It has been three weeks since Labor Day and new listings of single family homes, condos, and TICs continue to outpace sales in San Francisco (although the gap has narrowed). Over the past week, roughly 230 new listings hit the MLS and the inventory of Active listed units in San Francisco increased about 2.2%. The percentage of reduced listings is holding relatively steady at ~19%.

Based on last months sales, we’re looking at about 2.5 months of listed inventory. And as always, these figures only take into account Active listed inventory (but that’s all about to change). Be sure to “plug in” tomorrow for the launch of SocketSite’s Complete Inventory Index (Cii).

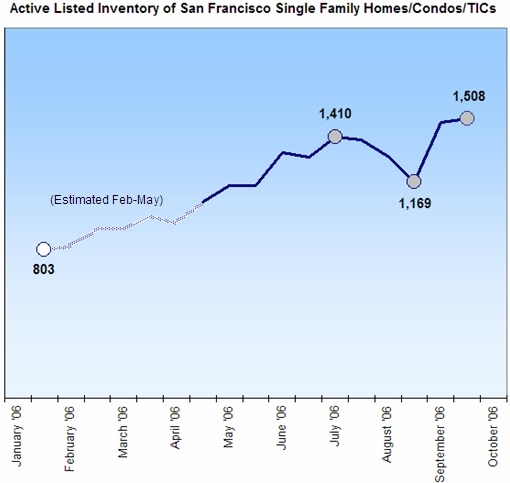

∙ SocketSite’s San Francisco Inventory Update: 9/05/06 [SocketSite]

Historicaly, inventory always goes up after Labor Day. Last year things were still selling at a crazy pace, whereas we all know things are sitting on the market a whole lot longer this year. I feel this is obviously a great time for buyers. People freak out because interests rate aren’t in the 4’s anymore, but money is still relatively cheap. People are going to be waiting a long,long time if they want to see interest rates go that low again. Might never happen again.

You really think its a great time for buyers? I feel its still too expensive, and the price cuts recently still haven’t offset the interest rate hikes over the last year. Sounds like youre an agent trying to influence buyers into thinking the affordability will worsen over the next few months. I plan to take that gamble, and I have a feeling I wont be the only one.

I am a realtor – and if I could time the market I wouldn’t be working 24/7 …. but to weigh in my 2 cents I think it’s a great time to find a bargain AND I think there’s probably some more correction coming. Trick is how much. If you’re one for looking at trends the market traditionally picks up in Spring so ‘theoretically’ between now and Spring is a good time to get in.

That being said I also believe the years of double digit appreciation are behind us for at least the immediate future…so along with Socketsite’s comment (cant remember where I read it) plan to buy a property you like, one that you wont immediately grow out of and I would plan on staying in it for a minimum of 5 years to make sure you get your money back out.

Prior to the last decade run up on property appreciation, average per year appreciation was between 5-7% per year. I would plan on that for any purchase I make (and I am currently looking to buy myself) and I will be very happily surprised if it outpaced that.

B, I have to disagree with this: “I think it’s a great time to find a bargain”

How can you call picking up properties at the peak of a huge price runup the time to find bargains?

Fair question. Allow me to elaborate. Because we are not at a peak currently. That would arguably have been roughly in March of this year for the current run up. More inventory, longer sit times, and for sellers who need to move you can finally start asking for concessions depending on the property.

Example – a condo I’ve had my eye on which is was a rental, been sitting vacant, shows terribly and the owner’s had it for over 10 years. Listed below current comps already, but because it shows terribly and has been on the market for 60 days; I’m going to make a very little contingency offer, 14 day close but go in $40k under the asking price – which will put it $100k less than an almost identical unit which closed just 2 months ago.

Because they are losing money every month and dont know if the market is going to continue to go down (plus they are already realizing a nice profit as they’ve owned it for so long) I’m gambling a quick close and ‘sure thing’ will get them to bite.

And I would call that a bargain if it goes through. That’s one of many good deals to be had in this market that would not have been available when the market was moving quicker. Only hindsight will tell if it was a bargain or not. SF is only 7×7 and there still are a ton of buyers out there. They are just playing chicken with the Sellers.

