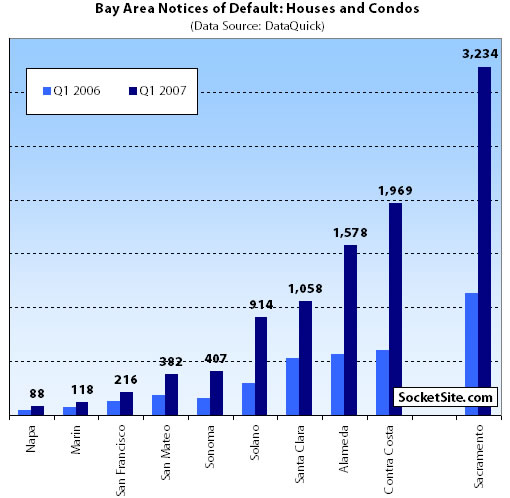

While a 67.4% year-over-year increase in San Francisco Q1 “Notice of Default” activity sounds dramatic, in absolute terms it still represents relatively few properties (216). Within the greater Bay Area, however, Contra Costa hit a record level of Q1 default activity (1,969 notices, up 225.5% year-over-year) as did Sacramento (3,234 notices, up 184.7% year-over-year). And Alameda isn’t too far behind (1,578 notices, up 179.8%).

According to DataQuick, “[t]he number of default notices sent to California homeowners last quarter increased to its highest level in almost ten years, the result of flat appreciation, slow sales, and post teaser-rate mortgage resets,” and “[m]ost of the loans that went into default last quarter were originated between April 2005 and May 2006.”

And while most homeowners “emerge from the foreclosure process by bringing their payments current, refinancing, or selling the home and paying off what they owe…about 40 percent of homeowners who found themselves in default last year actually lost their homes to foreclosure in the first quarter.” That’s up from nine percent at the same time last year.

Keep in mind that long-term interest rates remain near historic lows, and according to most, the Bay Area economy remains strong (and incomes are up).

∙ California Foreclosure Activity Jumps Again [DQNews]

For some, the worst is yet to come. For others, opportunity is going to be knocking … hard … and many times.

Wow…i know that many on this blog have been anticipating this, but I’m floored by the absolute and percentage increases, even if things are not (yet) dire in SF.

The percentage increase is impressive. But do we have any sense of how the absolute numbers compare to the last real estate slump in the early 90’s?

“The default numbers reflect wide regional differences. The first-quarter numbers were a record in San Diego, Sacramento and Contra Costa counties. In Los Angeles County it was almost 60 percent below the first-quarter 1996 peak, reflecting the depth of the recession in the mid-1990s as well as relative strength in today’s market.”

So despite the lack of any local recession, Contra Costa and Sacramento defaults are HIGHER than during the 90’s real estate slump.

When I, amongst others here, made predictions about this stuff like 6-9 months ago, people posted comments like “How can anybody let a property go to foreclosure in such a hot market?”

Now it’s all slowly unwinding like it has in previous cycles, even though “it’s different here” and “it’s different this time.”

I was told by my broker that in Antioch 60% of current listings are short sales. I’d be surprised if there’s even 5% short sales in SF.

I calculated 2007 Q1 NOD as a % of total sales (new and existing). I used 2005 Dataquick sales figures as I didn’t have the year-end #’s for 2006. The three “worst” counties are Sacramento (9.0%), Solano (8.1%), and Contra Costa (7.8%). The three “best” counties are Marin (2.5%), San Francisco (2.9%), and Santa Clara (3.4%)…that was surprising about Santa Clara.

Less surprisingly, there seems to be some correlation with “affordability”. According to DataQuick, Sacramento, Solano, and Contra Costa Counties are among the lowest in average sale price for existing homes. Marin, San Francisco, and Santa Clara Counties are among the highest.

It will be interesting to see if these higher-priced markets continue to hold up.

