purely economic basis. It currently does not, despite the modest price drops we’ve already seen in some areas of town.

When I’m financially better off buying with 20% down on a 30-year fixed mortgage than I am renting and investing the difference, I’ll jump in. And I factor all the variables into my comparison (taxes, maintenance, HOA, expected appreciation, etc.).

Then again, I’ve never predicted a 50% hit or any kind of ragnarok scenario, where we all “live off the fat of the land” like Lenny and George. My prediction has always been 15 to 20% down over 2-3 years. And I still think it’s realistic in ’08 and ’09. If it never happens, I can either move to the east bay or rent forever.

Amused,

foreclosures rising exponentially … check

bank REO inventories rising exponentially … check

fraction of homeowners underwater rising exponentially … check

reset waves coming … check

recession and job losses starting … check

credit tightening … check

One day SF real estate will be a great investment. But not today, and not at 20% off.

“Quick question:

Let’s say a 20% price decline emerges, on average, for the city of San Francisco in the next 18 months.

Would any of the (frequent, repetitive) doomsday cheerleaders actually DO anything in that event?”

Good question: Currently, the condos that seem to interest me most are 2bdr 2ba that are somehow being listed for 950K- 1.2M. I am currently renting a comparable nice 1250 sq ft 2bdr 2ba with parking and laundry in the heart of pac heights for $2150, so buying now is certainly out of the question.

If the market goes down 20% aross the board, the places I am interested in would still be be 760K- 960K. i could afford that range, but renting my comparable apt. would still be half as much per month, so 20% less would probably still be a no go for me. Personally, i think 20% less for these kind of properties is almost a given over the next 18 months.

at 30% less than current value, even though it would still be much higher than my current rent, i am pretty sure i would buy. But i would only buy when the market has popped up from its botton.

My personal estimate for the correction between now and Q1 2010 is between 20-35%.

For now, i am putting an additional $4k per month into investments for the next 18-36 months

I’m with the rest that say that the economics have to come closer in line between rent and buy before I jump in. I will put in a lifestyle factor so that it doesn’t quite have to be completely equal and also be sure to take on a total cost of ownership that remains comfortable. In today’s dollars that is probably more like a 20-30% drop overall for me.

Speaking of dollars…the falling value of our currency is ignored in this equation but I think we should all be building some consideration in for that. Makes my head spin.

One more…on the topic of the east bay. A co-worker just closed on a 3bd/2b SFH in Blackhawk/Danville at 35% less than the previous owner paid 18 months ago.

Amused, how about a little quid pro quo?

If you were currently renting, and had spent years saving and accumulating a six-figure down payment, would you bet it all to buy into today’s choppy market at today’s frothy prices, given everything that’s going on? Or would you wait a year or so, just to see how it all plays out?

Please indulge us, since it’s also easy to seem like the “smartest person in the whole universe” if you bought pre-bubble, back when it actually made financial sense. World is a different place today.

@amused: talk about sitting behind the keyboard thinking you’re the smartest person in the whole universe. get over yourself.

as others have said, the second it makes more economic sense for me to buy versus rent, or it will increase my quality of life, i will buy again. period. it won’t matter if the market is up, down or sideways.

Bye. I know I said I was out of here before. But this time I have a plan. I’m going to resurface in June or July. At that point in time I will either admit error if the market has changed by 10 percent or more, or I will ask for about six or seven others to admit error if it has not. As of right now market prices — as my Sunset numbers show — are largely the same for most parts of town, period. (And I am tired of arguing about it.)

Meanwhile, again, and as always, have fun storming the castle!

Amused, I certainly have not been a “cheerleader” for price declines, although I did shake my head in disgust as the bubble inflated and have taken a lot of gruff for even suggesting first that prices will return, and now that prices are returning, to earth a bit. What will people DO with a 20% price decline? Many will walk away and mail their keys to the bank as they will be hundreds of thousands of dollars underwater — this might hasten further declines. Many will continue to watch to see if prices decline even further. Some construction projects will be halted. Some who would otherwise sell will now choose not to sell. Some, maybe many, will enter the market to buy. It’s what you would expect.

Dude, et al –

I bought in July 2005. According to SS bylaws, that puts me in a two-digit IQ group. So there’s that bit of disclosure.

I was renting (for 15 years, post-college), spent years accumulating, put down a quarter of a million dollars (20%). In 2005, to be sure, there were also a number of naysayers.

I don’t regret my decision for a minute. I am on the record on this site of being tired of a) armchair economists, b) repetitive negativity, and c) pointless cheerleading. As I’ve said, I come here for design porn. It’s very voyeuristic on my part.

I don’t claim to be the smartest (never have), but my strong bet is that there are a lot of people here cheering the downward trend (which is happening) who couldn’t put a down payment on a Honda Civic. Not all. But a lot.

As for Dude’s question:

No one can time the market. I would buy now if I found exactly the right place, just as I did in 2005.

Despite the hopes of many, a 20% drop in desirable SF neighborhoods seems an unlikely scenario. And buy/rent will always be out of whack here.

As for toni’s post: I got bored and stopped reading after the first sentence. Can you paraphrase it for me?

“buy/rent will always be out of whack here.”

