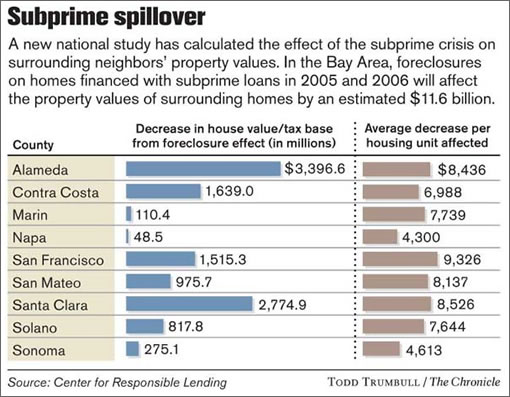

“The losses (from foreclosures) are extending to neighbors and to entire communities,” said Martin Eakes, chief executive of the Durham, N.C., Center for Responsible Lending, which released the survey on Tuesday. “The spillover effect is disturbing because we’ve only just begun to see the foreclosures.”

“Foreclosures aren’t causing prices to fall – it’s a symptom of the whole thing unraveling,” [Christopher ] Thornberg said. “If you had no foreclosures at all, prices were still going to fall. (Foreclosures) may accelerate the process, but it’s a process that has to happen one way or another because when you look at (home) prices relative to income, it’s completely insane.”

∙ Ripple effect of foreclosures touch entire communities [SFGate]

ouch…I’m considering selling soon. Should I wait till late spring or will I have a harder time of it then?

sell ASAP, its going to get a lot worse before it gets better

hold on to it forever and enjoy 20% year over year appreciation. this study is wrong – SF is immune. in fact, you should buy a 2nd home asap before you get priced out forever!

Clearly Chris Thornberg, The Center for Responsible Lending, and The Chronicle staff are nothing but a bunch of bitter renters and are not to be listened to.

A $9,326 loss…wew! Big loss! Gosh, I better sell my house. That’s one or two paychecks for most people who can afford to buy houses here.

Tough decision, jj. I’m with sw in reading the mountain of tea leaves that indicate prices can’t go anywhere but down — so selling now rather than after further declines makes sense. But we’re now approaching the slow real estate season where demand is usually a little more slack.

Those who made the then-tough decision to sell Cisco at 60 in fall ’00 — at 1/2 the price it was trading at 8 months earlier — came out far better than those who waited for the 2001 “spring bounce” when the price fell to 15 where it then basically sat for the next 5 years. (I know, I know, housing is not like the stock market and nobody is predicting SF real estate to decline by 80%).

Wow, I have to reduce my $200k capital gain by $9,326? How devastating. The market is clearly imploding.

You have no capital gains until you sell. If you wanted to mark-to-market, you would have to reduce it by the decline in property values, $9,326 of which is due solely to the effect of foreclosures of homes financed with subprime loans (according to this analysis).

jj – I think if you base your decision to sell now or wait on what people on this blog will tell you, you will be making a very bad decision.

While the market may not be imploding, I believe it is slowly unraveling. There are 5 two unit flats for sale in my neighborhood all on one city block. One was a complete remodel down to the studs. One building was completely torn down and rebuilt. One was a partial remodel. None have sold. Three of the five buildings have been on the market for at least 4+ months. I admit that this is not in a prime neighborhood, but it is still in San Francisco. And no, it is not the Outer Sunset or Bayview.

These amounts don’t match previously published statistics in the Chronicle. I think there is more to this than what is being said in this article.

The data given in this article does not seem to match the foreclosure rates given in another Chronicle article a while back. San Francisco calculates to 162 homes. Alameda – 403 homes. Contra Costa – 235 homes. Contra Costa had a foreclosure rate many times that of San Francisco. Something is not right about this data – or something about it has not been made explicitly clear. Refer to the article from Oct. 14.

http://www.sfgate.com/cgi-bin/article.cgi?f=/c/a/2007/10/14/MNVPSEMVQ.DTL

Andy, the article is using forward looking projected losses by the Center for Responsible Lending.

The stats you are referring to are backward actual foreclosures.

They cannot be accurately compared without gather much more information on CRL’s methodology.