I doubt they will. Sure, SF is more desirable than Fremont or Antioch. But at some price point they can become near-substitutues. If I can buy a ranch in Concord or Pleasanton for the price of a studio in the city, guess where I’m going? 2 hours on BART every day is worth something….$250K differential? $400K? The market will tell us.

The city will hold up better than other parts of the bay, but will not be immune.

I feel like a vulture sitting by the side of the road, waiting for a victim, but I can only hope that I can be in the right place at the right time by the end of the year. Yes, I hope to capitalize on someone else’s misery. Forgive me.

SF homeowners; even the stretched ones are not your typical owners. They generally have the means to last out a prolonged market decline IMO. I really don’t think this market will wholesale take a plunge. Outer area will get killed over time but SF will most likely hold steady, maybe show the odd % drop; but the years of 4-6% appreciation are gone. And certain markets are in danger of getting killed here if prices and oversupply (e.g., somoa condos) continue to build out at this pace.

Frederick (from the Detroit Street posting):

You questioned where I was getting my comment “a huge number of SF homes are in foreclosure or close to it”??? Guess that your 35+ years as a realtor didn’t help you see this one?

My only comment is the one I always have – only 12% of SFers make a salary to afford the median home price in SF. That percentage is MUCH higher everywhere else (the national average is in the 80s). If we’re seeing people in outer counties default at this rate, the city is going to be much worse.

Lol, Lori. Call me a buzzard, a vulture, whatever, it’s all the same. I’ll take it all with a smile as I ready to pounce. 🙂

One man’s loss is another man’s gain. It’s a cruel world.

I’ve been concerned about oversupply in the condo market, but so far it seems the growth has been controlled in a way that has prevented that from happening. We benefit from having such a wide variety of buyers in the condo market, with BMR folks, first-time homebuyers, rich city people, second and third home-owners, empty nesters and investors all in one building.

Our market, unlike the condo markets of Vegas and Miami, are not dependant on one kind of buyer. We’re much more similar to New York — which in 2007 has exceeded expectations of price and absorption.

This is following a classic bust cycle, newer outlying areas decline first as the bubble collapse toward the employment centers.

I agree San Francisco will hold up better then the outlying areas, but to think that SF is not going to be negatively has alread been disprovin.

The 10 city Case-Shiller index for January showed San Francisco prices were negative already.

The median might be holding up but the median seems to be mostly a feel good number for alot of people because it hides alot of negatives in the market.

With the loss of entry level buyers in LA, according to Data Quick, how long will their numbers hold up as the ‘move up’ market collapses. Does anyone honestly see SF being immune to the same effect?

We have had a 10 year run up in prices. Is that market going to really correct in 6 months to a year?

The 89/90 bubble took 5 years to bottom out and this bubble is signifcantly larger than the last.

Agree with rg and badlydrawnbear – this will take months if not years to play out, and we’re just getting started. Still several acts left in this melodrama, including the classic attempted government bailout, failed “investors” bawling & looking for sympathy, media hyping up every dead cat bounce that may occur as a reversal of the cycle, etc. etc.

Those of us waiting to pounce should not feel badly for anyone. Greedy flippers didn’t feel any guilt when they were making $100K/property in a year at somebody’s expense. Most acquaintances who bought real estate (whether they could really afford it or not) were quick to laugh at me for still renting and “missing the boom.”

Why should we feel sorry for them now that the markets are returning to reality?

Dude…my only point in posing that question is my wondering whether FBs would be more prevalent at the lower end of the price spectrum. I agree that some Antioch buyers are frustrated would-be San Francisco buyers although the reverse is less true.

That said, I’m not sure I buy Eddy’s argument that SF buyers are not as stretched or Damion’s argument that the SF market draws from a more diverse economic base (similar to NY). There is no comparing the wealth in cities like NY and London with San Francisco.

Not looking to pick any fights…just wondering.

The data seems to reenforce the idea that Americans, in general, need to learn how to manage their money better. I’m shocked at some of the gambles people took via loan structures or just plain betting the appreciation would make a profit.

I’m getting nervous about bailout discussions in Congress.