Maybe, but doubtful. The buy/rent equation being so out of whack is a very recent phenomenon. Even in the late 90s you could immediately come out ahead (after taxes) by buying. It got out of whack from the dramatic run-up in prices that is now seeing a pretty dramatic correction. It was driven by two phenomena that are now gone: (1) cheap money available to anyone with nothing down, and (2) the universals sense that prices will only appreciate. I’m no soothsayer, but the laws of economics are not meaningless.

Thank you for your candor, amused. My partner and I were close to buying in 2005 ourselves. But we (mostly I) got cold feet and decided to wait, and I subsequently became one of the naysayers you mention.

And to qualify my 15-20% down prediction: we’re not looking in the Marina or Noe Valley. The areas we’re looking at are probably not #1 on most people’s lists (i.e. Glen Park, Sunset). I still think we’ll see material drops in those areas and, with a large down payment, will get close to equivalent rents. But to those waiting for 50% drops city-wide….I agree that that may be a fool’s errand.

fluj – thanks for the good tidings. I’ll try not to let the knaves scald me with oil as I catapult over the ramparts. Before you go, please let us know how you define “the market.” We’ll need a pre-determined SF benchmark to track the market. Can’t use the S&P index, obviously, since it’s already down 10.5% from the peak set in May of 2006. Suggestions?

the only thing I am sure of….if SFO really goes down by 20%, nobody here would buy.

Just think about it. The SF MSA is down almost 10% right now, yet SFO is pretty flat. If SFO is down 20% at some point in the future, the SF MSA is at least down 40%, and some area will be down 60% to 70%.

What does that mean? As Satchel puts it – depression. A lot of people on SS (bulls or bears) won’t have jobs. Even those with jobs will be smart to wait. Actually, if we have a decpression, there will probably be wars, so some of us may not survive.

Excited about future? We will see.

Fluj, I wish you’d reconsider. Look back 8-12 months on this site and you’ll see lots of flaming and insults directed at anyone who even suggested that prices will come down around here. It would have been a shame if those voices had simply bowed out in response. I often disagree with your position (and very often agree with it) but you’ve kept the discussion well-rounded.

“buy/rent will always be out of whack here.”

Not a chance. Something, though, that is never brought up is that buy/rent ratios IMO are analogous to stock p/e ratios – the same ratio does not apply to all stocks in all sectors.

In housing, it would seem to me that the entry level places (1/1s, smaller SFHs in sketchy neighborhoods, etc.) should cost LESS to buy than rent. This is largely because there should be some return associated with capital scarcity. Not everyone has the employment prospects, discipline, etc. to save a downpayment or otherwise function as a creditworthy propsect for a lender, but everyone needs to live somewhere. Therefore, the people who have the ability to accumulate capital should be able to rent out the starter/less desirable units for a profit. This basic, commonsense notion was completely lost in the bubble, where literally no one faced capital constraints (even the banks – there was always some “Asian saver” or “European” to buy the toxic MBS). As the bubble deflates, look for these smaller properties to suffer the worst (and, incidentally, that is just what we are seeing in SF – only just starting, and it will get much worse).

As one moves up the scale of desirability, tax effects become more important, and a larger premium accrues to having a stable place to live for a longer period of time. Thus, nicer condos (2/2s,say) or modest houses in better neighborhoods should be closer to equivalent on a rent/buy basis. These properties and/or neighborhoods should have smaller relative adjustments as the bubble deflates, and in fact they probably did not go up as much on a relative basis than the crappier properties.

At the top end (mansions, the nicest neighborhoods, luxury 4/3 condos in prestige buildings, etc.), one would expect to be able to rent much more cheaply than buying. A buyer of a property like this places a premium on the stability of the living arrangement, and should be willing to pay for it accordingly. Additionally, there should be no benefits accruing to the ability to amass capital, as someone who rents one of these places is probably similarly wealthy to the one who owns it, or at least does not face severe capital constraints.

About the bubble deflating, 20% – or any figure – is sort of misleading IMO. Although there will of course be exceptions for individual properties and neighborhoods/situations, I think we are likely to see prices rolled back “by years”. That is prices will go back to where they were, say, in 2002 (not a real prediction – I’m still trying to get my hands around what is going on exactly). For some properties, this will be a 10-15% correction (many of the properties in nice parts of St. Francis for instance are only about 10-15% higher than in 2002), for others it will be a 50% decline (much of the Bayview, some of Bernal Heights, for instances). I don’t think there has ever been a bubble in history where prices did not deflate back to where they were (on a trend basis, and usually undershooting), and I don’t expect SF to be any different.

Did anyone catch the 60 Minutes piece on the housing market this past Sunday? It was pretty good, and all of the “on the ground” reporting was done from Stockton. One realtor has started a “repo tour” of all of the bank owned homes there. He runs two buses a week. The basic sentiment was that a new(ish) house in one of the new neighborhoods in Stockton can be had for as much as 70% less than in 2005. 70%! I know that prices are down easily 50% in much of the central valley like Fresno and Modesto- with huge inventory numbers.

The real estate crash has already happened in California. The fact that we can even debate what’s happening in S.F. is an indication that it is different here. How different is the ultimate question.

” And buy/rent will always be out of whack here.”