I dont know, nor does anyone, how much more of a correction there will be in SF but I’m solidly in the camp that SF is a strong real estate market and one should capitalize on the weaker markets as they present themselves. Last time I bought was just following 9/11. And I dont expect to make such a quick or healthy profit on my investment this time around. If that was why I was buying I might do better in stocks – although I’ve made and lost a lot of money there also.

Yes, ladies and gents, now is a great time to buy! Buying real estate now is like loading up on stocks when the nasdaq index pulled back to 4500. Good luck with that.

Got it so you’re a bear on the real estate market…and you think the real estate in SF is going to lose half it’s value in the next year?

Maybe not 50% in a year, but 10-20% is highly possible. Even you admit that “normal” appreciation is 5-7% a year. Yet values have gone up 100% in the last 5 years, more in some areas. So to return to that 5-7% range, prices either have to fall significantly or be flat until incomes catch up. It’s called mean reversion in mathematics. In either case, if you look at cap rates, it makes no sense to buy in SF right now….you literally make money by renting vs. owning.

Historically speaking we are far more likely to see a flat-lining of prices than a sharp decline. Especially in SF. I wont argue it could drop 10-20%, but I would strongly argue against the fact that it’s ‘highly possible’ aka probable. History just doesn’t bear out that kind of a decline in SF. Hawaii yes, LA yes, but so far not SF. I’m not saying it cant happen. But I am saying it isn’t likely to drop that sharply here – if you use history as a barometer.

B wrote, “we are far more likely to see a flat-lining of prices.”

So again, if prices are staying flat for the next few years, why should buyers jump in now instead of waiting for incomes to rise so that the purchase becomes quasi-affordable? Isn’t it smarter to invest excess income in something generating 5% return instead of being flat, like any high yield savings account, and wait?

(Yes, I know that real estate never goes down, and if I don’t buy now I’ll never get in because the same closet that sells for $600K today will be worth $5 million in 10 years and I’ll end up living in my car forever. But I’m willing to risk it.)

Dude and I’m with icallbs – you’re both right. Even if real estate stays flat for a year or two, that’s a REAL inflation-adjusted decline. Assuming everyone buying the average 1000sf marina condo is putting down min. 20% (laughing yet?), they’d be far better served putting that cash in a cd at 5%+ and waiting it out. If prices go down even 10% (optimistic in my opinion, i think nominal declines could be more), that’s going to cause an awful lot of pain, especially for the rare few that put less than 10% down, and that’s before B’s commission.

I’m not arguing real estate never goes down. I lost a years worth of income on an investment that was supposed to be a 10 year hold that I was forced to sell in 2 for partner reasons in a market much like this, same time of year too…it was an excellent buy for the buyer that capitalized on my error. I too had to pay the commissions on both sides – it was an area I wasn’t comfortable representing myself in. Fortunately it didn’t come out of my immediate pocket but was leveraged against another property that I had the equity to absorb it in.

Which brings me to my point. Yes there’s an argument for popping that cash into a safe CD at 5% interest, and if you don’t need the tax write off – many don’t – and don’t care about being able to leverage the investment, and don’t care about whether your landlord is going to jack the rent or sell the place at an inopportune time and you believe the market is going to go back to it’s 1999 prices or is not going to appreciate at all for the next 10 years, then yes a 5+ CD is the best option.

It’s just for me, my grandfather, and most of my modest earning friends the only real money they ever made – and kept – was in real estate, and I find myself wondering at your statement that its best to wait it out. Because how long is long enough to ‘wait it out’? How long have you been waiting it out and how much money did you leave on the table since you first thought about buying, and how much money do you really invest in that 5+ CD or did you buy a nice car with your extra cash like most do when they aren’t forced to save?

All rhetorical questions by the way, I’m not intending any personal insults I actually appreciate the debate and recognized the validity of the argument. It’s just I’ve been hearing for over a decade the market is over-inflated and I look at the world’s population, and I look at how many places are as nice to live at as here…and I think there’s quite a few world wide that will make it a priority to own a home here.