Is SF really going to be immune from 1-10 homes going into default?

http://www.bloomberg.com/apps/news?pid=20601103&sid=aonDdgoWQ.pg&refer=patrick.net

“April 12 (Bloomberg) — Kenneth Heebner, manager of the top-performing real-estate fund over the past decade, said U.S. home prices may plunge as much as 20 percent because of rising defaults on riskier mortgages.

Subprime loans, made to borrowers with a history of missed payments or untested credit, and “Alt-A” loans, which require little or no documentation, account for about $2.5 trillion of the $10 trillion in outstanding mortgages, according to Moody’s Economy.com. As much as 40 percent of these loans may default, flooding the real estate market, Heebner said.

“It will be the biggest housing-price decline since the Great Depression,” Heebner, 66, said today in an interview in Boston. Prices may fall by a fifth in some markets, he said.

That would leave home prices at levels last seen in 2003 and 2004, the middle of boom that lifted prices to a record in 2005. The damage from high-risk mortgages will slow the U.S. economy, though not enough to send it into a recession, Heebner said. ”

Quite true — there aren’t as many wealthy people here as in New York or London, but as in New York and London, most of the RE market is priced for the wealthy, and has so far not had difficulty finding buyers.

Even our entry level buyers, struggling to find something nice for $600,000, are wealthy by most people’s standards (outside of northern California.) And yeah, those people are probably “stretching it”… but there’s stretching it and there’s s t r e t c h i n g it, okay?

The guy in SF with a six figure salary making payments on a $600,000 loan is just not in the same position as the family in Sacramento or Antioch struggling to make the same payments. The suburban folks are more economically vulnerable, and have often been blatantly swindled by greedy loan brokers who used every trick in the book to close a deal.

Yes, SF *is* different. (Sarcasm alert –>) The real estate people in the bay area would *never* resort to the same tactics to make money as those in Antioch.

I’m sure lots of mortgage brokers in the bay area told their clients, “I’d rather see you succeed than have me personally make $20K for a days worth of work. Lets pass on this loan for which you would otherwise qualify. I’m sure your agent will understand if I steer you to a cheaper priced home that you can afford.”

You questioned where I was getting my comment “a huge number of SF homes are in foreclosure or close to it”??? Guess that your 35+ years as a realtor didn’t help you see this one? (rg)

“While a 67.4% year-over-year increase in San Francisco Q1 “Notice of Default” activity sounds dramatic, in absolute terms it still represents relatively few properties (216).” (SocketSite)

That’s quite a ways from “huge” and much closer to “normal”.

True, true, tipster — greed doesn’t stop at the city limits. But don’t you find that typical SF buyers are more sophisticated about money than the people who are being foreclosed outside of the city? (I know that sounds mean and snobby… I don’t mean it to!) It’s just that when you read the horror stories of people going into foreclosure, it’s folks who were bamboozled not only into buying something they couldn’t afford — but using the income from every family member and friend in a 500 mile radius to qualify! I mean, they really really really didn’t qualify. If you’re in SF and you really really really don’t qualify, I think you know it, don’t you?

There’s a HUGE difference between being able to qualify for a loan – which many did – and actually being able to afford a property for more than a couple of years – which it appears that many can’t.

Many buyers in San Francisco might have deeper pockets, but that might just mean a longer runway…

But don’t you find that typical SF buyers are more sophisticated about money than the people who are being foreclosed outside of the city?

I think the SF foreclosures knew exactly what they were doing. They were living in a home they couldn’t afford using other people’s money. This was a unique time in which someone, like the buyer of 755 Marina Blvd., could buy a home, and refinance it every year to make the payments, paying practically none of their own money to live in a dream home. They did this for, what, 5-6 years. I’d call that sophisticated indeed. More sophisticated than anything I would have come up with.

So people in Antioch stretched to house their families while people in SF partied and let other people pay their mortgages. Either way, people everywhere took advantage of the free and easy money that was flowing and for whatever reason they did it, they did it.