What is your basis for making this statement? They were in line prior to the late 90s. Should we trust the past 15yrs when the whole country was ina real estate bubble or the previous 90 years on record for San Francisco. Even 10 yrs ago, they were much more in line than now. The P/R ratios ahve been discussed ad nauseum on here and in national as well as local media. What so drastically changed about the SF in the past 10 yrs to make the P/R ratio no longer valid?

this argument sounds eerily familiar to irrational exuberance and the “new market” or “new ecomony” talk about the dot coms in 1999. At that time, people were saying P/E no longer matters, and we saw what happened.

Mortgage payment being double rents in SF is a new phenomenon and one that will revert back to the mean. the question is how long will it take?

satchel. great post. i agree on all points.

Well, I’m currently in the situation of moving back to SF and for the past (2) weeks I’ve done nothing but look at apartments for rent. The rent prices are insane, which I’m used to, and the places SUCK- which unfortunately I’m also used to seeing when trying to find an apartment in SF.

Regardless, it makes much more sense to me to spend just a bit more and buy a place. Those of you living in rent controlled apartments- sure, your situation is different. That’s not the perfect set-up either, as far as I’m concerned.

My point is that for some people it does make sense to buy, and I think there are probably quite a few of us out there looking.

Thou doth protest too much amused.

You only come here for the design porn but somehow get suckered into engaging the armchair economists in the comments? Let me guess, you’re an actual economist that is so amused you can’t help yourself from commenting? And you will learn these poor, rabble-rouser armchair economists that are secretly jealous and bitter of your superior wealth and judgment? That’s rich.

I am tempted to root against you just for the karmic justice in seeing you fall from your arrogant perch–but I will refrain–I can tell you are nervous about your own economic armchair decision. I would be too if I spent 15 years worth of savings betting on my analysis of a rosy housing market in the summer of 2006 (near the peak of a historic bubble). As you note, time will tell, but I detect a whiff of fear in your post.

Also, re the Honda Civic slur. Yes, you guys that borrow a lot of money to buy depreciating assets might put a down payment on a Honda Civic, or more appropriately, some underperforming overpriced car like a Lexus, but I bet a lot of the “bitter” renters would pay cash for a Civic rather than take a loan out or lease. Anyway, the Honda Civic seems practical to me so it’s not surprising that you associate that car with being a loser!

Wow.

Post something about buy/rent ratios and all of the people doing their Slim Pickens in Dr. Stranglelove impressions come out of the woodwork.

My “source” for this information was the chart right here on SS that indicated that SF’s equilibrium ratio is higher than in most other markets (42 something or other?).

No need to get all excited. As Satchel points out, the same P/E ratio does not apply to all stocks in all sectors.

I like fluj. He’s one of the few people here who backs up his rhetoric with data.

For a rational person, the price of a home is equal to its rental value, plus value inherent in ownership, plus (and this has been a big one) the net present value of the expected appreciation. That’s pretty much it. The differences among individuals are the value of owning the place, which is personal and emotional, and the expected value of the appreciation, which is unknowable, so people will be wrong – a lot.

Those of you who expect to buy at the rental value are missing the fact that for a large part of the population, real estate never goes down. If they expect it to rise indefinitely, they will pay more than you will. And some people just have to own stuff, so that value may be way different from yours.

The expected appreciation is falling and the inherent value of ownership, which had included using your home as an ATM and never really paying for it (via interest only loans, etc) is coming to an end. So values will fall.

But when people are able to buy more house for the same money, VERY FEW will buy the same house. They tend to buy as much house as they can convince a bank to give them. Thus, Fluj is correct: as people’s incomes rise, they will buy the most expensive house a bank will let them. Incomes have been rising and availability is still ow, so the fewer people buying may be spending more money. Mr. Case and Mr. Shiller are also correct: prices for the same home are falling.

When I bought my last TV, it was 1998, and I bought a 27 inch set for $800. I recently bought a 46″ LCD for $1600. Does that mean prices for TVs are rising? Nope. They fell. A lot. But I spent more. And lots of people are buying that size where no one bought that size in 1998. Median TV prices are up. Does that mean prices rose or fell? They fell. Got it? Prices can fall when medians rise. Fluj, you don’t have to take your marbles and go home just because people aren’t agreeing with you. You can BOTH be right.

Now take your game boys and play nice on this freakin humungous 46″ TV that no one in his right mind could really need…

SFHawkGuy –

You’re nuts. Please don’t assign all of your weirdness to me. I don’t claim superior wealth or judgment.

On second thought, I can claim superior reading comprehension skills, but only in comparison to yours.

I saw that 60 minutes report and for me, there’s the rub – huge inventory numbers. Maybe I’m crazy, but I just don’t see a massive collapse in value (the 50% declines that some of y’all are talking about) with a whopping 1,000 units on the MLS for SF proper (to 3.3 month supply even with the volume decline). But perhaps my sense is skewed – I know that on my lovely block o’ Glen Park, most of the people have lived here for a really long time and have no intention of moving. I know that I have no intention of moving to rent someplace permanently – especially given prior experience. Sure there are some oddly lucky people like Satchel and Spencer who seem to find bargains (and yeah – since we’re scheduled to a major remodel in a few months, I’d love your advice for finding something that will fit 3 kids with those crazy things like parking, a dishwasher, lead paint free, and laundry amenities for cheap!), but I’ve only had craptacular apartments with landlords who have no trouble raising the rent on a yearly basis on already outrageous rents.