And I’m happy to see the market slow down as the rate of appreciation we’ve seen is unsustainable. I also think we are not at bottom yet but I still see ‘good buys’ to be had and that’s as someone who watches the real estate market constantly, is looking to make a move, and not as an agent who needs a sale to make a commission or someone desperate to protect the credibility of this market.

B – you make some valid points, i guess we’re just going to have to agree to disagree. As far as forced savings go, i agree that a lot of people may need that; however, if those people lack the discipline to save, what’s going to stop them from opening a HELOC (and putting it to use) if the value of their home increases? I’m very financially disciplined, save/invest about half my income and for me, it makes sense to wait and see what happens and not put my $ at risk, especially since economic/housing data is making a very strong case for cyclical downturn in real estate. As long as prices continue to remain unreasonably decoupled from incomes, it pays (literally) to wait. I’m also a firm believer (like one of the other posters) in mean reversion, and when gains outpace historical norms for nearly a decade, i believe a period of below average returns is to be expected. I agree that over the long run, real estate always increases in value, though historically it doesn’t increase at a rate that much greater than inflation (maybe an extra 1-2%). And while i believe timing any market – housing, equities, etc. – is foolish, i do believe that there are times when it is foolish to ignore the trends.

Touche on the Heloc (second mortgage) comment. I did think about that but I was already way over a polite blog entry length at that point.

So September 28 2008 we can debate our positions again. I intend to buy between now and Feb/March and we can see if I lost gained or pushed.

Your position is to wait it out a year, or more?

Don’t know about the others, but I’m definitely waiting until mid 2007 to see what happens. Prices might fall more by then, but they’re definitely not going up by another 20%, so I lose nothing and get to increase my savings for a down payment. If we fall into a recession, there will be increased downward pressure on home prices (we have an inverted yield curve despite rates still being near historical lows).

Let’s not forget that rates might rise more to prop up the dollar against the Euro and Renminbi. Paulson didn’t make much progress in his recent currency talks with China. So basically, there are a lot of reasons to wait.

B – yes, a 2008 debate sounds fine, i plan on staying on the sidelines through the end of ’07 and into ’08.

Dude – i agree that there are a lot of macroeconomic factors we need to watch over the coming year. the yield curve doesn’t paint a pretty picture. hopefully a soft landing is in the cards.

Yep, I can back a hold to mid 2007 and possibly even 08, but my theory is there may not be the easy pickings of inventory by then, not that I expect a run up on pricing. I think Seller’s who are not getting their return will hunker down and pull from market and I like a wider selection to pick and choose from. I’m not seeing the problems with adjustible loan rates forcing sales and I think the Feds may even start lowering interest rates again early 07.

Caveat to my lower interest comment: China floating their currency, importation tariffs and the Bond market withstanding – of course.

B: where is that inventory going to go? People who need/want to sell are price takers.They can’t afford to wait it out 2 years for the market to come back. Anyone who bought in ’03 or before will still sell because even if prices fall to ’04 levels, they still made a profit and don’t care. I guess I’m saying that only specuvestors who bought last year under a sustainable financing arrangement will pull out and wait. The rest will take what buyers give them or bleed cash by renting.

Also, I belive the bulk of the ARMs will be adjusting early next year and into ’08 – that’s when the damage will really start. Coincidentally, government announced today they’re pushing for lenders to phase out what they call “affordability loans” – ARMs, IOs, etc. That reduces the pool of qualified buyers even further.

[Removed by Editor]

Good arguments but just theories on the bear side. If interest rates continue to rise that could put pressure on those ARM’s – but if interest rates dip next year any of those ARM’s coming due will get refinanced. 30 year fixed loans w/ 10 year interest only payment options are competitive right now which is the loan program I’m getting into. My clients that bought 1 & 2 years ago are all in minimum of 5 yr. fixed interest only options. That still gives tham a minimum of 3 more years to see what the market will do, or refinance. And the most common thing to do with a property you are not going to stay in is to rent it. My friends that are leasing agents say they can’t keep inventory it’s flying off the shelves so fast (the owners are still taking a monthly hit but at least they can write that off and if they end up having to sell at a loss it too is a write off whereas a loss in a principal residence is not).