BTW: 311 Marina Blvd is now also in foreclosure.

I’ve noticed that non-homeowners are doomsayers much more often than homeowners. It would help if posters included the information about whether they own or not. A typical bay area homeowner doesn’t have the available funds to “pounce” if the market has a 10% correction. Remember, a non-homeowner is typicall short the housing market, and a homeowner is typically flat the housing market.

To Chris at 12:07 PM: I AM a homeowner/investor … and NOT a flipper.

I’m a homeowner and I am not happy with the way things have gone up so dramatically in the last few years. I can’t afford to move, even though my propery has gone up in value. For starters, I can’t afford the property taxes. Most of my friends can’t afford to buy anything in SF. I’m not sure what dramatic property values increases have done for me unless I move completely out of the area. Don’t get me wrong, I’m happy that real estate has gone up in value but I think it’s mostly benefitted investors and real estate agents.

“Agree with rg and badlydrawnbear – this will take months if not years to play out, and we’re just getting started”

I predicted two years ago that Bay Area prices would be the same in 2015 as they were in 2005. Real estate downtowns typically take years to play out and, given the loose-credit based price runup we’ve seen over the last few years, I don’t see any reason to believe this one will be different.

I believe this time it is different. The downturn in the market in previous years did not involve all the (creative) financing schemes that have arisen fairly recently in the past few years. Just my speculation, but I think this time, the downturn may happen just a bit sooner than (some) people would like.

I previously owned and sold in 2006. Now, I’m waiting with a lot of cash in my pocket. I think what a lot of people miss in this debate is, why is it happening now? The economy is reported to be strong with 4.4% unemployment and no recession on the horizon. Why in the world would people be starting to default like crazy? Forget the absolute numbers for a second and look at the rate of growth in defaults. If all these people are defaulting but still have great jobs, what’s happening?

To me, it’s obvious that too much creative financing has been employed. Over 70% of buyers here use some non-traditional loan (plus a lot of folks who recently refi or are habitual- or serial-refinancers). This helps drive up values until the music stops. In the last 3 months, we’ve seen over 35 lenders close shop. That destroys lots of new buyers and kills refis. And what’s happened to median prices since all this started? They’ve completely flattened.

It’s worrisome that in a “good economy” we can have so many looming problems on the horizon. How can all these lenders go belly up? I won’t even explore what might happen if we get into a recession but it would undoubtedly be worse.

The days of doing a refi every six months while your equity piles up are done. Nobody can say for sure where prices are headed in SF, but my advice to anybody is to think about buying something you can afford using a traditional loan. Unfortunately for many, that means to buy nothing. But maybe that’s some advice that people should be hearing right now…

Chris @ 12:07 PM: I rent, having sold my home in 2003. A bit early, you might say. OTOH, I pay monthly rent of $3.68/SF for something that would cost >$1,000/SF to buy (plus taxes, insurance, and maintenance).

I might be interested in being an owner again someday, but not unless the value proposition is significantly different.

Tipster brings up some great points – I argued on the Detroit Street blog that realtors and brokers have been greedy and should feel guilt over the people they pulled into bad deals. I got yelled at. There is still no recourse for the realtors who strong-armed appraisors into “matching” the DESIRED value instead of using their appraising education to calculate the real value.

I feel that SF buyers are far LESS sophisticated about money. They have been enticed into buying, even when they can’t afford, by the year over year growth. And they apparently DON’T have the resources to last a prolonged market decline. Again, only 12% of residents can afford to buy in the City. That’s using census data on salaries, federal recommendations of % of income that should go to housing, and SF’s ever increasing median price. While 212 defaults may not be many, the percentage is astounding. And Michael, “normal” articles usually don’t make the top of the Chronicle’s business section.