Amused,

Reading comprehension has always been my strength. I’m really good at reading between the lines 🙂

Just didn’t like your mischaracterization of those you disagree with as poor armchair economists. In general, I think this site attracts a lot of intelligent posters and I don’t think many on here are poor. Anyway, as I noted, we are all armchair economists because those of us that rent or own housing are betting money on our economic analysis.

As Satchel says, let’s be friends!

10% from right now is the wager. Toodaloo till then. It’s a little bit fun at times to argue with all the b’errors on here, but I have grown tired of repeating myself.

Spencer, you agree with Satchel that values will roll back to 2002 levels? That parts Bernal Heights will lose 50% of its value? Well guess what? Since 2002 South Beach has emerged from the ether. The Mission south of 21st street has gentrified to a point of no return. The same is true of much of Bernal Heights. That’s why I find these proclamations ludicrous and unworthy of further argument.

See ya’s this summer.

fluj, you never answered my question: how are we going to measure the change? S&P data? CAR data? Local realtors’ clipped threshold medians? We need a benchmark before you run off.

Oh gosh, Fluj – don’t go. We need you as part of the vocal minority.

Fluj

coming back in 6-8 months will be of some help, but not a lot.

Real Estate typically has a very SLOOWWWWWW downturn. so I anticipate that most of the damage will be done by inflation over a time period much longer than 5-6 months (years and years and years)

so 5-6 years from now, homes may cost about the same in nominal terms or maybe just a little less. But the dollar will be worth less, so it won’t “hurt” as much. If we get 6 years of inflation at 3%, that takes care of 18% of the real drop…

I suspect a lot of the drop will be that way… inflationary.

when people look back, they’ll only see an “x”% reduction in home prices. they’ll say: that’s not much at all! but the true loss will be X% plus inflation losses.

it will still suck for owners IF this happens… imagine paying 2-3x comparable rent for a place that’s worth the same amount 6 years from now. that ends up being hundreds of thousands of dollars given the high cost of owning versus renting.

I have friends as example who are going from a $2100/month 1BR apartment to a condo with PITI payments nearing $6,000/month.

even after tax breaks that comes out to more than $30,000/year extra on housing. If they don’t get appreciation for 6 years, the will have spent $180,000+ more just to “own”.

that’s where the damage will be I’m guessing.

(yes, the condo they’re buying is much nicer than the apartment, but also the same size. and it’s $30k a year more!!!! yikes!)

just to be clear, i did not say that would all happen by this summer. I think it will take 2-3 to unwind.

but yes, i do think we will be back to 2002-2003 levels in many parts of the city. I would certainly include bernal and the mission in that projection. south beach is hard as it is a new neighborhood, but it will be coming down to some degree.

i think prices in the city are already down between 5-10% from peak and there is a lot more inventory than you can find on MLS (willing to bet 5x the inventory is out there)

FWIW:

my numbers above are not my prognosis, just a hypothetical example.

we may instead see somthing like:

inflation running at 4% per year

SF RE going UP at 1 % per year.

the nominal price is going up, but the owner is still losing a lot to inflation…

it’s a hidden price drop.

anyway…

Someone wrote:

> buy/rent will always be out of whack here.

Then Satchel wrote:

> Not a chance. Something, though, that is never brought

> up is that buy/rent ratios IMO are analogous to stock p/e

> ratios – the same ratio does not apply to all stocks in all

> sectors.

In real estate we call the ratio the GRM or Gross Rent Multiple. Homes in better areas (that rent to better tenants) have always had higher GRMs

> In housing, it would seem to me that the entry level places

> (1/1s, smaller SFHs in sketchy neighborhoods, etc.) should

> cost LESS to buy than rent.

My family has been buying and renting homes on the SF Peninsula for 50 years and every home (even the ones in nice parts of San Mateo and Burlingame west of El Camino) cost less to buy than to rent (that is how we make money). The homes in sketchy (if you want to call Shoreview in San Mateo or the Saramonte area of Daly City sketchy) had huge cash flow from day one in the 50’s, 60’s, 70’s, 80’s and 90’s. It has only been in the last few years why you could lie about what you make and get a $500K loan while working at McDonalds that prices have gone out of whack.

> About the bubble deflating, 20% – or any figure – is sort of

> misleading IMO. Although there will of course be exceptions

> for individual properties and neighborhoods/situations, I think

> we are likely to see prices rolled back “by years”.

Remember the crappy Richmond District homes that went up 300% (from $300K to $900K) only need to drop 66% to get back to where they were in the 90’s…

As banks keep losing money and homes keep dropping in value they will keep making it harder and harder to get a loan and prices will keep going lower…

The table below compares MLS sales for the Jan 1 – Jan 28 period for 2007 and 2008 by MLS district for Single Family Homes. The rows contain the following fields: MLS District, 2007 sales, 2008 sales, median selling price 07 (in 000s), median selling price 08, price per sq ft 07, price per sq ft 08. (Price per square foot is the median of the applicable range where square footage was available.)