“Forward looking” i.e. assumption riddled.

Craig –

yeah projections like these are tough and sure to be off. However the latest DQ Number for So Cal show medians falling back to 2005 levels.

The Nor Cal numbers tend follow the So Cal trend but with a couple of months delay (basically, So Cal is in the front car of the coaster and Nor Cal is in the rear). The Nor Cal numbers should be out tomorrow.

The big question for both regions is how strongly will the Jumbo mortgage market return. The market needs big loans obtained easily to sustain prices and since that spigot was cut off in Aug we have seen a dramatic impact in CA.

As credit markets stabilize Jumbo’s should come back but will they come back enough?

If I had to live in So Cal I would put an end to it all, not due to those numbers, but due to the people. One does lead the other, but it seems that So Cal prices have risen more (% wise) over the last few years compared to SF, so perhaps they may have further to correct as well? Just guessing here.

I will be interested to see what happens with the Jumbo market by next spring. Things seem to be doing their normal slowdown right now, which is likely to stem any real short-term impact of unattainable jumbo loans.

Craig –

Case Shiller would totally agree …

http://www.papereconomy.com/CSI.aspx?id=LXXR|SFXR&yoy=all

Badlydrawnbear. Thanks for the heads up on the forecast but the article I listed shows both past foreclosures and notices of foreclosure which would point to future actual foreclosures (look at the detail by county by zip). Somebody is way off, and since this is a forecast with no real explanation, I wouldn’t put to much into this and would put more into the other article which uses actual data. That said, I agree with the comments that the small drop they are indicating in values on a per home basis (which is in itself not so helpful cause real estate is local) does not indicate the sky is falling and shouldn’t cause people to sell unless they have to….or perhaps unless they are speculators.

Please refer to a certain other blog out there. Prices will soon touch $2000 psf in SF.

Buy now or be priced out forever !

On a serious note, the economic fundamentals will catch up sooner or later. A RE bubble is not like a stock bubble, it will take a while to slowly deflate.

jj- you probably should speak with someone knowledgeable about the market in the neighborhood where you own.

As the data released today on this site shows, prices for SFH’s are rising in some SF neighborhoods, year-over-year, and falling in others.

^ that data shows that what people are paying for homes in some neighborhoods are rising/falling, which isn’t the same thing as home values.

district 8 has gone from three sales and a median sales price of $1.546M to one sale and a median sales price of $5.939M. think that’s indicative of skyrocketing property values or a change in the mix?

Hey, another great thread about rising/falling prices in SF!

Owners: “Prices are holding going up! Break out the champagne, its gonna be another great year for SF real estate!”

Renters: “Prices are on the cusp — they’ll drop soon, I just know it — look at what’s happening in (insert neighborhood/town here): Bayview / South SF / Outer Sunset / Oakland / Stockton / etc…)”

Repeat ad nauseum.

Clearly, prices DON’T have to be inline with economic fundamentals because if they DID, then how would you get a “bubble” in the first place?!

The whole discussion is nonsense.

As someone who just bought in San Mateo county and has been watching comps like a hawk ever since, this study is extremely dubious. It’s interesting, you can’t even tell that these are PROJECTIONS unless you read it closely. It’s amazing how people are accepting projections as fact. If they are so good at predicting the future, they wouldn’t be working at non-profits.

Literally.

I agree with Thomas that these projections by the Center for Responsible Lending need to be viewed with a grain of salt – check out the CRL’s activist pedigree. But I also disagree with Jimmy (Bitter Renter) – economic fundamentals determine prices over the long term. Bubbles can’t last forever – although there can be paradigm shifts. Thornberg is a pretty credible guy and he still thinks prices are “completely insane”.

jj,

I came across this nifty Home Value Calculator earlier today:

http://www.papereconomy.com/Calculator.aspx

It uses the Case/Schiller Index and provides some projections on the future prices. The results for my house in San Jose (I used San Francisco index; it doesn’t appear that there is a San Jose index) that I bought in 1996 are somewhat off but I would be interested to know how it works for San Francisco.

Here’s a link that explains a little how the calculator works:

http://paper-money.blogspot.com/2007/11/calculate-your-paper-housing-wealth.html