This “correction” SHOULD take years to play out. What the rapid increase has forgotten about is the need to match rise in incomes! SF simply is going to run out of younger, potential first-time buyers because no one is making the money to afford houses. I’m a renter, desperately wanting to own AND stay in SF. Of course I’m going to be negative on Socketsite. In the last 5 years, my income (which was small to begin with as a typical office worker, but a graduate of UCB) has only raised about 50% (to still WELL below six figures)while real estate has multiplied many times over. Give me time to catch up salary-wise, and meet me halfway with some decreases down to a reasonable median price. That’s all I’m asking.

Btw, NYC’s real estate is NOT priced only for the wealthy. I’ve had multiple friends leave SF for NYC in the past years, and they can all buy a place there. It may not be huge or in Soho, but studio to one-bedroom condos can still be had for under 300K there. Does anyone actually know NY areas median price? I know that a few years ago it was only around 400k, even though SF was in the mid-700k.

I’d add one comment about the absolute numbers in various stage of foreclosure right now. If you go to realtytrac.com and search for SF, you’ll find that about 400 homes have received a notice of default, 140 homes are up for courthouse auction and 300 are now bank-owned. That’s 800 houses and condos in some stage of foreclosure.

These are small numbers to be sure, but there are only 1,000 properties for sale on the market right now. The number of homes in some stage of the foreclosure process is pretty big when you put it in this perspective.

California Dave – Why is this happening now? In a good economy? : The last generation of SFers came of age with high-paying dotcom jobs. This next generation will start off with far less and has been priced out. A “stable” market requires a constant supply of newbies, and we simply don’t have them (or they’re being killed in Iraq, but that’s for another blog)

The key point is not whether 1000s of SF homes actually go into foreclosure. The key is that the rapidly rising numbers of foreclosures and recipients of notices of default are clear indicators that the market has turned south, although the slope of the downward curve is still open to debate. Homes do not go into foreclosure in large numbers in a rising market.

Fueling the price rise and bidding wars of the last few years was a buyer mindset that you cannot wait or you will miss out. It is just the opposite now — the buyer mindset is that you almost certainly won’t pay more if you wait, and you may pay a lot less.

SF sellers have largely held their ground, with prices in 2006-07 slipping a little, by simply refusing to sell. But many, many people here at all income levels have paid more than they can afford, and many of those will have to sell just to avoid a deepening hole. And the usual numbers will still sell for the old reasons (moving for a job, kids approaching school age and want to move to a district with good public schools, etc.). Those sellers cannot just sit on a place forever. They will sell at the highest bid, which will be lower than in the recent past because buyers will be unwilling to buy at inflated prices.

Both the law of supply and demand and the 180-degree turn in buyer psychology will bring prices lower. It is anybody’s guess how low or how long before things bottom out — but the present-day trend is clear as day.

Regarding the comment that only 12% of SF residents can afford a home in SF.

I don’t think those numbers mean what you are touting them to be. It means that only 12% of buyers can buy the median home right now given their salary. It doesn’t take into consideration that a much higher percentage of people can afford the home they already own and that if they sold said home, a large proportion could reinvest that equity and by a home at today’s prices. The 12% figure is concerning because it is indicative of a relatively small pool of NEW buyers.

Also, the 212 foreclosures is an outstanding percentage of what? The increase YOY is a lot, but as a percentage of the total number of outstanding mortgages in SF, it is small.

Finally, I can’t quite figure out how the # of foreclosures is related to current # of listings? Foreclosures as a percentage of total mortgages of a certain age would be informative, but to compare foreclosures to listings doesn’t make sense to me.

To Anonymous 2:18:

Prices are determined at the margin. On the way up, that means that the most desperate/foolish buyers set the benchmark. On the way down, the most motivated sellers set the price level for the rest of the market. To the extent that forced sales become a large component of available inventory, pricing would likely be affected.

I’m not saying that a huge whoosh down is inevitable…as we have all seen, external variables and interventions can have unforeseen effects on markets.

Yeah, I think you CAN get a studio in New York for under $300k. It will be under 300 square feet, similar in size to the studios that were offered here at the Book Concern building last year and took forever to sell, and may in fact be available still (it’s a freaky building!) I don’t think there’s a big price difference for studios here and there — larger studios/junior one-bedrooms in new buildings in New York can go into the 5 and 600’s.