1 7 5 $1,000 $2,275 $600.0 N/A

2 18 17 $794 $809 $490.0 $515.0

3 3 7 $750 $1,000 $480.0 $505.0

4 24 7 $868 $1,240 $563.0 $557.0

5 12 14 $1,165 $1,477 $775.0 $805.0

6 2 3 $1,250 $2,050 N/A $721.0

7 6 5 $2,471 $3,500 $790.0 $879.0

8 1 0 $1,275 – $582.0 –

9 11 9 $1,025 $795 $560.0 $681.0

10 42 12 $690 $615 $516.0 $582.0

Tot 126 79 $817 $900 $530.0 $592.0

Note the overall volume decline for SFH – 126 sales for the 07 period v 79 for the 08 period. Also note that the median price increased in the 08 period for every district except 9 & 10. However (and surprising to me), the median price per square foot increased in every district except for the slight decline in District 4.

As many have pointed out, even dissecting at the district and per sq ft level doesn’t really fully account for mix – but these apparent price increases for SFH’s were surprising.

I’ll look at condos by district later. Overall price declines seem more evident in condos: The Jan 07 period had 137 total sales at a $735K median price while Jan 08 shows 86 sales at $710K. Price per sf declined from $573 in 07 to $555 in 08.

FSBO,

Interesting data. Just about the $/sq. ft rising, though – I wouldn’t place any faith in that. None of it – or almost none of it – is adjusted for additions/renovations. The bubble has resulted in an ENORMOUS amount of renovation. Some of this has always been present in SF no doubt, but my belief is that over the past few years the trend has accelerated. Additionally, one can assume that seller/flippers are motivated to sell, and thus a higher percentage of their homes listed actually get sold and thus feed through to the data, as compared with presumably less motivated long-term owners (who will often wait to get “their” price). At least that is what I am seeing in my part of District 4.

The distortions are large – and of course well known to the realtors. Here is just one example (of literally a dozen or so within 5 or 6 blocks of where I live): 195 St. Elmo.

Here is the Zillow listing, which shows the square footage as 2,116:

http://www.zillow.com/HomeDetails.htm?zprop=15137515

Now, here is the advertsising copy:

http://www.ubayp.com/buy/PropertyDetail.aspx?ID=336124&ViewPanel=true

Note the “magic” addition of about 1700 square feet!! The house also “grew” 2 extra bedrooms and 2 bathrooms! Wow!

Now, when it sells (at less than #2.1MM – my guess is it will go for $1.6-1.8MM – let’s assume $1.7MM), the data will go into the stats at $803 sq/ft (keying off the phony 2,116 tax record figure), rather than the “true” $445 sq/ft figure (keying off the renovated 3,816 figure).

As I said above, this goes on all the time. You can guess that it doesn’t take too many of these flips/renovations to distort the data sets, especially when you are dealing with the low numbers of SF inventory and sales. Even easier to get the distortions when numbers of sales are down, as many of the ones that do sell are the “winners” of the beauty pageant.

The CAR and NAR understand all this, even if the average realtor is not bright enough to grasp these simple statistical problems. Once again, at the risk of sounding really pompous, when you are dealing with a very heterogeneous population (het. with respect to value) as in SF, medians are almost useless. In more homogeneous environments (think of the tract homes in Vacaville, for example), trends in the median come closer to representing what is actually going on. If the CAR and NAR were honest (which they are not), they would at least utilize “clipped medians” – an elementary way of filtering some of the “noise” out of the median by cutting off values that fall, say, 1 or 2 standard deviations above or below the mean (many ways to clip medians – that is just one).

Additionally, because of the overinvestment in housing because of the bubble – with the attendant renovations/remodelling, especially in glamour locations – the dispersion of values in a heterogeneous value environment like SF is actually growing over time, leading to heterskedascticity in the data, again calling into question the usefullness of unadjusted median/mean data.

Bottom line, take all median data with a LARGE grain of salt. And, please, don’t encourage the $/sq. ft fraud!

FSBO,

Further to my rant about the unreliability of $/sq ft. statistics, here is another District 4 “gem” that has polluted the stats:

155 Upland. Sold 10/07. $895 per square foot for this lovely 1 bathroom house:

http://www.trulia.com/homes/California/San_Francisco/sold/108593-155-Upland-Dr-San-Francisco-CA-94127

Or was it really a 4,000 square foot house (!) with 5-1/2 bathrooms (!) that sold for $412 per square foot:

http://www.obeo.com/Public/Search/AgentSearchResults.aspx?Agent=63229

(Look at the fourth listing down, and click on the picture for the full tour.)

Now, WHICH IS IT? Do nice SFHs in District 4 go for $900 per square foot or $400?? And which do you think CAR want you to believe!

Anyone looking at $/square foot measures in a bubble and thinking they are accurate is foolish.

I’m looking forward to your data on condos. There, it is much more difficult (obviously) to distort the $/sq. ft measures, although there are still issues relating to general renovations as well as the “beauty pageant” effect (in a declining sales volume market, the prettiest condos sell, and it looks like prices are skewing upwards).

If one of the many realtors on this site wants to dispute my logic here, I would of course welcome it. Any seller of securities (regulated since the 1934 Act) to the general public engaging in the sort of nonsense that is regularly peddled by the used house salesmen would be in jail. I am not a huge fan of regulation, but given the central importance of decisions to purchase homes in average peoples’ lives, it would seem that some disclosure laws are going to have to be passed, and control of the MLS system (at the very least) is going to have to be taken away from the salespeople.

Re: recorded and actual square footage:

Lots of houses are bigger than their recorded square footage. So price per square foot is inaccurate for many homes. But that inaccuracy is built in to both 2007 and 2008 price per square foot figures, so it is not likely the explanation for year over year changes in prices, especially if the number of sold homes being compared is large enough that an inaccuracy in any one home doesn’t substantially affect the numbers.

Dan,

I posted a more elaborate discussion about medians and $/sq. ft but that hasn’t shown on the site yet (probably delayed because of some www links that need to get cleared by the editor).

What you say about inaccurate data being consistent from year to year basically is plausible in normal environments, but not at the tail end of bubble environments, for two basic reasons. First, the bubble encourages rampant flipping and speculation/overinvestment, on a trend basis. Thus, all else being held equal, over time during the bubble, the data become more distorted, as increasing amounts of renovated product washes through the data. Now that the bubble is bursting, these distortions should lessen, but it will take time.

Second, and more importantly, volumes begin to trail off at the end of bubbles, usually before we see any big price drops. That has been the pattern in markets where everyone agrees there has already been a crash (e.g., Stockton, or Naples, FL), and we are almost certainly seeing the inklings of that falloff now in SF proper, with volume of sales off 20-40% depending upon area and exact temporal point of reference. As sales volume decreases, the “beauty pageant” effect begins to weigh more heavily. The gussied up – read, “renovated down to the studs” – sells in this lower volume environment, both because it is prettier as well as because the owner/flipper is a more determined seller. Thus, again holding all else equal, we would expect to see $/sq. ft rising as the proportion of renovated/flipped houses increases. In a small market like SF (relatively low numbers of sales), the impact of these renovated houses is likely to be relatively large.

And that’s what is going on IMO. In my original post (which I am guessing will show up soon), I noted another District 4 house that will soon be used to distort the data some more. I have a large list of them. My interest in all of this stems from my desire to make money off the credit implosion that will follow from the massive and stupid misallocation of resources that the US has diverted into silly things like home renovation; so far, my thesis is proving correct, and for those who were able to foresee this, the equity and credit markets over the last few months have been a wonderful gift!

And last, about inaccurate data, if the realtors know the data is inaccurate, why do they advertise it?? (See the Trulia listing for 155 Upland above.) On Wall Street, there is a simple name for this: material misrepresentation, or, fraud.

I mostly agree with Satchel here – the $/SF numbers have taken on the aura of gospel in the last couple of years in the local real estate world yet a key part of this equation, the house size, is a pretty unreliable number in many cases. Case in point, all those Sunset and Area 10 row house homes generally do not include the square footage of legal or illegal improvements in the lower level of the house. Furthermore, a lot of sales do not have a listed area figure at all, so what do you do – not include those sales? Or if you include them at zero square feet you are basically making your price per square foot measure meaningless. It’s a measure of the general market’s value, but it’s accuracy leaves a lot to be desired. I wouldn’t go so far as to say it’s widespread systemic fraud – it’s just more that this number is not required to be published or reported accurately by any public agency and realtors get sued for misrepresenting size all the time, so they go with the public record figure instead of going out on a limb. The number to watch more carefully though is the sales volume/number of sales and this has been telling a significantly different story than the rising median price and price per square foot for some time now.

Here is the table of condo sales for the period Jan 1 – Jan 28 for 2007 & 2008. As with the table above, the rows contain: District #, 07 sales, 08 sales, 07 median price (in $000s), 08 median price, 07 median price per sf, 08 median price per sf:

1: 8 6 $740 $872 $540.0 N/A

2: 0 2 $0 $703 $0.0 $503.0

3: 4 0 $518 $0 $553.0 $0.0

4: 3 0 $725 $0 $520.0 $0.0

5: 23 11 $780 $875 $581.0 $586.0

6: 15 12 $725 $659 $540.0 $550.0

7: 13 10 $785 $801 $663.0 $870.0

8: 23 13 $790 $610 $680.0 $743.0

9: 42 32 $723 $653 $673.0 $680.0

10: 6 1 $501 $455 $524.0 $375.0

Tot: 137 87 $735 $710 $585.0 $682.0

Here are the district descriptions:

1 Northwest

2 Central West

3 Southwest

4 Twin Peaks West

5 Central

6 Central North

7 North

8 Northeast

9 Central East

10 Southeast

As with the SFH table, I obtained the median price per square foot where there was sufficient data. Nearly 30% of the condo records lack square footage data (as did nearly 20% of the SFH’s) – so there is a real gap here. The median sale price declined in Jan 08 v Jan 07 in four districts (including the higher volume districts 8 & 9) and in total. Three other districts showed an increase in median price and three had no sales in one of the January periods. The median price per sf seemed to increase somewhat in all measurable districts (except for the one sale in District 10); however, if I would have used median price / mean square footage the results would be different.