I moved to SF from NYC about 18 months ago. I was a RE attorney there, but do not work in RE here in SF. Comparing NYC prices to SF is deceptive because of the predominance of co-ops in NYC and the inclusion of the outer boroughs in some reports. In NYC most apartments are co-ops, and condos are more desireable and are still a very rare opportunity in Manhattan. Co-ops are priced significantly lower than condos because of the difference in ownership styles. The entry criteria for a co-op purchaser is much more stringent and only truly qualified purchasers will be approved by the co-op board, and creative financing is generally NOT permitted. This eliminates a lot of purchasers who might be tempted to stretch beyond their means and decreases the value of comparing foreclosure rates between NYC and SF. In my opinion, first time ownership in a Manhattan co-op is a realistic goal for the average NYC resident with an average career and salary. Also, NYC has a more robust public transportation system which makes living in an outer borough a much more realistic and appealing option than living in the East Bay, for example, and commuting. Entering the market in SF is a much more daunting task, from my perspective.

There’s a lot of attention being paid now to subprime and Alt-A borrowers who were “taken advantage of” by those “evil” agents and brokers. Not taking either side of that one – probably equal greed on both the part of the buyers and the lenders/agents. Nobody forced these people to buy real estate….but it seems they’re suddenly victims when forced to take some responsibility for their own decisions.

The bigger story is the grade-A credit folks with 700+ FICOs, who got their granite and stainless with an ARM that’s about to adjust. Talking about high wage earners who are smart about money but got greedy and wanted to cash in on the boom. Their only choice will be to sell…lots of those loans converting this year and next.

To anon 2:18:

The 12% affordability figure doesn’t mean much to me on its own; all I know is that it’s waaaay lower than normal, so much lower that someone (I think dataquick? NAR?) changed the way they calculate affordability so that the number wouldn’t look as bad.

Also, I don’t buy that people in SF can ride out a downturn that much longer than others. I have a high income, but if I bought at the high end of what agents and mortgage brokers said was “affordable,” I wouldn’t be able to make payments for long. I know a lot of people with low 6 figure incomes in 600k+ places; they’ve stretched to get in and won’t be happy if their circumstances change.

Most high income folks with 700+ FICO scores will be able to hold on to their homes, as long as they keep their high-paying jobs, and as long as interest rates remain low.

Interestingly, the last time there was a big surge in foreclosures, setting the all-time record for foreclosures in California, was March 1996. This surge in foreclosures was followed by a run-up, not deflation, in home prices. This was because of a rapid expansion of the economy accompanied by a decrease in mortgage rates. That 1996 peak in foreclosures reflected what had already happened to home prices, rather than predicting what was to come.

Of course, much is different now. But what happens next with home prices is not predestined, but rather will be influenced by the economy and interest rates in the months and years to come.

Dan, not to nitpick but the peak in foreclosures that you describe was at the tail end of a multi-year housing bust. It’s like pointing to the bottom of the NASDAQ bust and saying, “see, stocks starting going back up.” House prices were flat in nominal terms and fell in real terms prior to that period. And prior to the peak, there were steady years of increasing foreclosures, much like we’re starting just now. So, I don’t think your argument holds much water.

I agree with you that high-fico, high income owners have a better chance of survival, but that’s speculation on your part. You don’t know how much leverage they’ve taken on, or how exposed those folks are to the ARM-merry-go-round…

More useful information is to compare the amount of foreclosures as a percentage of overall homes, vs the same ratio back in the early 90’s.

Anybody who wasn’t expecting foreclosures to increase must not have been paying attention.

Also, can Socket Site pls state their own position? Homeowner? Ex-homeowner? Renter? etc. If you guys can state your position, this would be a much fairer forum. That way, homeowners can realize why there is so much negativity on this board. Anybody coming on to this board for the first time would think the sky is falling.

You got it all wrong. It seems like the sky is falling because the sky is falling. Wake up. After ten years of inexplicable gains across the entire state of California, the “financing revolution” is nearing its end.

Last year, Californians lost their homes at a rate of 100 per week. It’s now 900 per week. Interpret it however you will, but it’s a fact. It has zero to do with who owns a home, who doesn’t, who’s bearish and who’s bullish.

This site is essentially one gigantic billboard for San Francisco real estate, so your accusation that the forum is “unfair” due to the lack of a stated position rings hollow.

The funny thing is (which posters should also list) – everyone on this blog is probably in their 20s and 30s. I’m 32 and a renter.

My 85 year old grandfather is laughing at all this sub-prime stuff. He told me 5 years ago, when interest only mortgages started coming out and I mentioned “this is a scam, these people can not really afford the house they’re buying,” that every few decades a housing scam like this comes out and when it crashes, people lose their shirts. The S&L scandals are in the past and most of us aren’t old enough to remember the others. The only stable market is one that grows slowly, relative to incomes, and at higher interest rates. And yes, stable markets also see DEPRECIATION (something that Californians appear to not believe exists, even though SF saw 30% losses in the 80s). Simple real estate investment says that as newer units come on the market, older units depreciate unless investments are made to update them OR unless there is such a demand that no one cares if they are new or old (which SF saw 6-10 years ago, but no more). Things aren’t crashing right now because, even though there isn’t high demand, sellers are too proud to lower their expectations and prices. They will wake up.

anon, your grandpa is a wise man. California is prone to real estate cycles every decade or so, sometimes regardless of exogenous economic factors. Maybe it’s the boom-bust history of our state…has affected people’s mentality. Always a gold rush or land grab or silver lode or something. Get rich quick with tech stocks. Tech bubble popped? Get rich quick flipping real estate.

“Things aren’t crashing right now because, even though there isn’t high demand, sellers are too proud to lower their expectations and prices. They will wake up.”

Anon raises an interesting point, and I wonder if anyone is aware of solid data on the numbers of MLS-listed units that actually sold. I’ve been looking for the past year or so at 3-4 BR SFRs in certain neighborhoods, and I have seen dozens of places that looked interesting but which also seemed (to me) to be priced far too high. These just disappeared from the MLS and follow up research on Zillow, etc. appears to indicate that the sellers simply pulled the listing and did not sell at all — likely because nobody offered them the price they wanted (although I suppose there are a few other scattered reasons). Many sellers can afford to do that for a limited period. But many or most sellers will simply have to just lower their inflated expectations at some point and take what the market is offering. We have lots of data on what has sold but I’ve not seen anything on what has not other than days-listed data where the listing stays on the MLS. This could be a helpful indicator on the state of the market.

“…everyone on this blog is probably in their 20s and 30s.” I’m in my mid-forties, and have lived in California most of my life, so I remember past cycles.

As I wrote above, “That 1996 peak in foreclosures reflected what had already happened to home prices, rather than predicting what was to come. Of course, much is different now.”

Yes, 2007 is not 1996, by any measure. However, real estate down cycles in the past have co-incided with recessions and rises in interest rates.

This idea that high-income/high FICO’s will protect SF will be interesting to watch play out.

The reality is that FICO’s are only high if you pay your bills on time. It doesn’t necessarily matter whether that bill is $100 or $100,000.

And while a lower-income earner without a lot of job options, no savings and a resetting ARM doesn’t have any flexibility in a down market, don’t think that just because someone makes a lot that they are protected from risky financial decision making too.

I own in SF and have a very high income (no flames, please, just giving perspective). So I have one foot in the door, so to speak, into the world of people who are buying big homes in Pac Heights, Presidio Heights, etc, even though that’s not me.

There’s no special magic to financial security for the wealthy. You have to spend less than you make and protect your assets. Just like everyone else. So if I leverage up my big Marina house with a ARM refi/equity line to buy a place in Tahoe and/or Napa, buy a nice new Mercedes and take a $$ vacation, and figure “savings” will come from real estate appreciation, I’m just as exposed to a declining market.