Satchel – I agree with your points. It is tough to make comparisons with these relatively small sample sizes and given that these are not identical assets being priced at different points in time. (It would also be nice if 30% of the data was not missing the square footage figures.) Regarding 155 Upland, the recent post-renovation sale for $1.6M lacks square footage, but the 2006 sale for $985K shows 1,844 sf. It looks like a pretty extensive remodel (with lots of permits pulled). How hard is it to measure the area of rectangles?

So volume is clearly down but the pricing data remains somewhat equivocal. You can look at other areas (eg Sacramento) and the data is down every which way from Sunday. It’s still just not that clear here (but I would not bet against your forecasts).

FSBO, I truly appreciate your posting up-to-date MLS numbers and a good, honest assessment of things. I assume you are a realtor? Can you provide contact info? (We have a steady flow of new associates in my office looking for realtors, and who knows . . . maybe I’ll be interested in buying or selling someday).

Trip – thanks, one of these days I’ll figure out how to do Excel tables in HTML because I would like to post more data. I’m not directly in the retail side – but I think there’re some very analytical realtors at the site (including fluj who I hope doesn’t make good on his threat to leave).

Satchel,

You discount YoY SFR stats due to renovations in the same breath as you admit renovations are an ongoing San Francisco trend. That is ridiculous. Just as many people were renovating properties in 2006 as 2007. Probably even more in 2006!

Also, without renovation, RE depreciates. Let’s assume a property lasts 40 years in average, so after 40 years, the property is worth the lot price.

In normal market, the depreciation and renovation cancel each other out. The condition of properties as a whole does not change much.

[fluj],

Read my argument carefully, and note what I postulated about increasing renovation/remodel activity in the context of declining sales volumes and the “beauty pageant” effect. It’s just a theory I have – time will tell!

However, I would caution that I have never predicted a spectacular crash. That’s not the way these sorts of bubbles deflate. Houses are long-term – and illiquid – “investments” (they’re not really investments at all). By the time the data unequivocally demonstrate a serious problem, it will be too late for most who bought in the bubble frenzy. They will be relegated to hoping that inflation “bails them out” while simultaneously hoping that equilibrium interest rates don’t go up (because that will collapse a leveraged asset class). So, we need to come up with theories and test them against what we are seeing. If I had unrestricted access to the MLS – or first hand knowledge of evry transaction that is going on – then I could post much more cogent analysis.

“Just as many people were renovating properties in 2006 as 2007.”

If you’ve got hard data on that, I’d love to see it. That does not accord with what I have witnessed over the last 6 years in my small part of District 4. Also, keep in mind that the nature of renovations means that there are usually 1-2 YEARS between the initial purchase and the sale of the flipped property, so the distortions take some time to wash through. FYI, residential investment as a share of GDP has collapsed in 2007 to below its trend level (from an extraordinarily high share – Calculated Risk has an interesting piece on this today). Also, CME lumber futures have collapsed (down to $220 last I looked – I think that’s an ALL TIME low for the continuous contract), indicating severe contraction of building activity (among other things). It also seems plausible to assume that the flipper/renovation frenzy peaked sometime after 2003/2004 (historic low interst rates, coupled with the inklings of the frenzy starting to be reflected in the mass media and tv shows like “Flip This House”, etc.), and so the distortions would have been increasing on a trend basis through the 2005-2007 sales years. Now my guess is that this process is going into reverse in SF. There is nothing surprising about the fact that SF – being very wealthy and having numerous positives – would be one of the last holdouts as the bubble deflates (along with Manhattan, and a few West LA spots, primarily).

We’ll see how this all spins out!

Satchel – your hypothesis regarding square footage and realtor hyperbole is unfounded. The first example you gave, 195, St Elmo claims 3812 square feet in the listing. This works out at around $570 p/sf – more or less what one might expect for a remodel in district 4. The other example at Upland does not list the square footage at all and likely would be excluded from any p/sf calculation. My point is that in these examples one is likely to get a better idea of p/sf from a knowledgeable realtor (not necessarily an oxymoron) than a public real estate entertainment site like Zillow. In addition, with such a limited data set the figures lack meaning. Using square footage to determine the value of San Francisco single family homes is an extremely crude tool – not all square footage is created equal. IMO the reason the market seems to be defying logic and we are not seeing any meaningful price declines is simply a paucity of decent single family homes in good neighborhoods.It really is that simple.Given this tiny number there are of course going to be buyers who, for any number of personal reasons, will snap them up and not pay too much attention to the metrics. They just want the house. There is very little inventory and they don’t want to, or can’t, wait. Even if the market does tank in San Francisco proper it is unlikely we will see a deluge of quality single family homes swamp the market at pre bubble prices. More likely several years of sclerotic activity with little change in nominal prices whilst inflation slowly eats away at real value.

Screw it. All of you are seemingly backing off of your Ragnarok predictions after I challenged you yesterday. I’ve seen a steady stream of, “How can we quantify it,” “Inflation will actually account for it, rendering true percentage drops immeasurable” “Cycles actually take two to three years” and “insert hedging equivocation here.” So I guess there’s no point in leaving. This has absolutely nothing to do with being addicted to real estate blogs. I promise.

So Satchel, yEah, exactly. It is one or two years behind. You were questioning ’07 versus ’08. I suggested just as many renovations were in ’06 as ’07. So you are wrong. Ask any tradesmen. SF is Carpenter’s Paradise and it always has been. The popularity of TV shows such as “Flip This House” was at its zenith in like 2005 and 2006.

Clearly all of you are backing away from your doomsday predictions now. I love it.

Yeah! Fluj is back to challenge the masses! I for one am very happy.

@Expat – I could not agree with you more. Excellent post. We need more like you on here.

Then be of good cheer .not. fluj. You can depend on me.

50% off everything in the city by 2011. Case-Schiller at 110. Just like I’ve always said.

Fluj,

That’s GREAT that it’s you! Please stick around.

I haven’t predicted the apocalypse – I haven’t predicted a replay of the Great Depression. But it will be bad – VERY bad for people who are highly leveraged and thought that credit inflation and lower interest rates were one way streets.

About SF proper – my prediction is down 30% on average, within 3 years. Nominal, not inflation adjusted. As for methodology, this 30% is a hypothetical number, which would basically be “discoverable” if you do this basic experiment: throw a bunch of darts at a SF map at the peak of the bubble frenzy (I’m going with late 2006, on average). Use a large number of darts. Divide by the number of darts, and note the dollar figure. Revisit the properties identified by these dart tosses 3 years from now. Most will be down. Some will be wipeouts. A few will be up. Subtract out fair value of all renovations done (not necessarily what was actually paid), in the aggregate. Divide the resulting sum by the number of darts and compare with the earlier figure. My guess is that the number will be 30% lower (more or less).

As for specific neighborhoods/types of houses. I expect that the best neighborhoods will show the least declines and there will be further segmentation of the SF marketplace. Maybe 5-20% declines. Many neighborhoods will be in the middle. Maybe 15-35% declines? Some neighborhoods will be annihilated, like down greater than 60-70%. We’re already seeing foreclosures in the Bayview at almost 50% last sales price, so no bold prediction here.

As for types of residence. Smaller, more undesirable properties (1/1 condos in SOMA, smaller starter homes in Sunset, e.g.) will do WORSE on a relative basis than their neighborhood. The better, more desirable, and larger properties will do better on a relative basis, and will not go down as far as their neighborhood “average” decline.

Those are my predictions, and I’ll let you know if I change them!

As for what this would do to SF, in response to John above equating a 20% decline with a Depression, I don’t think a 30% decline would be a big deal. More than 60% of the city are renters, and they won’t care. Many long-term owners will be a little upset, and they might save a bit more to compensate for the loss of perceived housing wealth, but again, no big deal. Some recent buyers will be wealthy enough that – again – no big deal. But for the smaller percentage who stretched to afford during the bubble, well, for them my prediction is that it will certainly feel like a depression. Maybe 5% of the population will have their financial security “wash out”. Probably less.

20%, or even 30% – or even 40-50% is NO BIG DEAL to a great city. NYC did it in the early 90s (probably around 20-25% decline). Fort Lauderdale and Miami (questionable whether these are “great” cities but what the hell) are experiencing greater than 20% losses to bubble wealth RIGHT NOW, and my wife just got back from visiting with family there and reports that everything seems fine.

“Clearly all of you are backing away from your doomsday predictions now. I love it.”

Fluj – As far as I can tell you’re the only one on this thread that keeps talking about a 10% decline over the next six months. I don’t see anyone backing away from a 10-20% decline over the next two years. It makes me wonder if you understand how real estate markets work other than when they’re going up.

As many have noted, the problem with predictions is it is extremely difficult to quantify whether they have come true or not! CSI, whatever its perceived flaws and irrelevancies, is at least a firm number, and the fact that the Chicago Merc sees fit to trade on it at least indicates that those willing to put real money on the line consider it valid.

What we see in the graph above is a deeper, steeper drop in SF (yes, the MSA not just SF) than at any time in the last 20 years. And this is through November — we know that December was awful and January is looking the same. CSI for the SF MSA is now 10.5% off the highs in early 2006. My 2 cents is that we’ll see another 15% drop by the end of 2008 — to 166. (Heck, if the current trend prevails, we’ll see that by April). That’s not doomsday, and it will only really hurt those who bought the last few years, or have already refied out all their equity, and now must sell for whatever reason.

The problem is that everybody I’m referring to has been reserving the right to begin at a future point in time. Meanwhile, they have been talking about collapse or sea change for many months if not over a year. When, then? Can we at least go back to mid-August of 2007 when the credit market changed? Even that is a generous start point for the prognasticating set. They had been talking sea change for quite some time before that!

I think most of us talking sea change realize that it takes years to develop. It certainly has started. no one know when it will finish. Personally I have always expected it to take 2-3 years, but it could take longer.

The start of the time horizon was summer 07, but it has been predictable for some time. if you didn’t know we were ina buble , then your eyes were closed.

A valid complaint fluj. But at least in my case I’ve been saying that you would see the first signs of distress in 08 and the beginning of serious declines when the Alt-A / Option Arm reset wave begins hitting in earnest in 09. That’s why my prediction is for 11. When, exactly, sentiment is going to turn in the near term is not something that I would predict. Like the saying goes, “Markets can stay irrational longer than you can stay solvent.” I’ll admit to being amazed that the market has held up as well as it has for as long as it has, which is why I never contradict you about the current state of the market. But the process is proceeding through the expected stages and I see no reason to change my outlook.