I’ve felt like a dinosaur these last few years with low debt/income and a 30yr. fixed mortgage, because “people just don’t do that anymore”. But I’d be willing to bet that if you walk down Union St. or Sacramento St., some of those beautiful people wearing beautiful clothes getting into beautiful cars, are trying to figure out how to pay their property tax (that is now in arrears).

This is an expensive city, and you can hemorraghe almost unlimited sums without trying too hard. It’s just a matter of 00’s; the same principles apply for everyone.

Great post Michele! I agree with what you wrote. There are a lot of wealthy people here, and a lot of wealthy people who stretch as well.

B/c only ‘12% can afford to buy’ in SF, we need to be understanding of those who aren’t in our financial positions, or who did not buy over the past 10 years.

Of the 30-35 people out of 50 that own in my office, I would have to say a majority of them have 30-yr fixed loans at UNDER 6%. The rest have 6-6.125% rates on a 30-yr. Other homeowners have 5-7 yr ARMS in the low 5% rate. When the ARMS refinance, they go from 5.25%-5.5% to 5.75%-6% which is no big deal since over the past 5-7 years of their ARM, they’ve paid off 60-100K in principal, and their earnings have risen by 50-150% since.

Does anybody know if Socket site is an owner or renter? It seems that they are renters.

Great info Prime. I agree, this seems like a renter site, but we have to remember that these penniless fools have the right to express their opinions too.

Often, at my yacht club meetings, the discourse turns to real estate and we all tend to agree that there is no better investment. It is a good thing that no one really takes the discussion and collaboration that occurs on the internet seriously.

Agreed with you Rib. The other day I was sitting on my whale leather couch and skimming through the latest Robb Report, while my butler read SocketSite postings to me aloud. Some of these people who only make 6 figures a year can be so trite and pedantic. After a while I felt a case of ennui coming on, and had to take my Lambo around the block a few times to pick up my spirits (I prefer the Enzo but it was in the shop).

Prime: Your statistics remind me of those surveys that show the majority of people are convinced that they are all above average.

In your office the “majority” of people have 30 year fixed rate mortgages and yet 70% of mortgage originations over the past few years in the Bay Area were short term ARMs.

In your office around 70% of the people are homeowners and yet according to the last census less than 40% of SF residents own.

In your office “over the past 5-7 years…their earnings have risen by 50-150%…” There’s only one profession in the Bay Area that has seen that kind of income growth. And it’s not technology. Or banking.

Prime, may I ask what your office is? Because I am obviously in the wrong profession. Being the “penniless fool” that I am who works his ass off everyday designing high-end remodels for Owners whom I have to argue with every month to just get them to pay their measly $1500 bill.

The Chron. published 2006 income data a few monthes ago. It showed that incomes went up 1.6% in SF last year. Which, of course, is completely absorbed by inflation.

Btw, do you need a high-end remodel done to your house?

Yikes, you guys are mean flaming Michele for her ‘very high income’ statement. Truth be told, there are many ‘very high income’ people in SF believe it or not. 🙂

Someone wrote. “Your statistics remind me of those surveys that show the majority of people are convinced that they are all above average.”

Isn’t it peculiar that everybody thinks people here think the economy is going down the tubes, yet everybody will be ok and be gainfully employed with healthy incomes? I love it.

Rg, you may note that perhaps the wealthy got that way b/c they focused on the bottom line, and not frivolous spending? Hmmmm.

“Yikes, you guys are mean flaming Michele for her ‘very high income’ statement.”

Give it a rest Prime. Nobody is flaming Michele’s excellent comment. They’re all making fun of you and your fantasy office. But you probably already knew that.

And because you seemed to have missed it, the whole point is the economy is just fine, people are employed, and incomes are healthy. And yet defaults are increasing, sales volumes have been trending down over the past three years, and property values seem to be flat to down depending upon your data source. Get a clue or just go away.